The number of officials seeing upside risks to inflation is now greater than it was at the peak of the inflation crisis—a detail that markets seem all too eager to brush aside. The disconnect between Powell’s rhetoric and the broader FOMC stance is striking.

Traditionally, escalating trade tensions would drive demand for the Greenback as a safe-haven asset, but investors are now looking beyond short-term flows and focusing on the economic damage these tariffs could inflict. Higher volatility = lower dollar.

If the greenback’s slump reflects eroding trust in Trump’s economic agenda, could his approval ratings be next in line for a drop? With trade tensions rising and investors reassessing his second-term outlook, it’s a risk worth watching.

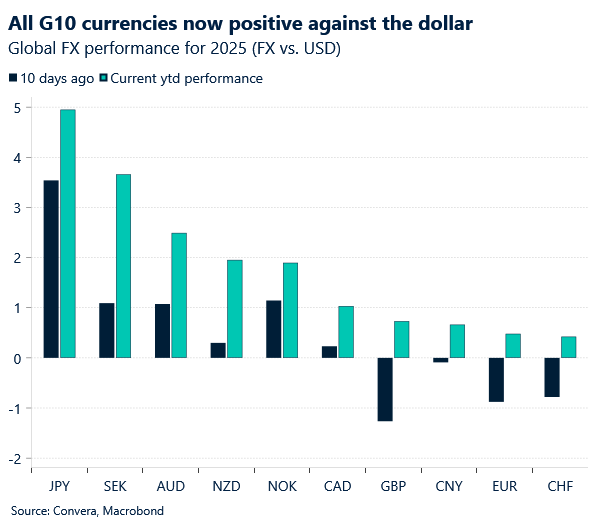

The US dollar is having a bad start to the year due to 1) signs mounting that the US economy is losing momentum and 2) the lack of tariffs so far. Every G10 currency is up against the Greenback ytd.

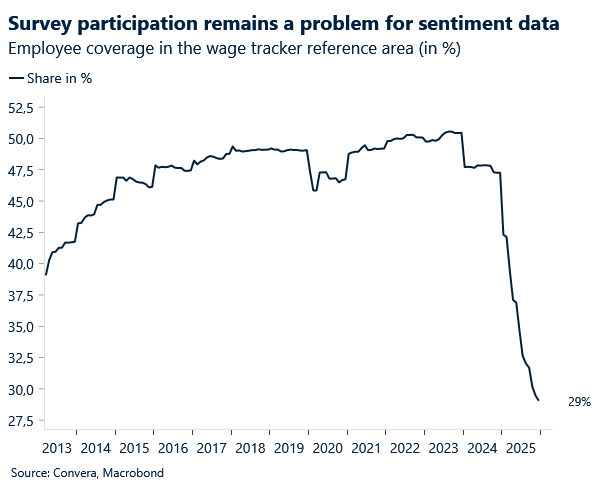

Side note: Low participation rates in sentiment-based surveys remain a persistent weak spot, a trend not just in the Eurozone but also in the US. Does this affect the predictive power of wage models? Unclear—but something worth watching.

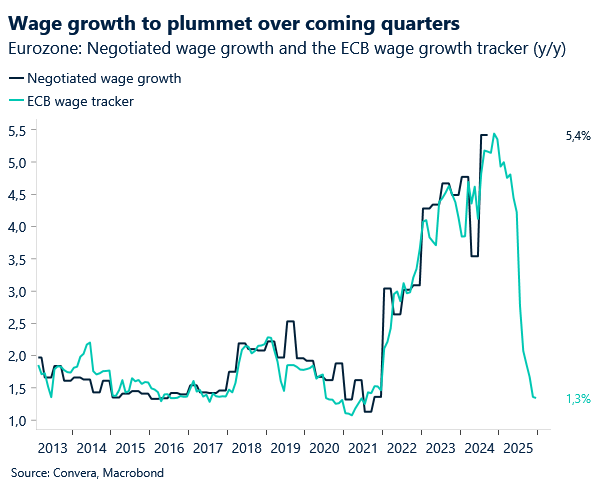

One concern the ECB likely won’t have to grapple with is wage growth. While currently running above 5%, a pace last seen in the mid-1990s, both the Indeed and ECB wage growth trackers point to a sharp slowdown in the coming quarters.

