Sabitlenmiş Tweet

$NILI.v

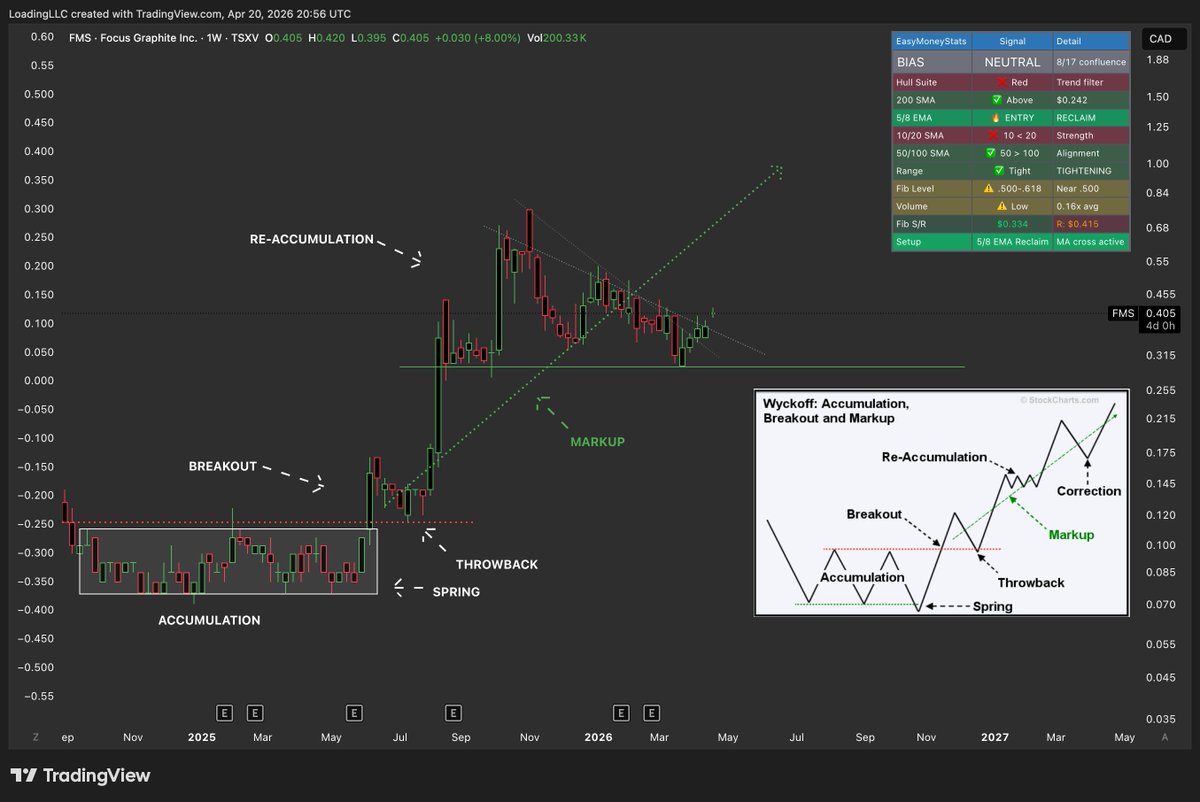

Fractals carry roughly 35% standalone reliability.

Signal quality improves materially when layered against confluent structure:

Unfilled gap at 0.90

Nested inverse H&S across micro and macro timeframes

Confirmed breakout from primary downtrend

Price approaching .618 retracement (launch pad zone)

Improving macro tape across the lithium complex

Confluence stack continues to build.

English