Mbarry58

292 posts

We're launching an initiative at Figure and looking for a senior (C-level) marketing professional to help in what we're doing. Think of it as an independent startup within the company, and an AI-centric effort across all facets of the business - product, engineering, legal, finance...and marketing.

I'm posting what we're looking for below. If you (or someone you know) fits the bill here, please reach out to me with a CV.

- Success marketing traditional finance and/or blockchain products to retail and institutional investors

- Strong understanding of AI in marketing, including content creation, contextual outreach, social management and channel optimization

- Solid grounding in and belief of self-custody, distributed applications versus fintech super apps

- Hands on player/coach comfortable working with a small, nimble team in a 0 to 1 startup environment

- Experience managing mobile application app store processes

- Strong media relationships with proven track record of managing earned and paid media

- Successful background that should include some combination of fintech, online banking/payments, investing, DeFi, crypto and AI

English

Ok - a few years back, we launched a SPAC - FACA. At the time, the SPAC market turned south, and while we had some interesting acquisition targets, we felt any transaction would not hold the $10 par value and chose to return the capital rather than launch a deal where we got paid but investors lost money. Ironically, I think that made us one of the better performing SPACs in that peer group.

We are considering trying this again. The idea would be to launch a SPAC that could acquire an entity that could derive significant enterprise value from some combination of Connect, Democratized Prime and YLDS. That could be an asset originator that can benefit from the Connect/Democratized Prime capital market, a fintech that could swap its ledger to YLDS, among others. And of course, we'd dual list the SPAC and the resulting company on OPEN.

The goal here is to triple dip. We can make money for Figure shareholders on the SPAC economics, we drive more usage on the Figure ecosystem and we get another listing on OPEN.

While I like the idea, we also have a lot going on, and we are executing in rare air - 100% growth rate, 50% EBITDA margins - blowing way past the "rule of 40". I'm curious what the X universe thinks. Let me know below...

English

@mcagney $figr - mike I like the idea. I’d say quality of acquisition and loan or asset book quality of what u acquire matters far more than size. Directionally a size increase is in multiple avenues is still positive but lowering overall product / book quality would be a huge story drag

English

@BlueBird_Invest Heck yes. The year over year will be huge for $figr if month to month is that strong

English

$FIGR Accelerating the destruction of antiquated lending platforms. First a nibble, then the collapse. $2 trillion annual TAM - FIGR $10 bill run rate growing 30% and increasing. 🚀

Aayush Shah@aayushtrades

$FIGR figure heloc book +$830.9M qtd in q2 so far (28 days in) running $29.7m/day vs q1's $20.5m/day. this is about a 45% faster daily pace in raw dollars and base adjusted growth of ~30% this is net book growth not clmv so its not exactly what the company releases but gives you an idea of momentum

English

@aayushtrades Not worried!!!! Long and strong. $figr. When fundamentals outpace price….more time to build a bigger stack for the run!

English

$FIGR

insane that it's in the low 30s again despite all the on chain data looking stronger than ever

English

Mbarry58 retweetledi

@aayushtrades $figr is getting some love from the haters - “shoot I missed the base and now need to cause fear for a pullback so I can go long” figr is beyond differentiated from anything else in the market

English

to those comparing $BETR to $FIGR:

$BETR is essentially just a nice ui sitting on top of the exact same legacy mortgage rails that everyone else uses. all other lending companies basically do that same model. anyone with enough funding can write software to originate loans and buy growth. the problem is they still have to rely on expensive warehouse lines of credit to fund those loans and then deal with weeks of settlement delays to sell them on the secondary market. all those layers of middlemen eat the margins which is why they are burning tens of millions in cash just to push volume. reason they are growing 100% YoY is because they were literally about to die and coming off a really low base and decided to slap AI on their product lol

$FIGR is fundamentally different because they are a blockchain company reinventing the entire backend infrastructure. every loan they originate is minted directly on the provenance blockchain. by putting the asset on a distributed ledger they completely eliminate the need for third party custodians trustees and title intermediaries. settlement happens instantly.

that backend is incredibly hard to replicate. you cannot just sign a partnership and spin that up. it takes years to build the infrastructure get the regulatory approvals and actually convince massive institutional buyers to transact on a blockchain ledger.

