Harsh Mamodia

388 posts

Harsh Mamodia

@MAMODIAHARSH

Investor by Choice, Knowledge hungry , Quest for Growth

New Delhi, India Katılım Kasım 2013

403 Takip Edilen45 Takipçiler

@nileshkurhade Excellent show..wait for concall and guidance

English

@nileshkurhade TAC infosac..Kedia holding..cyber security company.good level to enter

English

SME BULK DEALS on 19/05/2026

🇧 • 544037 • AMIC • Amic Forging Ltd

🟩 • CRONY VYAPAR PVT LTD • BUY • 58,500 SHARES • ₹1,708.94

🟥 • CRONY VYAPAR PVT LTD • SELL • 56,300 SHARES • ₹1,712.17

🟩 • RAMDOOT REALTORS PVT LTD • BUY • 57,400 SHARES • ₹1,716.44

🟥 • RAMDOOT REALTORS PVT LTD • SELL • 57,400 SHARES • ₹1,721.37

🇳 • ARUNAYA • Arunaya Organics Limited

🟥 • KAPADIA FINWEALTH LLP . • SELL • 2,04,000 SHARES • ₹29.93

🇧 • 544747 • EMIAC • Emiac Technologies Ltd

🟩 • ACME CAPITAL MARKET LIMITED • BUY • 64,800 SHARES • ₹107.23

🟥 • ACME CAPITAL MARKET LIMITED • SELL • 8,400 SHARES • ₹104.00

🇧 • 544665 • GLOBALLOG • Global Ocean Logistics India Ltd

🟥 • MARWADI SHARES AND FINANCE LIMITED • SELL • 1,28,000 SHARES • ₹121.56

🟩 • NECTA BLOOM VCC - NECTA BLOOM ONE • BUY • 1,28,000 SHARES • ₹121.56

🇧 • 544759 • GLPL • Goldline Pharmaceutical Ltd

🟩 • CHANDRAPRAKASH KHANDELWAL • BUY • 2,52,000 SHARES • ₹59.75

🟥 • NIRMAN SHARE BROKERS PVT. LTD. • SELL • 1,23,000 SHARES • ₹57.13

🟩 • SUREKHA SHINDE • BUY • 63,000 SHARES • ₹59.75

🇳 • IEML • Indian Emulsifiers Ltd

🟥 • PRUDENT EQUITY PRIVATE LIMITED • SELL • 1,00,000 SHARES • ₹51.89

🇧 • 544160 • JAYKAILASH • Jay Kailash Namkeen Ltd

🟩 • KADARU AKHILA • BUY • 30,400 SHARES • ₹33.58

🟩 • PRERNA CHOPRA • BUY • 32,000 SHARES • ₹31.62

🟥 • PRERNA CHOPRA • SELL • 30,400 SHARES • ₹32.42

🇳 • RFBL • RFBL Flexi Pack Limited

🟩 • CRAFT EMERGING MARKET FUND PCC- CITADEL CAPITAL FUND • BUY • 3,81,000 SHARES • ₹52.50

🟩 • JAGID VANITABEN RAJENDRAPRASAD • BUY • 1,32,000 SHARES • ₹54.94

🟩 • L7 HITECH PRIVATE LIMITED • BUY • 11,79,000 SHARES • ₹52.50

🟩 • L7 SECURITIES PRIVATE LIMITED • BUY • 9,45,000 SHARES • ₹52.50

🟩 • RATHOD DIGVIJAYSINH RAJENDRASINH • BUY • 13,50,000 SHARES • ₹52.50

🟩 • RIDDHI SIDDHI INTERNATIONAL • BUY • 9,51,000 SHARES • ₹52.50

🟩 • SMITAL SURESH THAKKAR • BUY • 1,44,000 SHARES • ₹52.50

🇳 • SAIFL • Sameera Agro And Infra L

🟩 • HI GROWTH CORPORATE SERVICES PVT LTD • BUY • 4,12,000 SHARES • ₹5.85

🟥 • HI GROWTH CORPORATE SERVICES PVT LTD • SELL • 3,64,000 SHARES • ₹5.86

🇳 • TAC • TAC Infosec Limited

🟩 • MULTIPLIER SHARE & STOCK ADVISORS PRIVATE LIMITED • BUY • 1,50,000 SHARES • ₹422.00

🟩 • NEO APEX SHARE BROKING SERVICES LLP • BUY • 3,70,600 SHARES • ₹414.30

🟥 • NEO APEX SHARE BROKING SERVICES LLP • SELL • 1,94,600 SHARES • ₹420.33

English

@RajStockWatch Ashish sir stake is big positive in the counter..with power sector growth in coming years

