Sabitlenmiş Tweet

From the outside, your business may look solid.

Inside, the whole financial picture lives in your head.

What’s safe to pay yourself.

What you owe in taxes.

What’s sitting in savings.

What debt is creeping up.

What insurance is missing.

What happens if one bad month hits.

That works for a while.

Until April punches you in the face.

..or payroll gets tight.

..or you realize you’re making decisions from memory instead of numbers.

That’s the trap for a lot of owner-operators.

Not failure.

Fog.

You’re busy.

Revenue is moving.

But the picture is blurry.

And when the picture is blurry, every decision can feel heavier than it should.

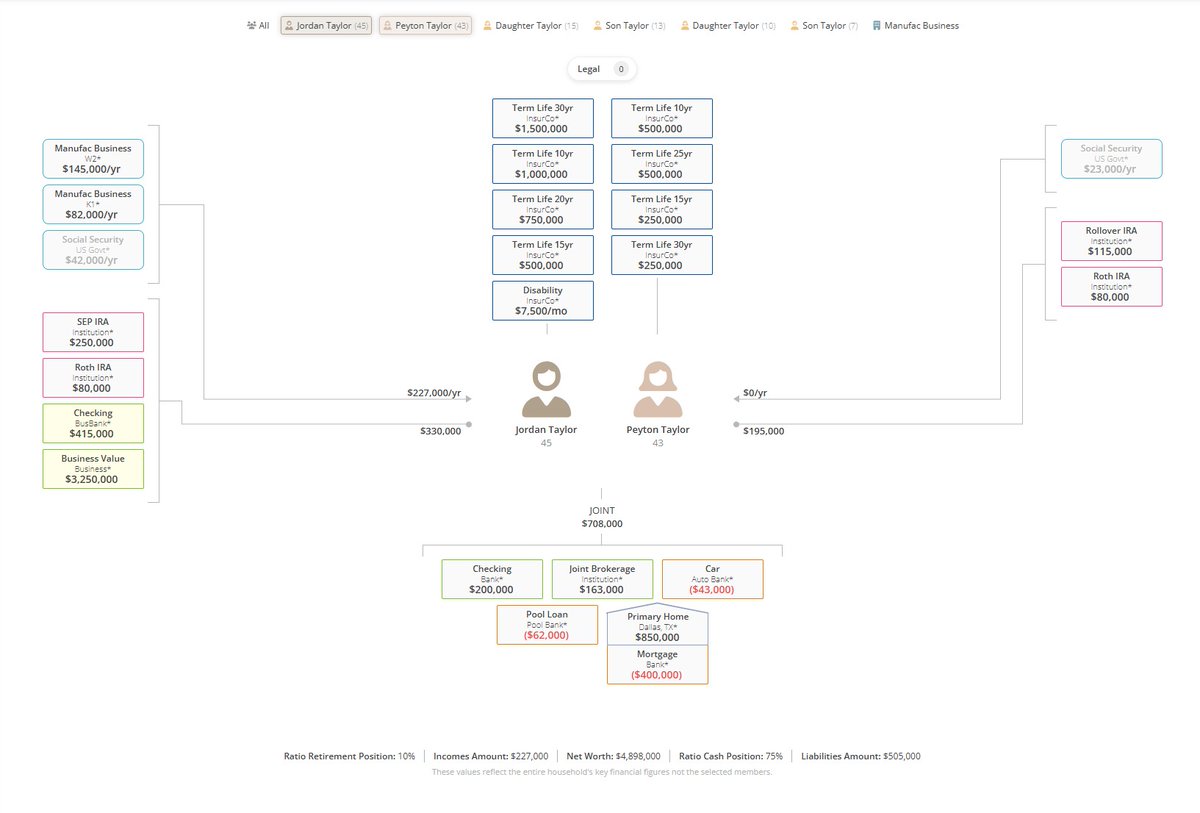

An Asset-Map helps get it out of your head and onto one page.

So you can see:

- what you own

- what you owe

- how everything connects

And if you can see where everything is, you can start to see where the gaps are.

Not in five tabs.

Not in your notes app.

Not in the running spreadsheet in your brain.

On one page.

Because clarity changes how you decide.

What to keep.

What to fix.

What to protect.

What you can actually afford to do next.

There’s an example attached so you can see what an Asset-Map looks like.

If you’re an owner-operator and you want a clearer view of your financial life, start your free Asset-Map here:

app.asset-map.com/i/OaVVwLaQ

You can get a working picture in as little as five minutes.

-----

👇 Regulatory stuff 👇

2751 Teakwood Ln Plano TX 75075

Securities offered through Cetera Wealth Services, LLC, member FINRA/SIPC. Advisory Services offered through Cetera Investment Advisers LLC, a registered investment adviser. Cetera is under separate ownership from any other named entity.

English