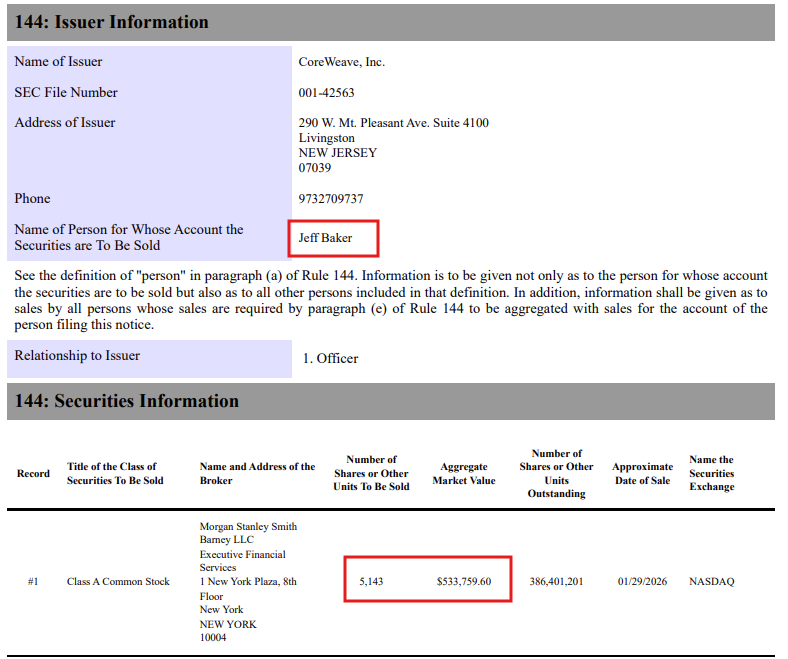

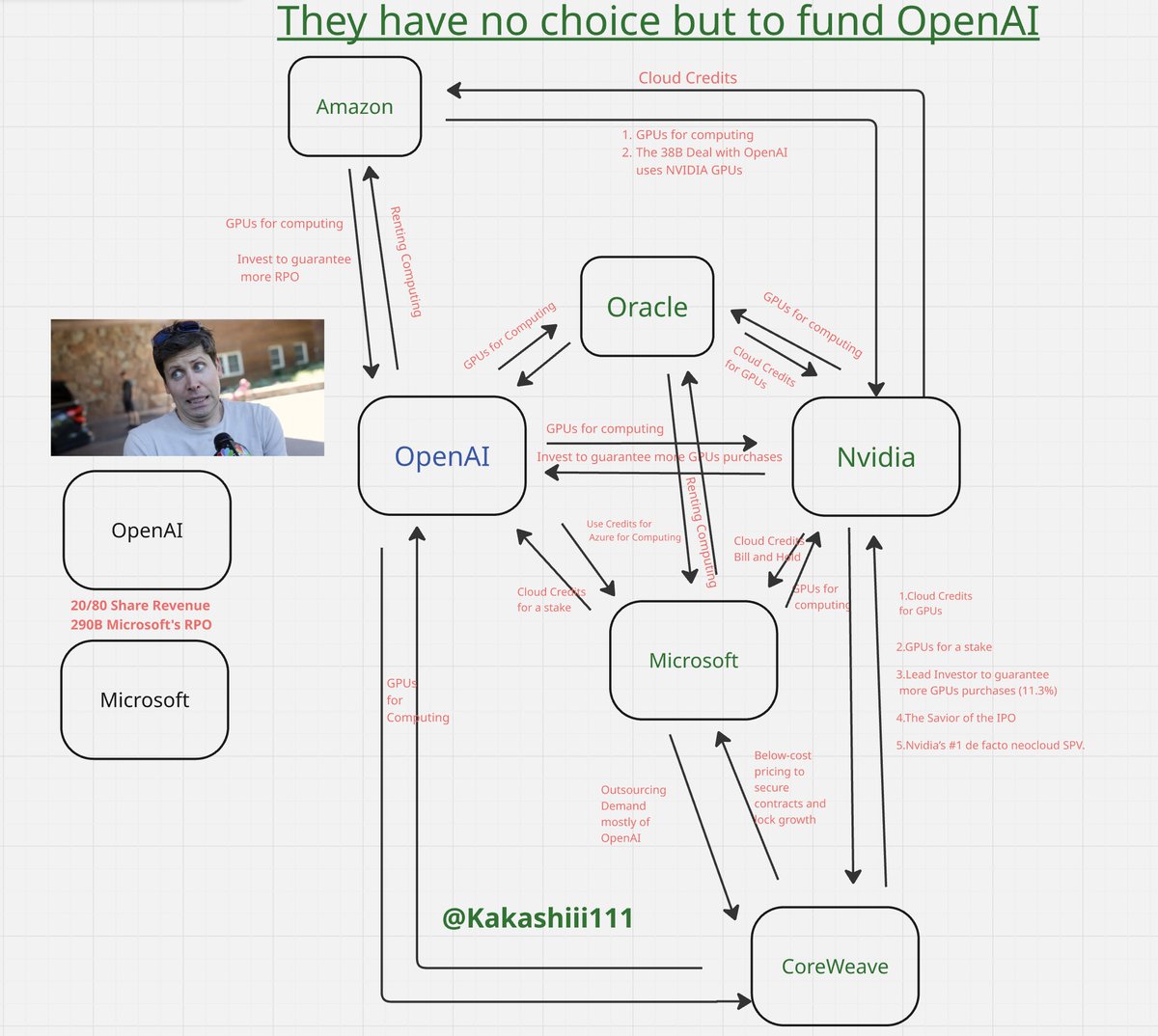

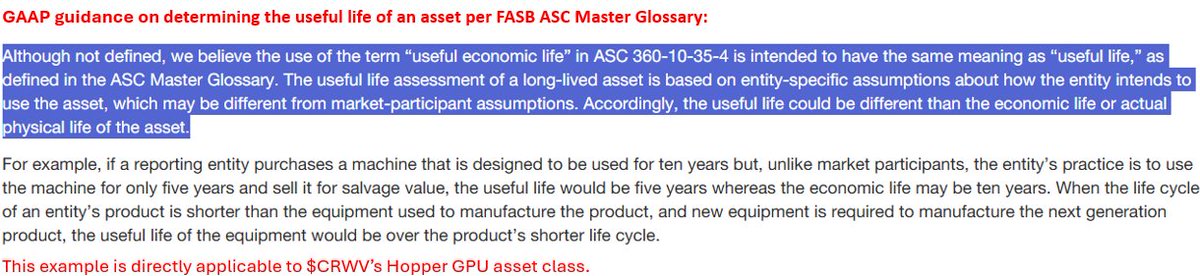

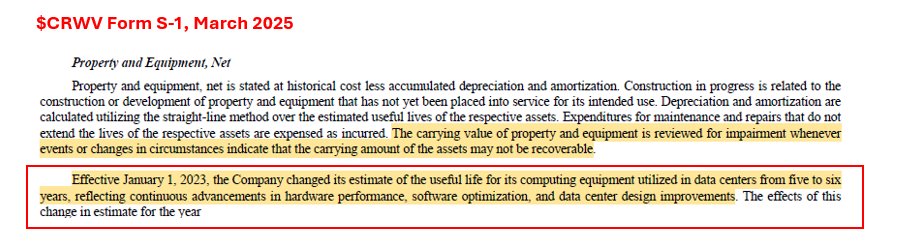

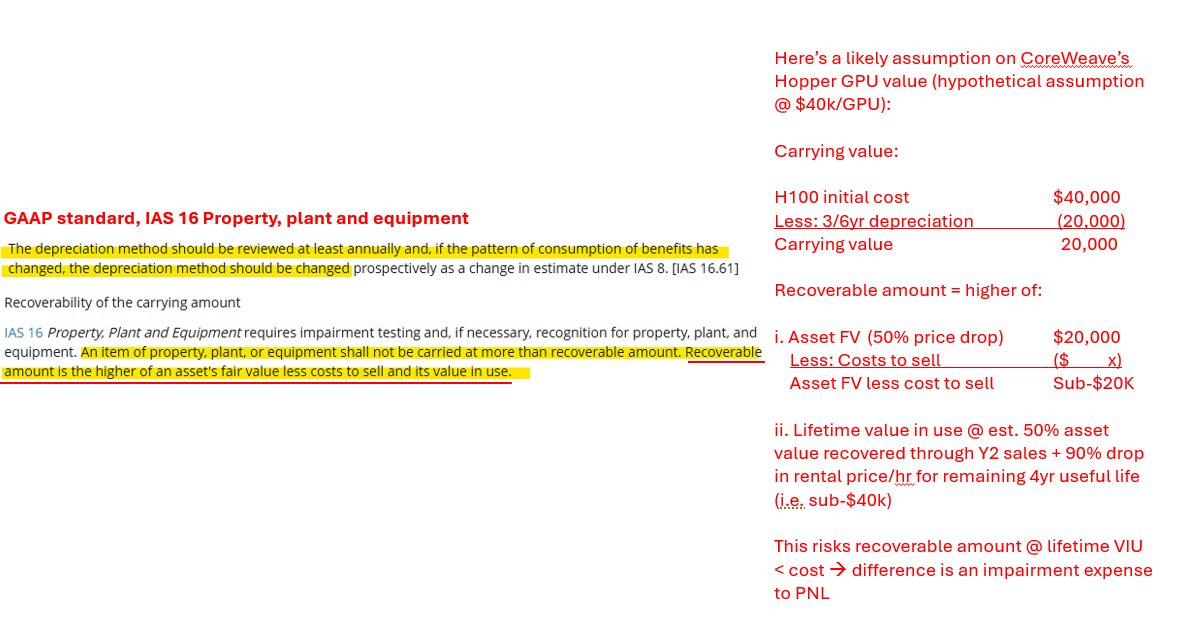

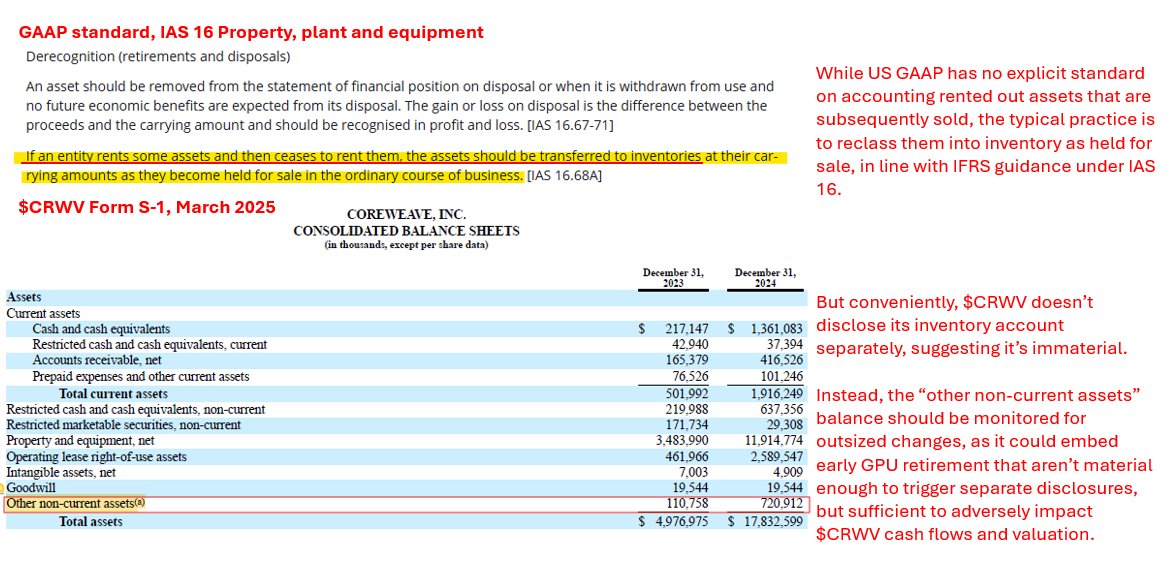

In my past life as an auditor (to those who ask in my DMs - here's your answer), I'd witnessed a material accounting-related valuation reset on a transaction that'd blindsided my client. And this ongoing $CRWV $NVDA debacle is becoming eerily reminiscent of it. It was one of the biggest accounting backfires I've seen. My client had acquired a telco with what seemed like straightforward revenue streams - rent collected from cell towers. But a deeper dive into existing MSAs post-close uncovered a technical accounting issue that'd ultimately converge those revenues into costs. The less accommodative accounting caused the cash flow assumptions used to justify the acquisition to fall apart. The result was a forced