Legend1

223 posts

$ARM if 180 breaks its an inverted head and shoulders on weekly measured move to 280.

PT for 2027 280.

English

@colin_gladman @colin_gladman , what do you think of AVIS (CAR)? It went parabolic. Is it good time to take some long dated puts?

English

@Kelvinccccccccc Maybe because nobody knew about it? I was one of the first people to point out $AXTI in relation to photonics bottlenecks.

And NCI is an even more the niche upstream red phosphorus supplier needed to make InP substrates.

So the even more unknown bottleneck of a bottleneck.

English

A Guide by Serenity:

How to Cripple the Western Hyperscaler buildout with just $170m.

Just take over Nippon Chemical (4092) with $169m!

For InP substrates, you need: Indium and High Purity Phosphorus.

Thought $AXTI was a bottleneck? NCI is the bottleneck of the bottleneck.

NCI is actually the leader of the high purity red phosphorus chokepoint holding 26-27% of the market share (Rasa has less share, then the rest is China).

And they export to $AXTI, Sumitomo, JX that need it to make InP substrates.

So… if you have $160m to spend to acquire NCI (plus Rasa as smaller capacity), you can remove the leading Western world’s production of 6N/7N red phosphorus needed to make InP substrates!

And without InP substrates: no photonics.

Fun fact: China’s tech companies would get pretty disrupted with it too by NCI.

For $AXTI, the mapping/reliance is actually pretty interesting:

- AXT's Tongmei outlined its structural reliance on importing high-purity precursor materials from Japan on their STAR Market listing

- WITS data showing ~$460/kg high-purity phosphorus flowing from Japan into China

So they secretly do depend on NCI.

China does have capacity like Wylton Chemical, Qin Xi New Materials, Jinding Electronics, and Chuxiong Chuanzhi, Guizhou Wylton Jinglin Electronic Materials as well.

However, they’re all smaller players so can’t make up for high purity red phosphorus capacity provided by NCI for InP substrate production at scale.

$LITE CEO already said inp substrates keeps him up at night.

So now with NCI, you can give the guy permanent insomnia?

For just $169M.

So here's what the supply chain looks like:

-> DGC phosphate rock mine and ships it to NCI

-> NCI refines Yellow Phosphorus into High Purity Red Phosphorus

-> Sumitomo / JX / AXT melt the Red Phosphorus with Indium to grow InP Substrates

-> $COHR / $LITE fab InP substrates into Lasers

-> Innolight/Fabrinet package them into 800G/1.6T transceivers

-> $NVDA / $GOOGL use them for ASIC/GPU clusters.

And basically, the entire West depends on NCI to make InP substrates for photonics.

I hold some very small positions, just for fun. However, Japan is not well known for price hiking.

So you’d probably run into regulatory problems eg. FEFTA if you bought the company and hiked prices 15000% (like government seizing back the company once they realize)…

Maybe 30-50% hikes is possible to compress fwd p/e? But very likely wont end up like $AXTI.

Regardless, this company is a massive, massive national security risk priced at ~$160m.

As for fundamentals, they’re trading at .54 book value and a forward P/E of 11.4 so it’s probably undervalued anyway.

TLDR:

-> Is it the next $AXTI? No.

-> Is it an unknown structural bottleneck + critical vulnerability of the Western hyperscaler buildout with photonics? Yes.

-> Is there still room for re-rating?

Just reverting to Book Value of 1 is immediate 80-85% upside. Maybe more if you give it multiples past 11 fwd p/e.

Regardless, it’s fun to find a major point of failure in the hyperscaler supply chains for $169m.

English

@grok @SaralTrader @Banana3Stocks @grok how much of straight of Hormuz capacity is severed through east west pipeline

English

Yes, this is true based on today's announcement from Saudi Arabia's Ministry of Energy.

They confirmed restoring full pumping capacity on the East-West (Petroline) pipeline to ~7 million bpd after recent attacks during the Iran conflict reduced it by 700k bpd. The line runs from eastern fields to Yanbu on the Red Sea, bypassing the Strait of Hormuz.

Source: Reuters (and multiple outlets quoting the ministry statement, April 12, 2026). The "needs no more Strait" phrasing is interpretive hype—not an official quote.

