MFkiRani

2.5K posts

MFkiRani

@MFkiRani

Investor, Awareness. Mutual Funds/Personal Finance/ Financial Talks. Soft corner for a good sense of humour✌

India Katılım Ocak 2019

241 Takip Edilen403 Takipçiler

MFkiRani retweetledi

My year end musings. A Financial Sector Model for India’s dream: 9% annual growth, $30 trillion GDP by 2047.

India is transforming from a nation of savers to investors. The tussle between the saver/ borrower and issuer/ investor model is underway.

In the early 80s, the Indian saver had low confidence in financial assets versus gold and land. Slowly the saver moved some part to bank deposits, UTI and LIC.

Even in the 90s, investing in equities was considered “speculative”. Hence companies looking for capital went to the foreign institutional investor (FII). FIIs saw potential and bought into companies while the Indian saver stayed away. Companies raised capital through the less known Luxembourg stock exchange. India’s capital market was being exported.

Some of us highlighted this phenomenon to SEBI. That began the private placement market (QIP) in early 2000s. Hence FIIs could also buy on Indian markets. The Indian saver’s interest in markets improved after the global financial crisis.

That saver is now savouring the joys of investing. Mutual fund platforms, cash equities and derivatives markets, insurance funds, global private equity in India, other platforms like AIFs, lower tax regime for equity, have all converted a saver to an investor.

How do we create a sustained growth story hereon?

1.Many investors have joined post Covid. They have mainly seen upside. While the situation is not comparable at present, we need to keep Japan of the 80s at the back of our mind. Its Nikkei Index peak was 1989. 34 years later with near zero interest rates, the Nikkei is still below its 1989 peak. We must avoid bubbles through policy, regulation, education, and supply of quality paper. Companies should raise equity at lower cost of capital for productive use.

2.While we must avoid tax arbitrage in debt, unless debt markets grow it will be a one legged race. The current gap on highest marginal tax rate between debt and equity of 39% and 10% is perhaps too wide.

3.Double taxation on dividends needs relook. A shareholder is like a partner. There is no additional tax when money is moved from the partnership to the partners capital account. Same principle applies to shareholders.

4. Low cost leverage through derivatives can distort financial markets. This needs attention.

5.As savers become investors the banking sector faces challenges on its deposits and cost of funds. The large corporate sector has to meaningfully move to capital markets (debt and equity) and away from banks. Banks will become distributors of corporate debt rather than storage houses. They will need to penetrate mid sized corporates, MSMEs and consumers.

6. We should avoid a retrospective tax and regulatory regime. We will need to balance developmental and regulatory role.

7. Two areas which need urgent focus for India’s aspiration are acquisition financing and streamlining of the IBC/ NCLT process.

As India aspires, the financial sector will be the key engine for delivery. Impact of technology is a separate subject of discussion for a future date. The saver/ borrower and the issuer/ investor models will coexist. It is time for a wholistic financial sector view.

English

MFkiRani retweetledi

Sometimes married couples buy properties or investments in the name of the spouse with lower income-tax brackets. But that could land you in trouble.

The @IncomeTaxIndia says that whoever earns the income, must pay tax on investment made from that income.