English

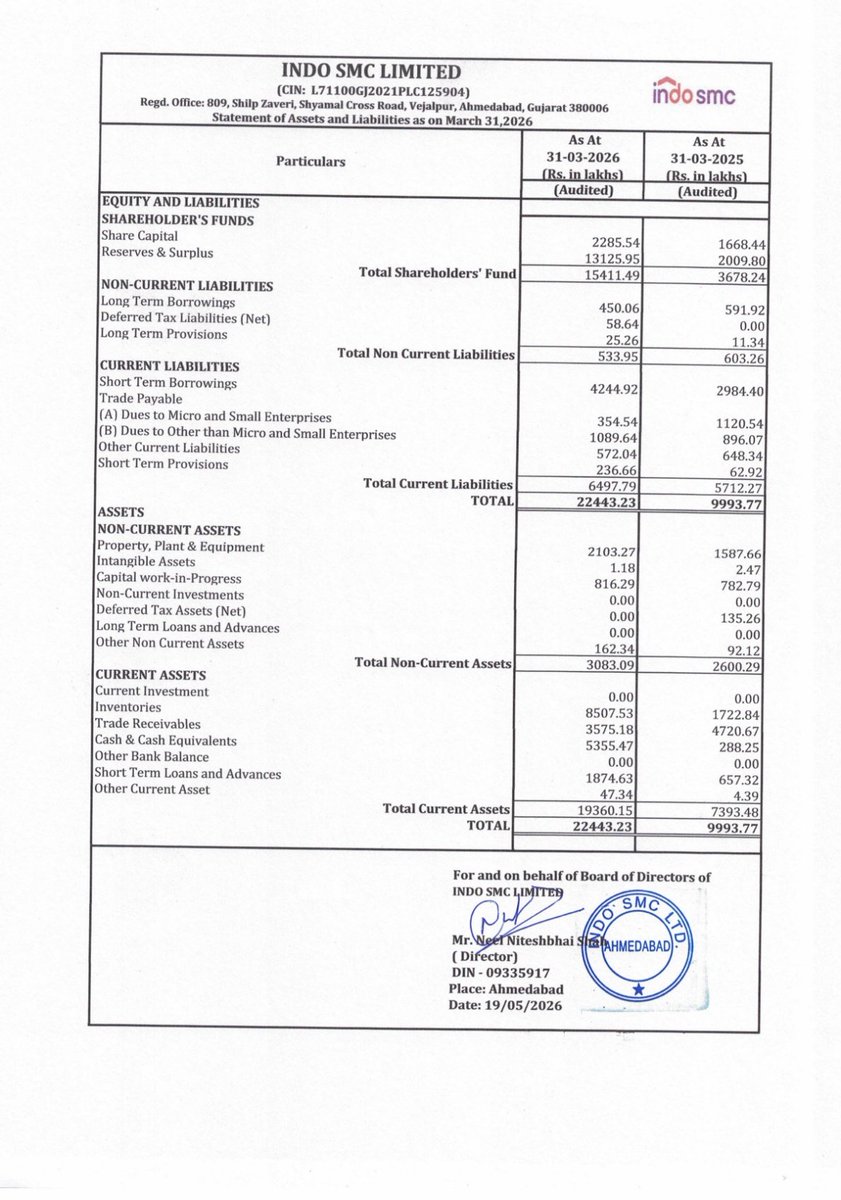

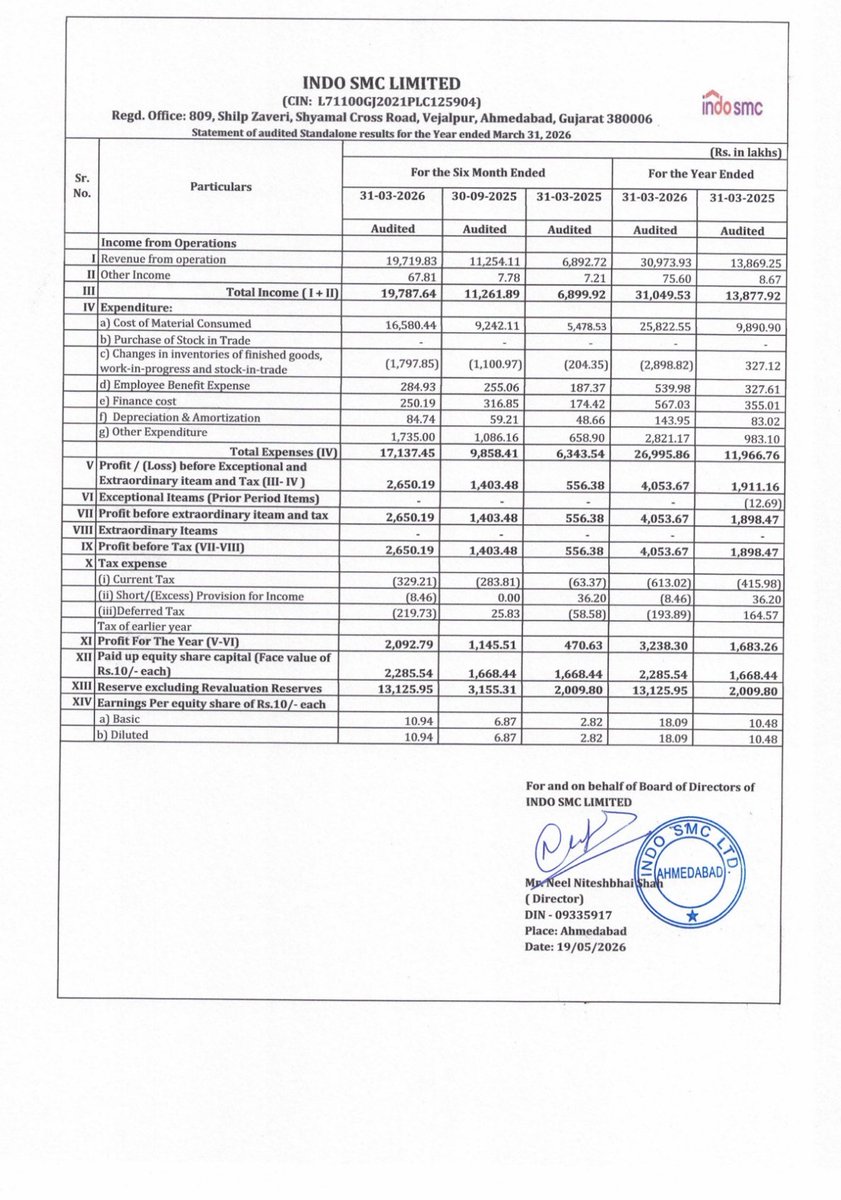

🍏INDO SMC FY26 ANNUAL RESULTS. H2FY26 RESULTS. Rs. 225 was at 27p/e. Now 16x👍

STRONG NUMBERS.👍👍 VERY GOOD. Also 25Cr CAPEX is ongoing

Company is mainly into production of Current and Potential Transformers 👍used in indoor and outdoor substations in power generation, transmission nd distribution systems. They also makes SMC boxes for meters / switch boxes and bus bar enclosures, using Sheet Moulding Compound.

H2 FY26 Vs.H1 FY26

REV:Rs. 198Cr Rs. Vs Rs. 112Cr👍

PAT:Rs. 21Cr Vs Rs. 11Cr👍👍

(May Compare with H2FY25 Rev=Rs. 69Cr & PAT=Rs. 20Cr )

