PVC Nov 2025 futures break below $4,600!

With PMI surging to 67.1, it signals stronger construction demand.

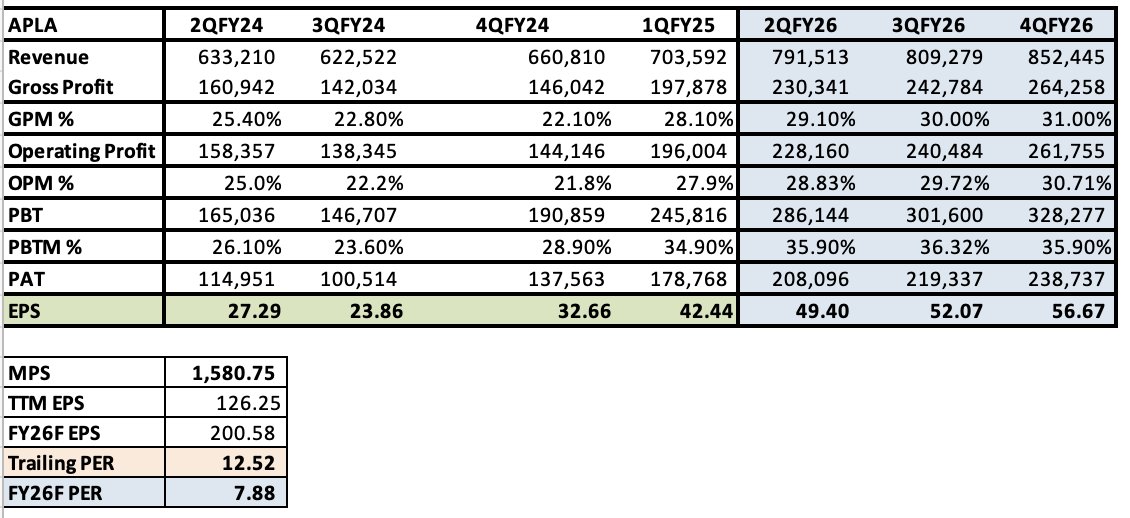

Macro setup for #APLA looks strong given the expected improvement in GPM and increase in capacity utilisations.

With the split boosting liquidity, is a rerating next?

English