English

MFkiRani retweetledi

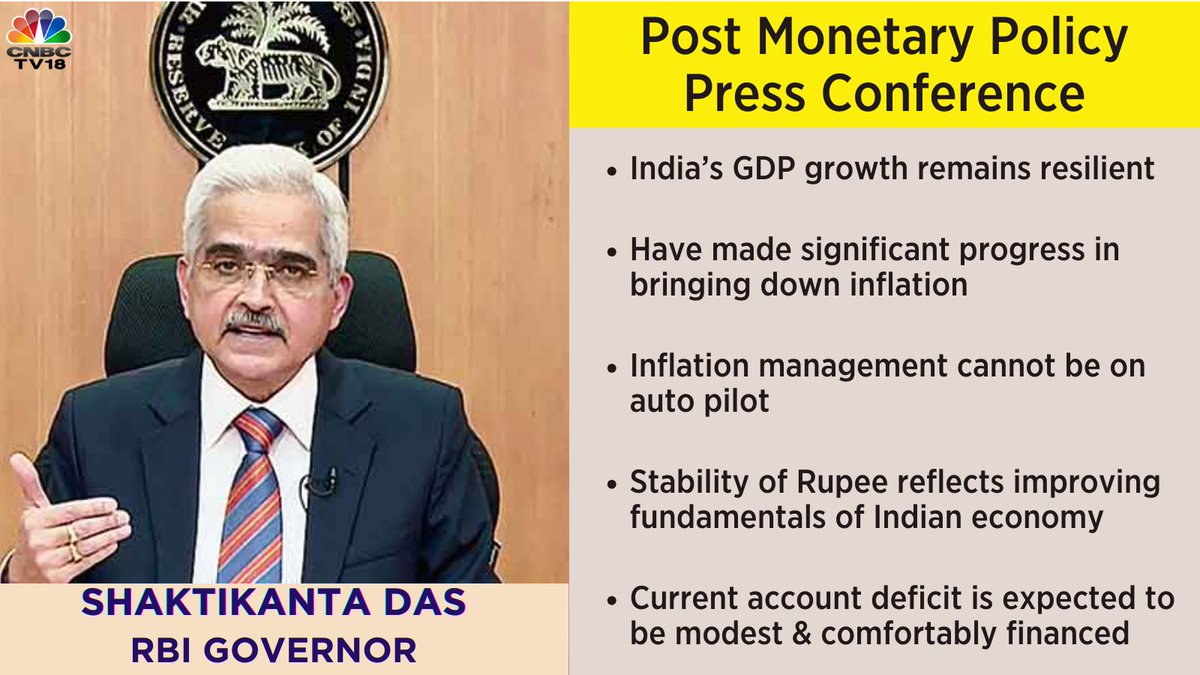

#RBIMonetaryPolicy | @RBI’s Monetary Policy Committee keeps the #RepoRate unchanged at 6.5%.

Here's how the equity markets reacted⬇️| #RBI @senmeghna

cnbctv18.com/market/stock-m…

English

MFkiRani retweetledi

#Inflation management cannot be on auto pilot. Current account deficit is expected to be modest & comfortably financed, says @RBI Governor @DasShaktikanta in the Post Monetary Policy Press Conference

#RBIPolicy #RBI #RBIMPC #RBIMonetaryPolicy

English

#NFOAlert @livemint @SAMCO_India

Dynamic Asset Allocation Fund

Opens Dec 07 closes Dec 21

livemint.com/money/personal…

English

“Invest for the long haul. Don’t get too greedy and don’t get too scared.”

#ShelbyM.C. Davis #ThursdayMotivation

#ThursdayThoughts

English

MFkiRani retweetledi

While all are talking about the roaring Equity markets, Gold has silently hit the all time high.

Lets discuss what’s moving the gold prices in this 🧵

Do hit the ‘re-tweet’ and help us educate more investors. (1/8)

English

It's not whether you're right or wrong that's important, but how much money you make when you're right and how much you lose when you're wrong. — George Soros

#tuesdayquote #investment

English

MFkiRani retweetledi

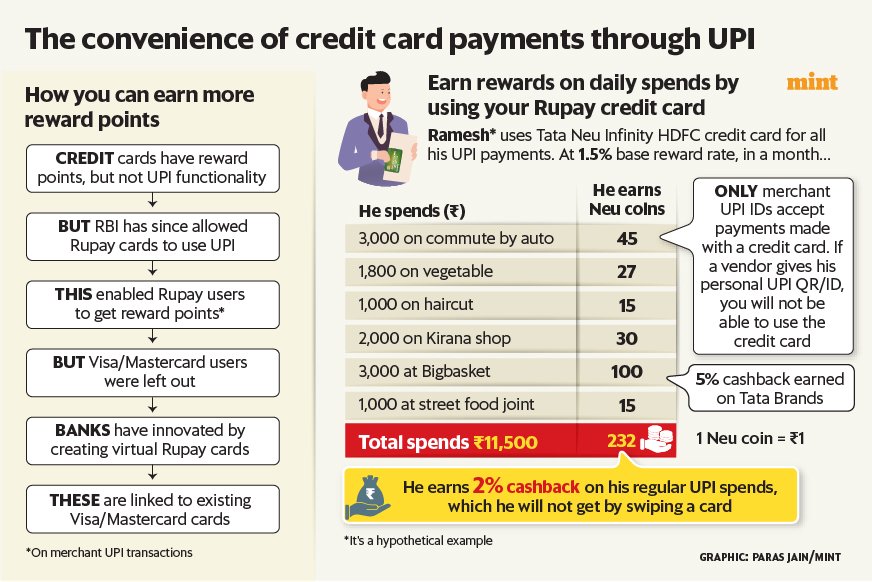

Use UPI a lot and miss credit card reward points? Don't worry, banks are creating 'virtual' Rupay cards connected to your existing card. Why? It allows you to use credit card linked UPI at small merchants without PoS gadgets. Story by @Shiprasorout. livemint.com/money/get-rewa…