FY26 Vs FY25

REV:Rs. 310Cr Vs Rs. 139Cr👍👍

PAT:Rs. 32Cr Vs Rs. 16.8Cr👍👍

INDO SMC SME IPO was in JAN 2026 at Rs.149 at 18p/e

Nilesh Kurhade@nileshkurhade

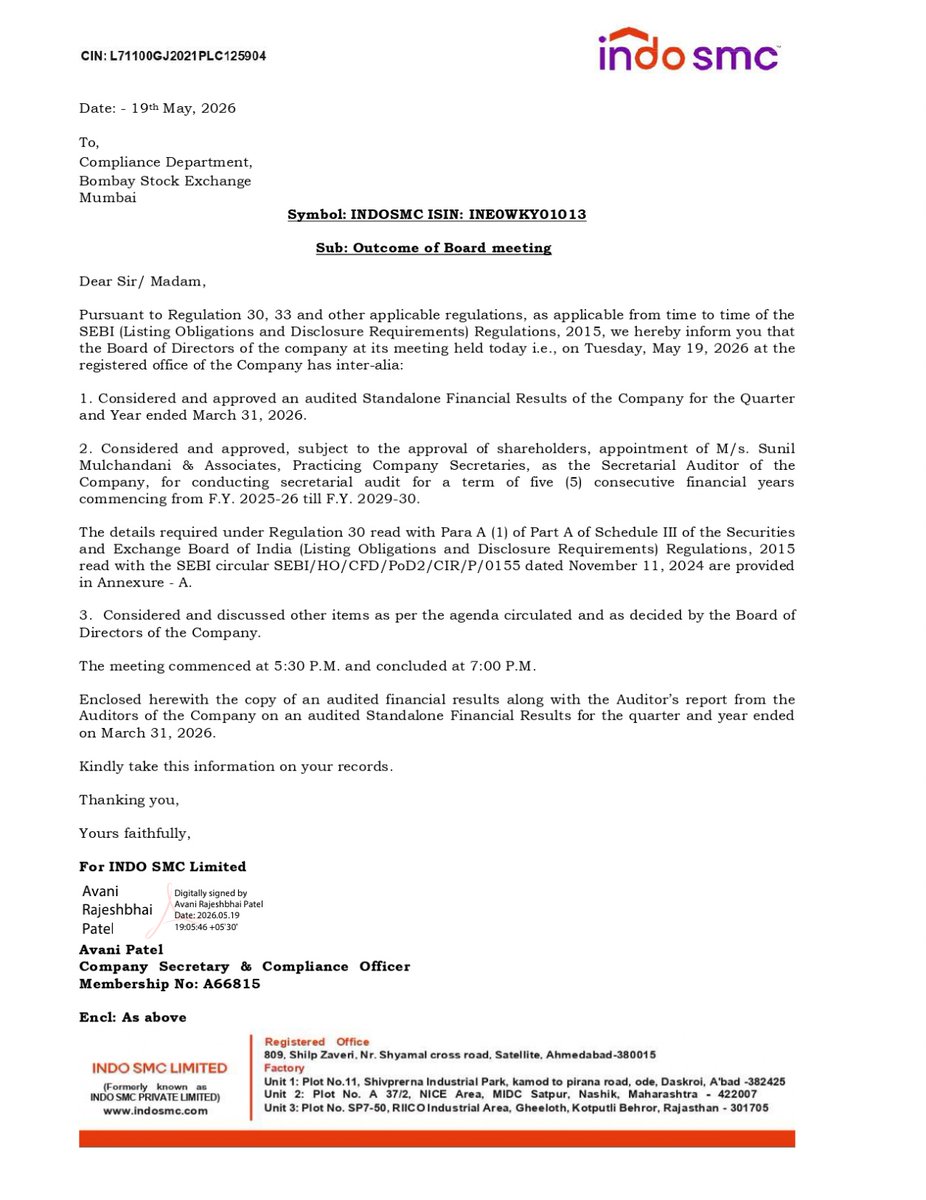