English

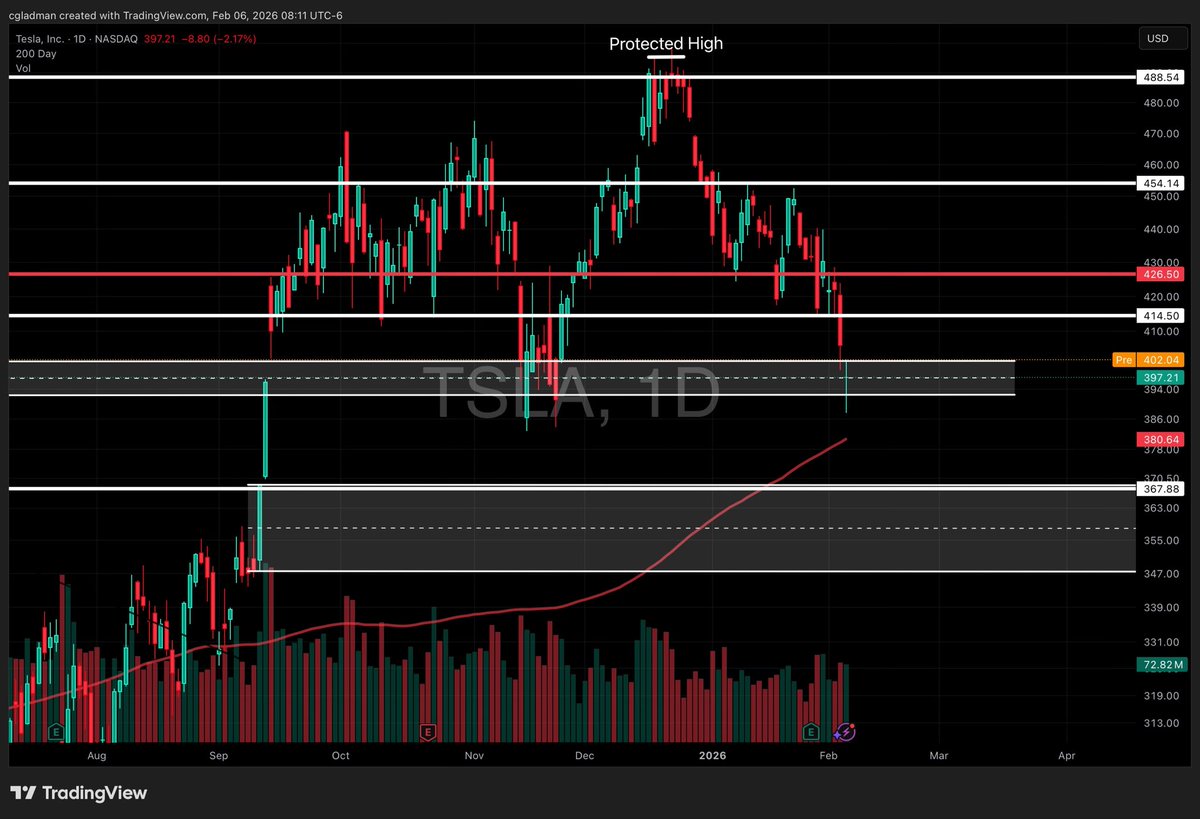

@colin_gladman Tsla death cross over. More bearish. You are great with TSLA puts. Hats off

English

Did you listen to the podcast today? $SPY @21RatesHQ

ProblemSniper@ProblemSniper

$SPY $SPX @21RatesHQ

English

The current bottleneck: Transformers/Switchgear.

Trade Idea: Long Hammond (~2.2B CAD / ~$1.5B USD) at 184 CAD.

They dominate the market for:

-Transformers (dry, multi year bottleneck ~23% of market),

-serve to switchgear (2-3Y bottleneck)

-and manufacture liquid too (5Y, larger bottleneck)

I personally anticipate components price hikes like NAND, as $AMZN, $MSFT and others compete for allocation.

You might have seen: “Half of US data center builds have been delayed or canceled, growth limited by shortages of power infrastructure”…

Then you go further:

“To address shortages… Canada, Mexico… became the biggest suppliers of high-power transformers for AI data centers to AI data centers”

Guess who is in Canada (Guelph).. Mexico (Monterrey 3 and 4)… and the US?

Hammond

Then here’s the reason the articles cite why hyperscaler DB buildouts are falling apart:

“Major reason behind these setbacks is the availability of key electrical components — such as transformers, switchgear”.

Institutions are probably looking at Powell, Eaton, and others… but little do they know?

Companies like these actually buy Hammond’s transformers to put inside their own switchgear (“strong sales into data centres, switchgear manufacturers")

Their market share over the transformers market is actually pretty large (eg. ~23% dry).

The most compelling signal:

-> 122% Y/Y 2025 backlog increase. And we can infer this to be 1B+ CAD.

Eg. company achieved 898m CAD in sales in 2025, capacity ceiling. Management said close of Q3 2025 orders were valued at 53% of the entire closing third-quarter backlog.

Given that Q4 2025 revenue was 254 million and the backlog is "more than doubled," we can infer a total backlog value exceeding 1 billion CAD.

Also:

“Gross margin compression last year was due to the buildout of their Mexico facility, but both gross margins are expected to increase and the facility expansions are expectied to turn into accelerated revenue Q2 2026)” which is now.

Downside is if raw material costs (copper, electrical steel) spike again, but given this bottleneck, they can price hike.

Personal FWD P/E estimates would be ~18-21 for 2026, <15 for 2027 from volume ramp.

But I think it’s possible to hit single digit fwd P/E if they do price hikes mixed with hyperscaler emergency orders. But that might get a little mixed with the new acquisition.

Regardless still looks cheap.