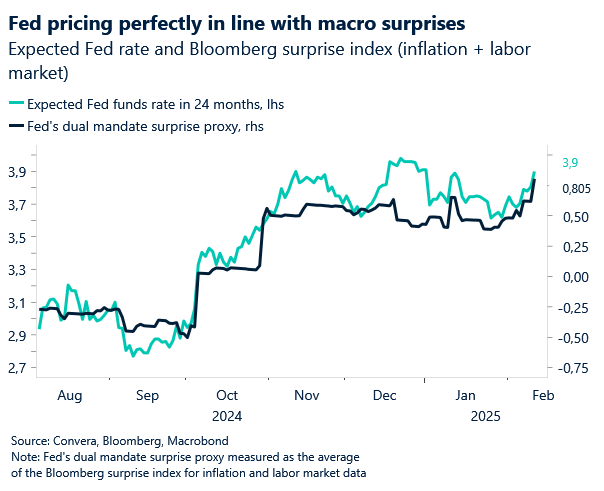

Yesterday’s upside surprise in US inflation has significantly dampened expectations for a Federal Reserve rate cut in the first half of 2025. The latest inflation data came in stronger than anticipated, reinforcing concerns that price pressures remain persistent and forcing markets to reassess the timing of monetary easing. In response to the inflation beat, our Fed Dual Mandate Pressure Index surged to its highest level in 10 months. This also explains the recent shift in Fed pricing, as markets increasingly align with the view that rates will stay higher for longer. Fed officials have maintained a cautious, data-dependent approach, and yesterday’s numbers only strengthen their case for patience. With inflation showing signs of renewed momentum and the labor market holding firm, the bar for rate cuts remains high.

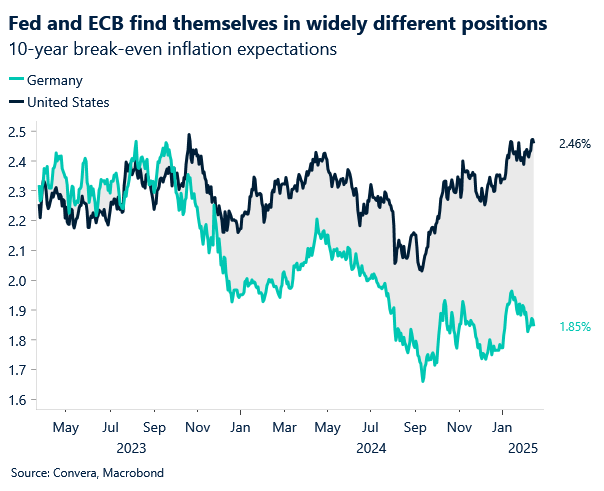

When it comes to EUR/USD, it is important to note that US market-based inflation expectations have been trending higher for a while now, with some tenors (5-year) hitting their highest level in years. This is theoretically dragging down the real rate differential between the US and Europe and could help solidify a bottom for the common currency.

Today's dollar depreciation despite the inflation beat confirms our asymmetric reaction function and geopolitical dominance thesis.

The US dollar weakened today against the euro, even as US inflation came in hotter than expected and Treasury yields climbed across the curve. Markets reacted to the upside surprise with a pullback in Fed rate cut expectations, now pricing in just one cut for the year. However, the dollar failed to capitalize on the shift, confirming its asymmetric reaction function. Instead, geopolitical optimism took center stage. Reports emerged that President Trump may be actively working on a peace deal with Ukrainian President Zelensky and Russian President Putin. This boosted risk sentiment, lowered oil prices, and therefore overshadowed Fed repricing, putting pressure on the Greenback. Today's market action aligns with our view that, for now, positive geopolitical developments hold greater sway over FX markets than concerns about the Fed delaying rate cuts. If this trend continues, the dollar could remain vulnerable despite resilient US data.