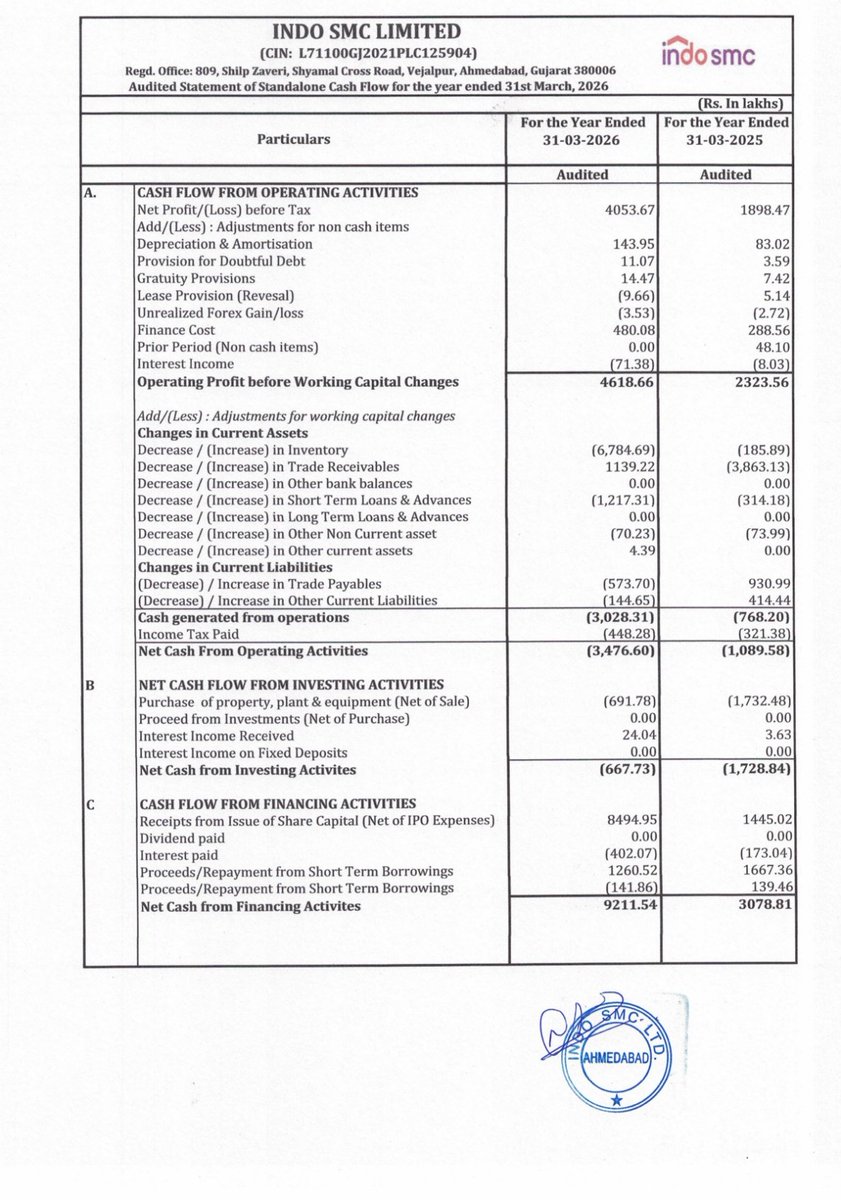

📌 INDO SMC Ltd informed the exchange about its approval for the financial results for the period ended March 31, 2026. #SME #INDOSMC 📄🧾

