@JamieHeard5 I will share my live trading alerts (entry and exit points) on WhatsApp. Join for free! ✅

➡️Copy search input Reply "444" to WhatsApp: +18083839160

Here’s the link : wa.me/18083839160/?t…

Interesting in Gas This Week

Winter Vol. There is so much to say and so much that's been said. Three points.

(1) This storm came at exactly the right time from a positioning perspective (something spoken to in this channel both of the last two weeks). January had thoroughly disappointed, speculative interest had drifted net short, and equity / commodity brokers alike were putting out their 'maybe oversold, but revising our price deck lower' reports. What a difference a week makes with 300 Bcf of weather demand added and now up to 100 Bcf of freeze off impact expected to roll into the S&D data over the next three weeks. Que NYMEX from $3 to $5 in record fashion.

(2) Gains will not be participated in equally. Physical marketing matters. NYMEX is $5, but HHUB cash is $8. Chicago February trades $6 but City Gate cash trades $21. Synthetic marketing books don't deliver cash gain, only physical marketing does. Q1 prints will show the difference this small but important detail makes.

(3) One winter storm does not a equity move make. Gas stocks are up a bit but not a lot, and that's okay. Hundreds of million dollars in a quarter of excess gains is of course also just 1-2% in per share cash flow value for many of the large gas businesses and so the first derivative impact of a big natural gas price event is always somewhat muted against the equity value of gas stocks which are discounting the next several decades of future financial returns (and the long term nat gas strip is mostly unchanged). However this storm does remind us that gas is going to be getting more and more volatile as S and D increase but storage adds don't keep pace. One positive demand shock to the system adds a couple percent in the equity stack, but it also takes some breathing room out for the rest of the year for future gas storage. We are now coiled up with better upside skew for every weather event point forward as gas storage, coal stocks, and utility risk appetite have lurched into the 'yellow' zone. Forward strips will never provide the credit for this upside skew (for if they did they'd be hedged and produced) but as you roll quarter to quarter the business do soak up the gains. Much like the marketing line item in marketing midstream businesses or the trading line item in majors / integrated businesses, gas businesses can begin to get some valuation support from the inherent upside associated with their own supply marketing portfolio that isn't reflected in strip but can reward in the quarter.

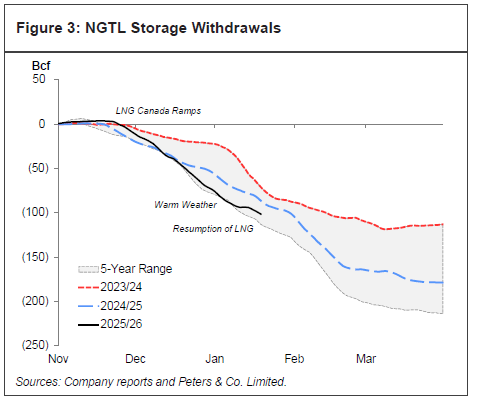

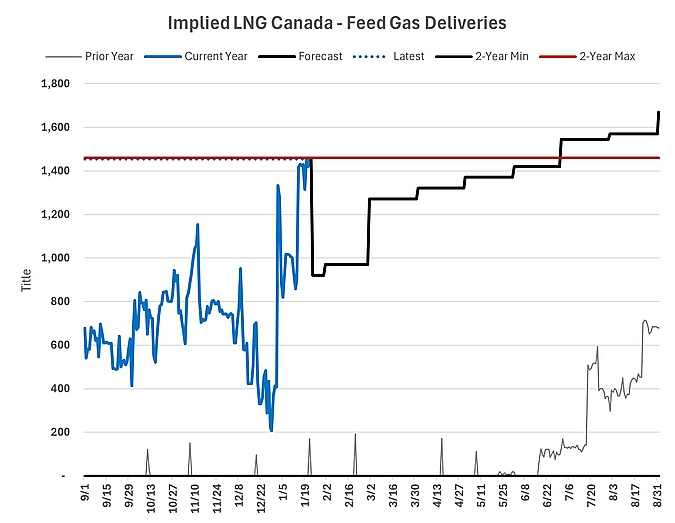

Don't sleep on AECO. This is a mid west storm with mid west price drama but quietly LNG Canada has been hauling out 1.0-1.5 Bcfpd for over a week with 4 loadings in the last 6 days. NGTL drew 3.9 bcf yesterday and is on pace for 4.2 Bcf today. For context we averaged 0.8 Bcfpd out of storage last year. With the plant now on and our own cold weather we could be on for a record seasonal storage draw at AECO. Some PACNW heaviness will slow basis improvement modestly, however great lakes / dawn / mid west is having a fantastic year which could create a dynamic where mid west markets trade up and over HHUB which is a big AECO basis tightener. Net/net supply adds have been very modest, and when the plant is on our aggregate demand load is creating eye popping draws. The solve is less exports to the US and the mechanism is higher local prices.

LNG Canada participant "Equity Sales" I believe are in fact structured equity financings. We don't see any WI in the upstream pipe or LNG facility being allocated to a new party, but instead a new financial partner helping fund Ph2 capital for each participant, in return for a participation in a portion of the Ph1 cash flows. Plant uptime is looking strong and if consistent, will be a difference maker in WCSB S&D this year and Ph2 FID is a sentiment driver that will drive future interest in Canadian gas resource.