The only interesting thing about yesterday's NFIB release was faltering concern for credit conditions despite the Federal Reserve's cutting pause. Historically, tighter credit expectations have led bankruptcy filings by about a year, but with small business sentiment on lending conditions stabilizing, the worst of the bankruptcy cycle may already be behind us. That doesn’t mean risks have vanished—elevated rates and slowing growth could still weigh on smaller firms—but the data suggests we may not see another major wave of business failures. Is this just the Trump effect working its way through the sentiment data or is it a real signal?

As we’ve previously argued, further dollar upside depends on a sustained trade escalation and actual tariff implementation. With the Fed pause fully priced in, the dollar now requires either a stronger US macro backdrop or deteriorating risk sentiment to advance meaningfully. Both are not unlikely but are partially priced in. This gives us an asymmetric reaction function weighted to the downside for the dollar over the next 12 months. However, for now, the high noise-to-signal ratio makes shorting the Greenback a difficult case to justify.

Inflation still the priority, not jobs

1. January’s US jobs report delivered a mixed bag for investors. Hiring slowed but wage growth ticked higher and continued the theme of “heightened inflation anxiety” driven by the tariff war and rising inflation expectations. The macro and geopolitical ambiguity was enough to drive the dollar higher before the weekend, but the gains were unable to turn the overall week green.

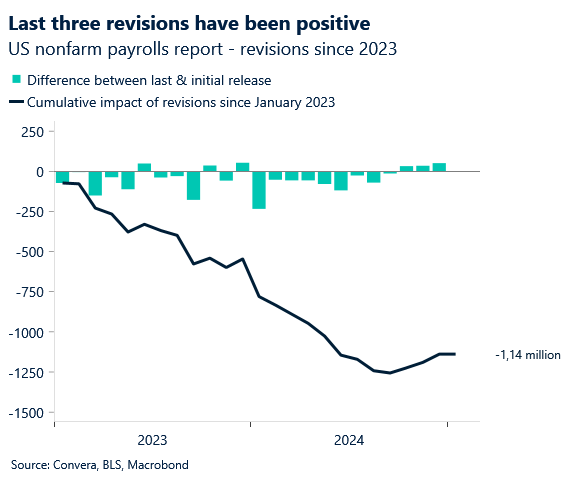

2. Headline payrolls came in at 143k, below the 175k consensus. However, upward revisions to the past two months added 100k jobs, and the unemployment rate held at 4.0% versus the expected 4.1%. Wage growth remained strong, with average hourly earnings rising 0.5% month-over-month, but the average workweek fell to 34.1 hours, matching pandemic lows.

3. These factors support the case for the Fed to hold rates steady for now. Options markets now reflect only two rate cuts from policy makers during the current easing cycle.