English

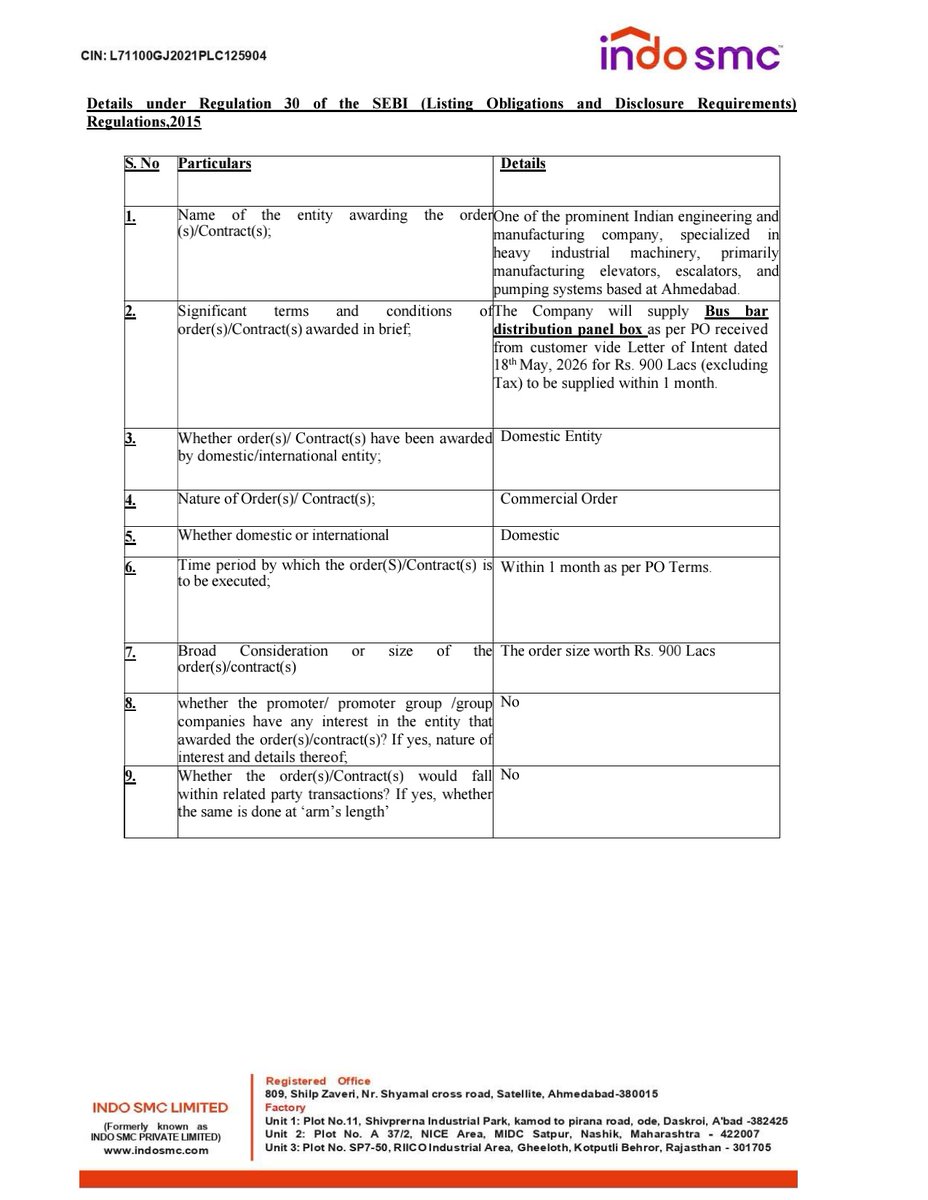

📌 INDO SMC Ltd informed the exchange about receipt of Purchase Order worth ₹900 Lacs for supply of Bus bar distribution panel box from one of the prominent Indian engineering and manufacturing company, specialized in heavy industrial machinery, primarily manufacturing elevators, escalators, and pumping systems, to be supplied within 1 month. #SME #INDOSMC ⚡📦

English

INDO SMC: Q4 SL NET PROFIT 209M RUPEES VS 47M (YOY) || Q4 REVENUE 2B RUPEES VS 689M (YOY)

INDO SMC: Q4 EBITDA 292M RUPEES VS 77M (YOY) || Q4 EBITDA MARGIN 14.79% VS 11.20% (YOY)

HT

MANGAL ELECTRICA: Q4 SL NET PROFIT 128M RUPEES VS 139M (YOY) || Q4 REVENUE 1.8B RUPEES VS 1.5B (YOY)

Español

@tushar9590 Concord Control Systems..good growing in railway electronics

English

@Rakesh_Invest Sattrix gonna shine this year

Elecon is good play in Capital Good space

Kedia sir is known for 100 beggar..that's his patience across different cycles

English

Vijay Kedia made 15x on TAC Infosec (₹106 → ₹1,671)

Now he's quietly building a cybersecurity bouquet on the SME platform.

Three positions. Same theme. All entered early:👇

- TAC Infosec — 10.95% World's 5th largest vulnerability management company. AI platform (ESOF) manages 5M+ vulnerabilities. CASA assessor for Google, Microsoft, Meta.

- TechD Cybersecurity — 5.26% Zero debt. RoCE 81%, RoE 62%. A capital-light services compounder.

- Sattrix Info Security — ~8-10% Added in Feb 2026 via preferential allotment at ₹347, near all-time high. H1FY26 profit jumped ~400% YoY. Premium 70x P/E entry.

He also added Exato Technologies — 4.71% Listed Dec 2025. AI-CX / contact-center transformation (NOT cyber).

Now here's the part most people are missing.

