Sabitlenmiş Tweet

🚨BREAKING: US consumers are falling behind on debt at an alarming pace.

Credit card serious delinquencies jumped to 13.1% in Q1 2026, the highest level since Q4 2010 and just below the post-2008 Financial Crisis peak of 13.7%.

Since Q3 2022, serious credit card delinquencies have surged +5.5 percentage points, an even steeper deterioration than the +3.9 point rise seen during 2007-2010.

Meanwhile:

• Student loan 90+ day delinquencies rose to 10.3%, the highest since 2020

• Auto loan serious delinquencies climbed to a record 5.6%

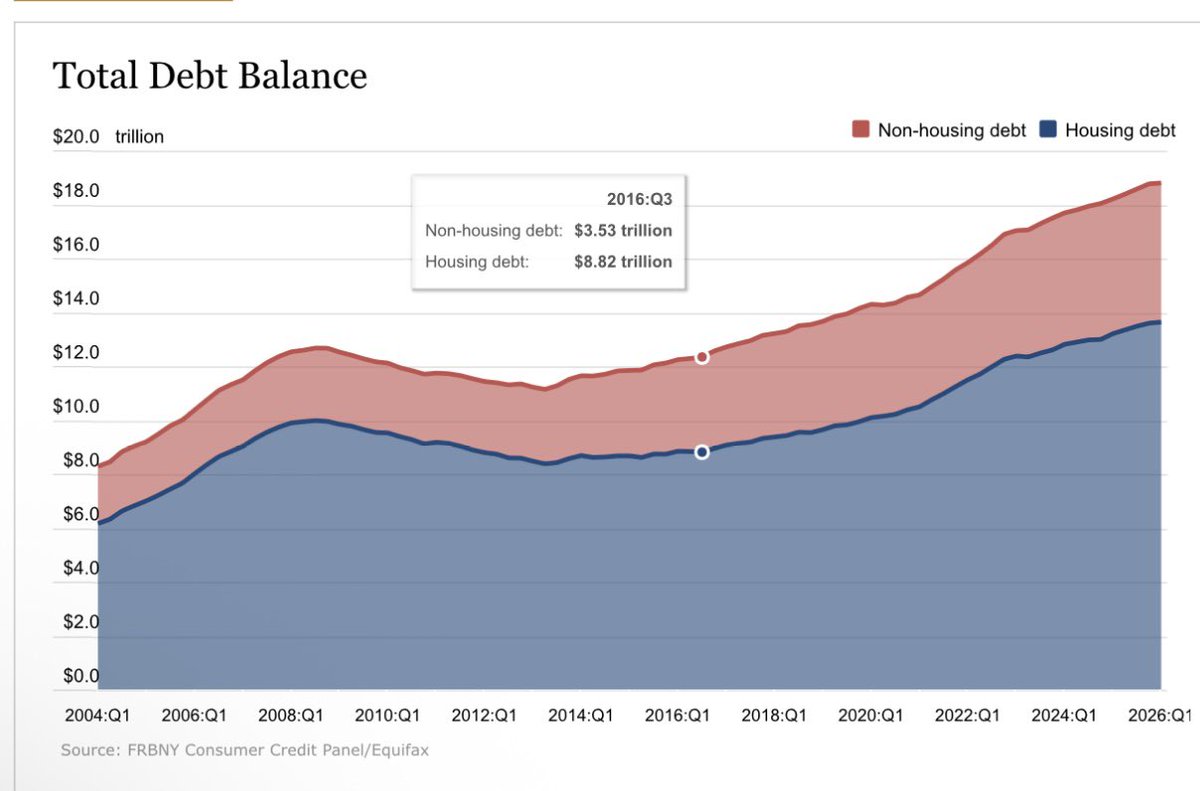

• Total US household debt remains near a record $18.8 trillion

• Personal loan balances hit an all-time high $277 billion in Q1 2026

• Subprime auto delinquencies recently hit the highest level in over 30 years

The troubling part is that this is happening while unemployment is still relatively low.

Consumers are increasingly relying on credit just to maintain spending levels as elevated interest rates, inflation, rent, insurance, and car payments continue squeezing disposable income.

This no longer looks like “normalization” after stimulus-era spending.

It looks increasingly like balance sheet exhaustion.

Recent New York Fed and TransUnion data support the acceleration in delinquencies and household debt stress.

English