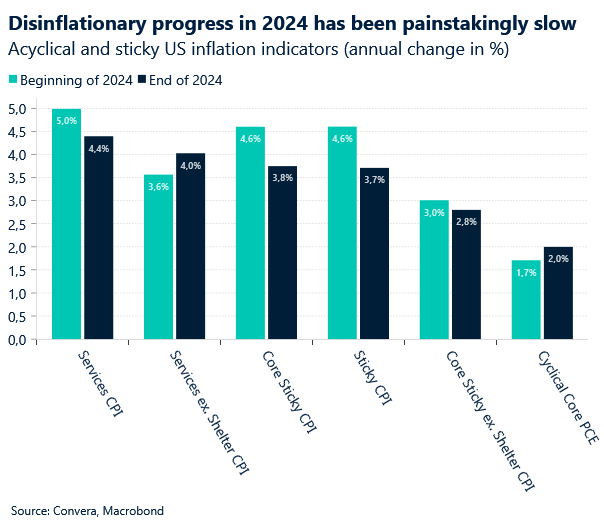

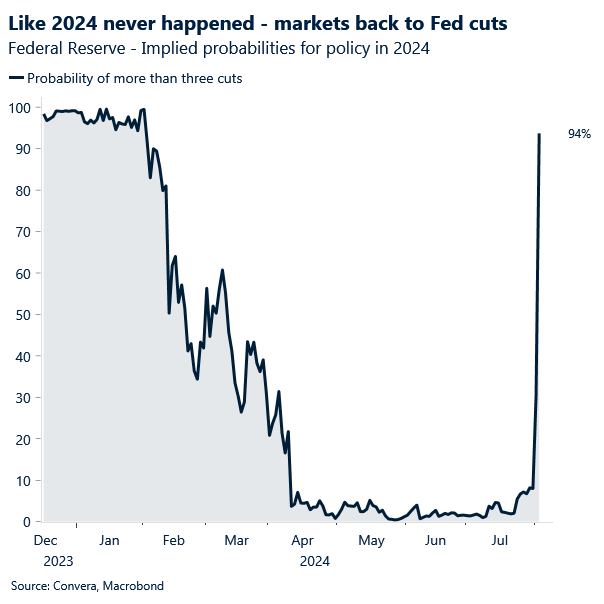

Murky inflation outlook. Fed Governor Waller's dovish comments this month sparked speculation about rate cuts in 2025. Powell dispelled them. Inflationary pressures remain, with signs of a slow return to disinflation. Market expectations for a 2% inflation rate this year may be overly optimistic. (10/10)

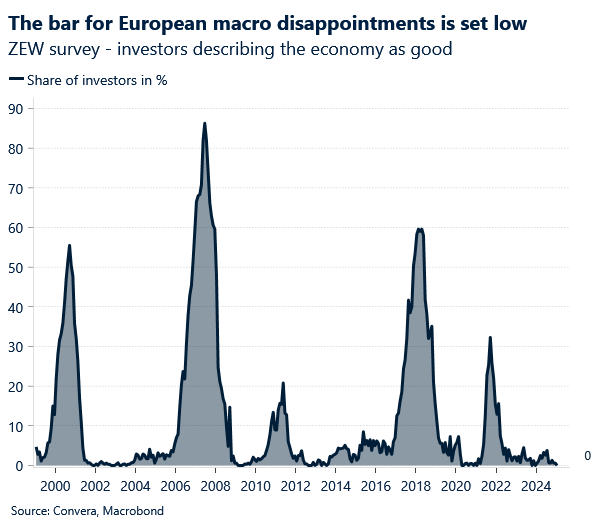

Europeans at peak pessimism. Despite fears of recession and weak growth, much of Europe’s negative outlook is already priced in. Positive surprises in data could lead to a strong market response. A modest rebound in consumer spending or business confidence could drive a market shift. (9/10)

The Trump effect. My ten charts of the month.

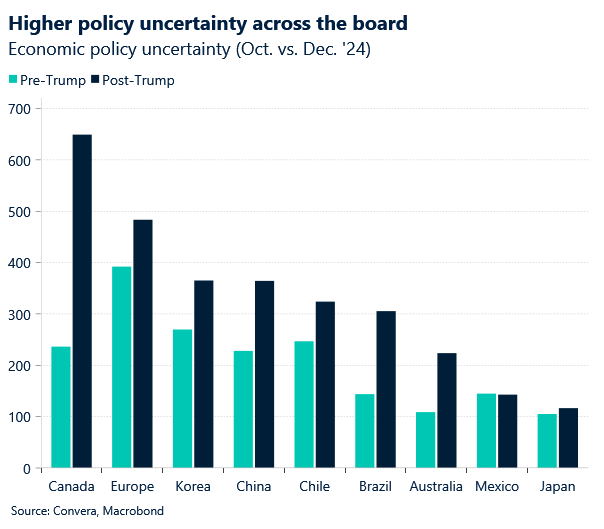

Trump's uncertainty shock. Under Trump’s leadership, global policy uncertainty reached new heights, influencing market movements. Europe faces growing challenges with shifting alliances and heightened uncertainty. The unpredictable policy landscape has investors on edge. (1/10)