Just a TLDR:

$AMZN, $MSFT, $META, $GOOGL, $ORCL datacenter are being bottlenecked because of a lack of transformers/switchgear.

Seems like markets missed this little player with large market share, despite backlog visibility and increasing revenue from capacity expansion coming online.

I personally found it pretty compelling, so I went long.

Just sharing my personal thoughts, of course DYOR before making any decisions yourself.

English

🚨 Incoming short report to drop soon on memory sector

I was given a glimpse on what is leading the selloff of memory sector and its bad.

Sora appears to be just the first announcement of planned shutdowns of Ai video. Report suggests OpenAi was struggling to keep up with commitments to purchase up to 50% of the global supply of RAM after costs exploded, making it difficult to maintain running memory intensive applications globally.

Basically OpenAi has secretly pulled its unrealistic commitment of HBM NAND and DRAM that could have massive implications for price volatility behind the scenes.

$SNDK $MU

English

What do you think has done the most collective damage to humans?

I’ll start: SMARTPHONES

English

@BioMindBeliever @aleabitoreddit Thanks for the reply. Looks like Robinhood didn’t support this.

English

@Legend1202s1 @aleabitoreddit It’s $SIVEF on Schwab. If you can’t easily find the ticket, sometimes searching by company name will help you find the OTC version of it.

English

@aleabitoreddit Here's to hoping that your $SIVE play turns out just as epic

English

@ecomTrevor $SIVE was my latest call! My personal short term PT was $2-3B, and it sits at a $300M MC now.

That being said a lot of these existingnames still have a long way to go.

English

Holy ****, my $AXTI thesis was legendary?

AXT is up another 20% today to ATHs at $58.

Happy I got this right, gains in a short time blew away holding $NVDA over the years.

Serenity@aleabitoreddit

Warning: The entire AI industry will likely be bottlenecked by two companies: 1. $AXTI ($700M) 2. $SMTOY ($31.7B) Which both control 60–70%+ of the world's InP substrates. Future $NVDA, $GOOGL TPU v7 pods, $META, $MSFT, $AMZN hyperscaler clusters require InP-based lasers and receivers. $AVGO, $LITE, $COHR use for EMLs for 800G/1.6T transceivers, DFB lasers, and other optical infra. Without InP substrates, the supply chain falters. After looking at TPU BOM to Maia BOM, it looks like future ASICs + GPUs + hyperscaler deployments are heavily reliant on photonics. And two vendors could freeze the global InP substrate market covering nearly all of: - Hyperscaler optics (TPU pods, etc) - Optical transceivers (5g, data) - LiDAR (robotaxis, drones, military) -Optical Modules (interconnect clusters) - Silicon photonics laser dies (Nvidia’s future co-packaged optics and Intel/Broadcom SiPh engines use InP CW laser arrays.) Since these companies make up majority of the market supply: -AXTI (est. ~30–35%) -Sumitomo (est.~30%) - JX Nippon (est. 10-15%) That’s it. (eg. 2021 industry note from Yole states that "Sumitomo Electric + AXT together had “more than 75%” of the InP substrate market") Hyperscalers/AI are moving toward photonics but the entire AI industry is fragile. If either $AXTI or $SMTOY stop supplying materials, the entire future AI buidlout gets crippled. It's even crazier that a $700m company could become the the center of it all. InP substrate will likely one of the biggest bottlenecks alongside HMB as the AI industry shifts to photonics.

English

@CKCapitalxx @grok fact check. How much of the energy is used for AI

English

Taking a MASSIVE position in $IREN on Monday.

Here’s why I’m going all in:

BlackRock just said it themselves: “The real constraint isn’t chips—it’s LAND and ENERGY.”

$IREN controls the largest power campus in the world.

Bigger than $AMZN data centers.

Bigger than $MSFT facilities.

Bigger than $META campuses.

$17B market cap.

For the company that literally controls the bottleneck to the entire AI buildout.

While everyone’s fighting over $NVDA GPUs, $IREN is sitting on 1+ GIGAWATT of power capacity that CANNOT be replicated.

You can’t just “build more power” in 6 months. This takes YEARS.

Meanwhile AI compute demand is doubling every 90 days.

The math is simple:

• Infinite demand

• Fixed supply

• $IREN owns the supply

Monday morning I’m backing up the truck.

This is my highest conviction play for 2026.

$IREN to $150+ by year end.

English

$MU $TSM $NVDA

"Chinese tech giants—including ByteDance, Alibaba, and Tencent—have been authorized to collectively purchase more than 400,000 H200 chips ... but with conditions that are still being finalized."

Trade Whisperer@TradexWhisperer

$MU How acute is that shortage? "For several of our key customers, in the medium term, we are able to support 50% to 2/3 of their demands." "That's why we're really focused on bringing up the supply." (Referring to the megafab constructions in ID and NY) -Micron CEO Sanjay

English

Jensen: we need more memory.

Ai needs memory.

Hate those context window limits?

The memory wars are here to stay anon

English