write-off, massive goodwill impairment, and a valuation reset that blindsided my client. $CRWV and $NVDA faces a similar fate. $NVDA now owns 7% of $CRWV, whose valuation is based on LT GPU rental contracts. But here’s the caveat: $CRWV assumes a 6yr GPU lifespan, despite $NVDA accelerating its upgrades to a 1yr cadence. Prices for older H100 and even H200 chips are collapsing, down 90% and 50%, respectively. This means $CRWV will eventually be forced to shorten its depreciation schedule. This would alter the cash flow assumptions on which its valuation is based on, resulting in a massive re-rate and write-off to the $NVDA investment. Still don't believe me? The weak link's hidden in plain sight in $CRWV S-1 disclosures: $CRWV said it only deploys capex when there's confidence they can be fully recouped through LT contracts. There are 2 primary types - take or pay and consumption-based contracts. But $CRWV doesn't disclose the mix. Considering the rapid pace of tech advancements, it's unlikely customers like $MSFT are dumb enough to commit to take-or-pays on a rapidly deteriorating GPU. The contracts are likely consumption-heavy, and commitments can be transferred to newer generations of GPUs. This leaves limited evidence that $CRWV 's existing GPUs can generate sales for 6yrs. Even worse, consumption-based contracts tied to older GPUs risk becoming economically obsolete, reducing the PV of LT cash flows. Say I commit $6B to renting H100s and H100s only. With rental prices declining 90% after Y1, it's going to take significantly longer for the $6B commitment to be realized into revenue, which pushes the billing and cash receipt cycle further out. These risks are clearly not priced in for $CRWV and will ripple back to the $NVDA investment too. The AI halo effect may hold for now. But if these accounting cracks widen (it’s just a matter of time), both companies could face a sharp revaluation. Don't be blindsided like my client.