English

MFkiRani retweetledi

MFkiRani retweetledi

MFkiRani retweetledi

MFkiRani retweetledi

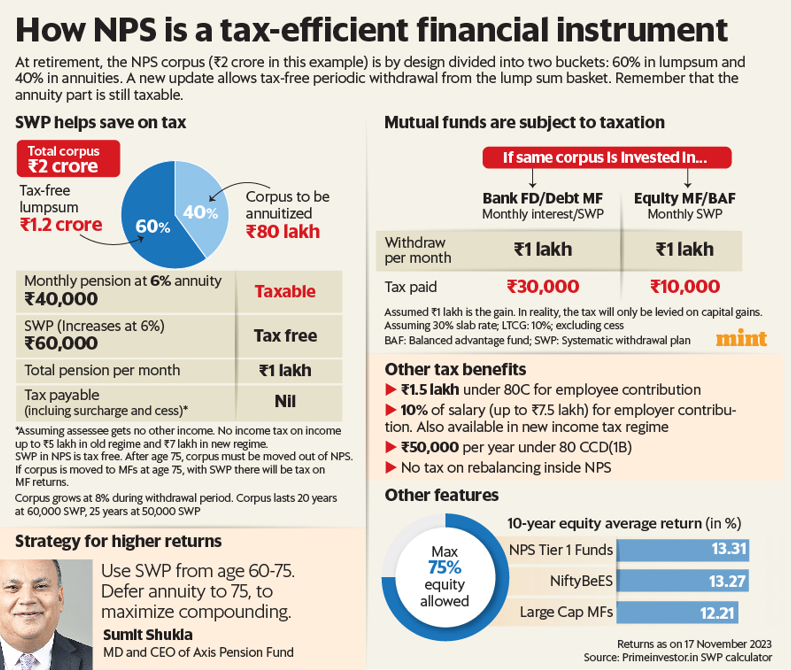

SWP in NPS is a game changer. Why? SWP + annuity can give a tax-efficient pension (see example).

To those who complain about annuity, @sumit0409 has a simple solution - postpone it till age 75. Let your money sit in NPS longer and compound. After 75, annuity rates shoot up (for annuity for life).

To those who say midcap/small cap stocks/MF will do better this is not either/or. You can pair NPS with MFs. Unless you want 100% in mid and small - best of luck with that. Story by @sashindnj

livemint.com/money/personal…

English

MFkiRani retweetledi

MFkiRani retweetledi

MFkiRani retweetledi

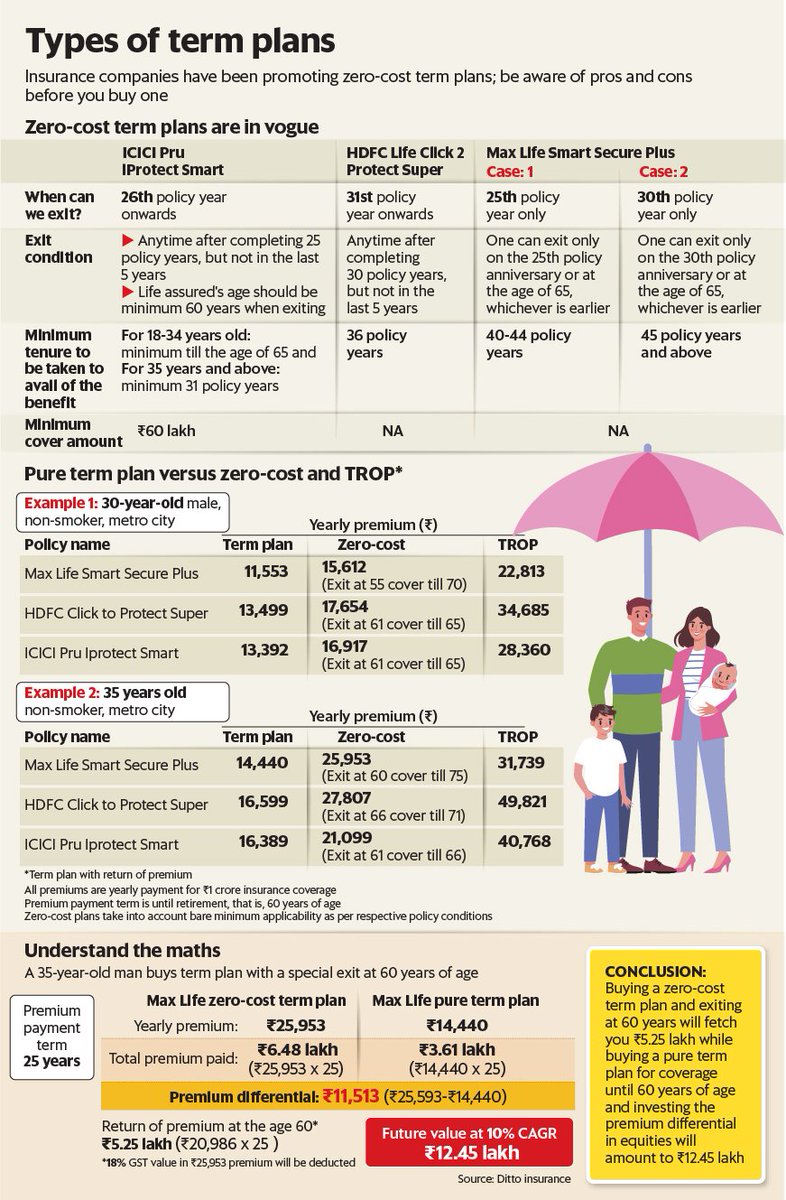

Today @apri_sharma shows why a simple term insurance policy is better than the bells and whistles that marketing throws at you such as zero cost/return of premium term plans livemint.com/money/personal…

English