His older cyber bets got smashed in Q4FY26: TAC Infosec — down (48%), TechD — down (31%)

His overall portfolio is down (38%) from peak over 14 months.

What did he do?

He didn't trim. He didn't average down on the falling ones. He added two NEW names — Exato in Dec, Sattrix in Feb.

That's not panic. That's not hope.

That's a man who believes the theme is bigger than the drawdown.

His core book stays untouched — Atul Auto (20.9%), Neuland, Elecon. Precision Camshafts was trimmed cleanly when it broke down. No averaging into weakness. Classic Kedia discipline.

The pattern is hard to miss:

Small companies. SME-listed. Early entry. High conviction. Long holding period.

The same playbook that turned TAC into a 15-bagger is now being run across four names at once.

If even one of these compounds the way TAC did, the math gets very interesting.

Disc: Not advice. Just an observation worth sitting with...👀

#Investing #CyberSecurity #VijayKedia #SmallCap

English

@Rahul_Invest Am fan of Ashish sir..his investing is remarkable..am holding too Shaily since last three yrs.. multiple growth is yet to come

English

Ashish Kacholia Sir has held Shaily Engineering Plastics for over 7 years.

Stake value today: around ₹ 610 crore (5.21% with Suryavanshi Commotrade).

Why it has compounded:

Shaily makes precision injection-moulded drug delivery devices, including insulin pens, auto-injectors, and inhalers. The same product family that the global GLP-1 wave needs at scale. Pen capacity is doubling from 40mn to 80mn units by FY26 end, backed by multi-customer take-or-pay contracts. Consumer side runs on IKEA, P&G, and GE Appliances.

Numbers:

CMP around ₹ 2,557, up roughly 600% in 3 years

FY25-28E EPS CAGR forecast: 75%, with healthcare at 68%

The point is not the return. It’s the holding period. Kacholia sir bought a boring plastics company 7 years ago and stayed. The story caught up later.

Most investors would have sold it three times over by then.

@LuckyInvest_ARK

Dis : Just for educational purposes.

English

@ShridhantS KMEW is expanding its Ship Repairing/ Dredging portfolio in Middle East ..way to go

English

@samisosa1234 V Marc Cables also joining the rally..Data Centre theme supporting the business

English

Prime Cables - Up close to 50% now. Now will depend on the whether the market wants to re rate it or not.

Disc : No Buy/ Sell Advice. Has seen a solid run up. Do your own DD

Samisosa@samisosa1234

Prime Cables : Continues its journey...Hopefully the management delivers...if it does ...may see a re rating Disc : No Buy/Sell Advice. Already seen a stellar upmove

English

@RailwaySeva @drmngpsecr @wrdrmrjt PNR 8646818428, M 9650998828

Presebty also after new engine.. triam is halted before Durg since 20 Min

I am Centre Govt Employee at NTPC Ltd..had to join office , from schedule arriving time..but had to take leave..facing very bad situation

English

For necessary action escalated to the concerned official

@Drmngpsecr @Wrdrmrjt

We request you to please share the journey details (PNR/UTS No.) and Mobile No. with us preferably via DM so that immediate action can be taken on your complaint. You may also raise your concern directly on railmadad.indianrailways.gov.in or dial 139 for speedy redressal.

x.com/messages/compo…

English

@RailwaySeva @RailMinIndia

Train no. 22905 boarded from Nagpur to Raipur.. causing 2 hrs plus delay .. washroom are very dirty . engine failed near Durg.. pl resolve..very pathetic situation

English

Harsh Mamodia retweetledi

5-Min Stock Idea

Dynamatic Technologies Ltd.

Our team puts in a lot of efforts to read ARs, ppts, concall transcripts & credit rating reports to write 1-page crisp report for our community.

If you find value, plz "Retweet" to help us reach out & educate max investors.🙏

SEBI Disclosure: This content is intended solely for educational purposes and does not constitute a recommendation.

English

@WealthEnrich Coimbatore based Muruggapa Company Elgi Equipment..leading payer in industrial compressor

English

💡Decode this Stock:

50%+ Profit CAGR (5 Yr), Powering Industrial Growth, But Un-noticed for Now !