on top of that infrastructure moat they built figure connect which is a marketplace that routes loans directly from originators to capital market buyers. and now they are taking it a step further by tapping into defi liquidity pools to fund loans.

one is burning cash to acquire customers on an outdated system and the other actually fixed the plumbing to change the unit economics of entire asset classes

English

$FIGR

all the people will start talking about figure again once there is a bit of momentum

already seeing more tweets

remember who was there tweeting during the darkest of days

English

@aayushtrades Haha!! U had me dude :). Was shocked given this names potential and material progress

English

@aayushtrades This feels like a huge volume are waiting given general market weakness to try and get sub 30s here. 30s seem way stronger than last time we were here. Won’t shock me if this starts running up we get a big volume surge

English

$FIGR

25k shares just dropped it a dollar??

wow

another super low volume day. no liquidity in this stock

English

Mbarry58 retweetledi

@zoozai_invest March was first month with over $1B in originations - but to say Jan and Feb were stagnant ignores the seasonality aspect - seasonally they were both strong months, but March really showcased the value of over 300 origination partners.

English

@zoozai_invest U thinking fundamentally bullish or just interesting item to watch?

English

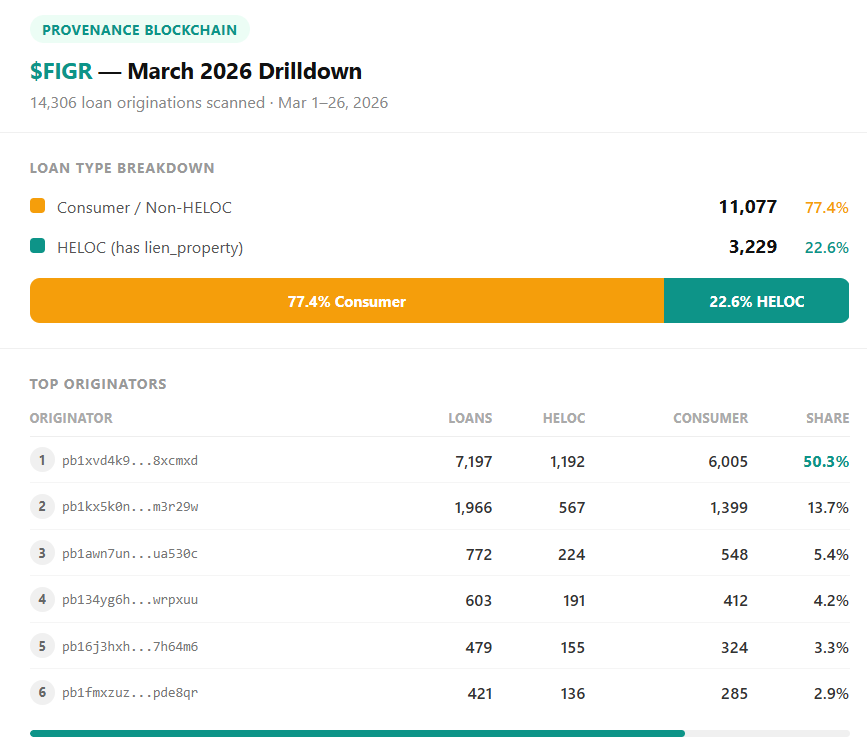

Drilling down some more into $FIGR March on-chain data.

The most obvious finding:

~77% of loan originations are not HELOCs.

How do I know?

(loan data and PII are stored off-chain and are not accessible to public)

Every mortgage transaction on Provenance includes a lien_property record (the collateral).

No lien_property = consumer/non-HELOC loan.

This 75-25 split is almost the inverse of what we saw in 2025 data. Would be interesting to see the shift month over month.

Another item that popped right away - originator concentration.

Top 1 address controls 50.3% of all March originations

Top 5 control 77% combined

Are new originators showing up? Are some fading out?

Will be looking into that as well.

More to come.

English

@zoozai_invest Yesss!! Ty for putting this together. The story is here and it’s great but sometimes the flow of info is hard to get in robust detail. Appreciate the $figr community here!

English

Things are clearing up in the analysis of $FIGR's transactions on Provenance Blockchain.

Just a sneak peek regarding accurate loan origination numbers across the last two years.

Although past 9 months have been quite stagnated, March seems like the first real growing month.

Working on a deeper dive for March to see the breakdown of the loan characteristics, hopefully this will shed more light.

Stay tuned.

English