As India’s manufacturing push continues to pick up pace, sectors like industrials, construction, mining & railways are seeing steady activity. With the govt focusing on capex, localisation & production growth, demand for core industrial equipment is gradually increasing.

In almost every factory setup, air compressors act like a basic utility. It’s not a flashy product, but one that is essential across industries. This is 1 such business quietly operating at the centre of that demand.

⚙️ The company is among the top players globally in air compressors & holds a strong position in India as well. Demand is well diversified across industries, which reduces dependence on any single sector.

Revenue has grown steadily over the last few years, while profits have grown faster at ~50%+ CAGR over 5 years, showing clear operating leverage. ROCE around 22%, ROE near 20%, & margins holding in the 14–15% range. Not a high margin business, but a steady industrial compounder.

⚙️ The company has been focusing on backward integration & product development over the years, improving control over quality, costs & supply chain. This also reduces dependence on external vendors.

At the same time, newer technologies & product improvements are helping in better pricing & efficiency, which gradually supports margins over time.

⚙️ Aftermarket services & parts form an important part of the business, which typically carry higher margins compared to equipment sales. As installed base grows, this segment can contribute more to overall profitability.

Capacity expansion & investments done earlier are now getting utilised, so growth does not require very aggressive capex immediately.

⚠️ This is still an industrial business, so demand remains linked to overall economic activity. Slowdown in capex cycles or global demand can impact growth phases.

Exports & global markets also play a role, so currency movements & external factors can influence performance.

⚠️ At ~35–36x earnings, valuations are not cheap, which means a lot of the steady growth is already priced in. Returns from here will depend on continued execution.

👉 Meri Conclusive Soch:

This is very much a core industrial play linked to manufacturing & capex cycles. The experience of holding it will be more stable, but not very fast moving.

What makes it interesting is the combination of global presence, strong product positioning & gradual shift towards higher margin aftermarket revenues.

With manufacturing growth continuing over the next few years, businesses like this should keep benefiting steadily.

Yes 'Patience' is the real ask/test here!

English

@WealthEnrich AIA Engg. Monopoly type company.earlier name..Magotteaux Engg

Big Grinding roll supplier to Power industries..esp NTPC. Expanded portfolio and now in. Mining eqpt supplier has large presence in Jharkhand n Orisaa mines

English

Mining is 1 of those industries where the consumables never stop wearing out & that's why i like this company. Its major products : Grinding media & mill liners are in continuous demand & the global market is well over 3 million tons annually. High chrome technology which lasts longer & cuts costs has barely penetrated 25 to 30% of that opportunity.

AIA Engineering is the stock here we talking about which can benefit big going forward. it's Q3 revenue at ₹1,066 crore, PAT of ₹294 crore, & a war chest of ₹4,200 crore cash sitting on the balance sheet. Even after losing nearly 30% of volumes to global trade barriers & tariffs, profits have grown from ₹600 crore to ₹1,100 crore. The business is running at only 60 to 65% capacity so the operating leverage when volumes finally pick up will be meaningful.

Chile orders are now coming steadily & also Ghana + China manufacturing are being set up. Mine trial results on the new solution package are expected in the next 2 to 5 months. That is the real trigger to watch out for ! The stock has consolidated pretty well in a tight range in last 3 odd years & might be getting ready for some interesting times ahead!

#StockTowatch AIA Engineering.

English

@LearningEleven Work presented by Mr. Sagar is not less than PhD in Aerospace..big salute..Must have knowledge

English

Finally completed this wonderful podcast.

Back in the time when I was in college, NIIT used to have this caption "If you are not studying at NIIT, you are missing something".

Likewise, if you are not watching this video, you will be missing out future multi-baggers!

@soicfinance @XponentTribe

youtube.com/watch?v=YsMadW…

YouTube

English

Coimbatore-based auto ancillary riding EV shift & diversification & has given 4x returns in last 5 yrs 🚀

Guess this company!

✔️Geographical: Domestic 92%, Exports 8% (FY25)

✔️Revenue Split (H1 FY26): Aluminium Products 60%, Powertrain 27%, Industrial & Engg 13%

✔️Key Drivers: Aluminium +105% YoY (DR Axion/Sunbeam acquisitions), lightweighting for PV/CV/2W, storage solutions growth in e-commerce/pharma.

English