Mk

665 posts

قال وزير الخارجية الإيراني الأسبق والبرلماني الحالي، منوشهر متكي، موجهًا حديثه إلى البحرين: "نحن الآن في وقت وقف إطلاق نار، فادعوا ألا تندلع حرب، فإذا اندلعت الحرب وأعدتم استخدام القواعد الأميركية ضدنا، فسوف نضربكم بشكل يجعلكم تنسون أسماءكم، وسنحوّل تراب بلادكم إلى رماد".

وأضاف متكي أن البحرين وبعض دول المنطقة سهّلت الهجمات على إيران من خلال توفير إمكانات وقواعد للولايات المتحدة، وأنها بعد الهجمات الأميركية والإسرائيلية لم تُبدِ التعاطف مع إيران بعد مقتل علي خامنئي، بل عملت على تحريك الولايات المتحدة لإصدار قرار ضد طهران في مجلس الأمن.

كما قال إن البحرين حاولت طرح قرار ضد إيران في اجتماع الاتحاد البرلماني الدولي في إسطنبول، لكن طهران، عبر "حكمة دبلوماسية" وبمساعدة بعض الدول، منعت التصويت عليه.

وأوضح متكي أن هذه التصريحات تأتي في سياق روايته الجديدة لجدل لفظي مع الوفد البحريني في اجتماع الاتحاد البرلماني الدولي في إسطنبول، مشيرًا إلى أن ممثل البحرين كان قد اتهم إيران بـ "الهجوم الظالم" على بلاده والدول العربية، فرد عليه بهذه العبارات في ذلك الوقت.

iranintl.com/ar/202605149101

العربية

عباس مقتدایی، نایب رئيس لجنة الأمن القومي في البرلمان الإيراني: "نحن نملي على أمريكا وحلفائها ما نشاء، لأن السيادة على الخليج، ومضيق هرمز، وبحر عمان، مسألة جوهرية وملك لدولتنا".

العربية

وفقاً لما نقلته بعض وسائل الإعلام الإيرانية المقربة من محمد باقر قاليباف، ضمن ما وصفته بتسريبات من محادثات جرت في إسلام آباد، على لسان محمود نبويان المقرب من قاليباف؛ دار حديث بين رئيس أركان الجيش الباكستاني عاصم منير وقاليباف مع جي دي فانس، حيث أفادت الرواية بأن قاليباف رفض مطلباً يتعلق بفتح مضيق هرمز، محذراً من أن أي استهداف للبنية التحتية الإيرانية من قبل الولايات المتحدة سوف يقابله رد يستهدف كل البنى تحتية في المنطقة.

العربية

الخارجية الإيرانية: نؤكد على ضرورة تأمین وصول سفارتنا في الكويت للرعايا الإيرانيين المحتجزين ونطالب بالإفراج عنهم فوراً

العربية

@StockSavvyShay @FuturumEquities you really do NOT give it justice. Some companies have such a distorted net income due to non operating items and you do not even allude to it.

English

This is Peter Lynch’s favorite metric and I like it too because it ties valuation to growth. I prefer using a 2026 to 2028 window so the multiple adjusts for how fast the business is actually compounding.

For example $AAOI may trade at ~80x forward earnings but earnings are expected to grow from $0.88 in 2026 to $4.83 in 2028 implying a ~134% earnings CAGR and a PEG of ~0.6x.

English

SEMICONDUCTOR STOCKS BY PEG RATIO

PEG < 1 usually means mispriced growth

PEG > 2 starts to push into the danger zone

Here’s how they stack up:

• $INTC ~2.8x

• $LRCX ~2.0x

• $KLAC ~2.0x

• $AMAT ~2.0x

• $ASML ~1.7x

• $ALAB ~1.6x

• $ARM ~1.5x

• $ANET ~1.5x

• $LITE ~1.3x

• $TSM ~1.1x

• $CRDO ~1.0x

• $NVDA ~1.0x

• $COHR ~0.9x

• $AVGO ~0.9x

• $AMD ~0.7x

• $SNDK ~0.7x

• $MRVL ~0.7x

• $AAOI ~0.6x

• $ON ~0.5x

• $MU ~0.4x

English

@bartender2026 @StockSavvyShay @FuturumEquities @grok the issue is they are taking net income which includes huge non operating income for some e.g. Marvell. Would that make it ok ? Grok is using the standard net income figures.

English

@StockSavvyShay @FuturumEquities @grok validate these PEG ratios. Give me the accurate numbers if these are incorrect.

English

Mk retweetledi

The PEG ratios in the chart are mostly accurate and directionally right based on multi-year forward estimates as of early May 2026. Minor shifts from latest data:

- INTC: ~3.2x (up from 2.8)

- LRCX/KLAC/AMAT: ~2.0-2.5x

- ALAB/ARM: ~2.1-2.2x (up slightly)

- NVDA/AVGO/TSM: ~0.6-0.9x

- MU: ~0.2-0.4x (even cheaper)

- AMD/MRVL: ~0.7-1.0x

PEGs fluctuate fast with prices & estimates. Cross-check Yahoo Finance key stats for real-time. Many AI/semiconductor names still screen attractively below 1.0x.

English

@StockSavvyShay @FuturumEquities are you sure about Marvell ? they have too much non operating income , does that not paint a wrong picture ? and should be excluded ? i.e. PEG > 2

English

And the situation with Hormuz clearly not improving

العميد إبراهيم ذو الفقاري@Ibrahim_alFiqar

We will immediately strike French and British warships if they approach the Strait of Hormuz. They are not welcome.

English

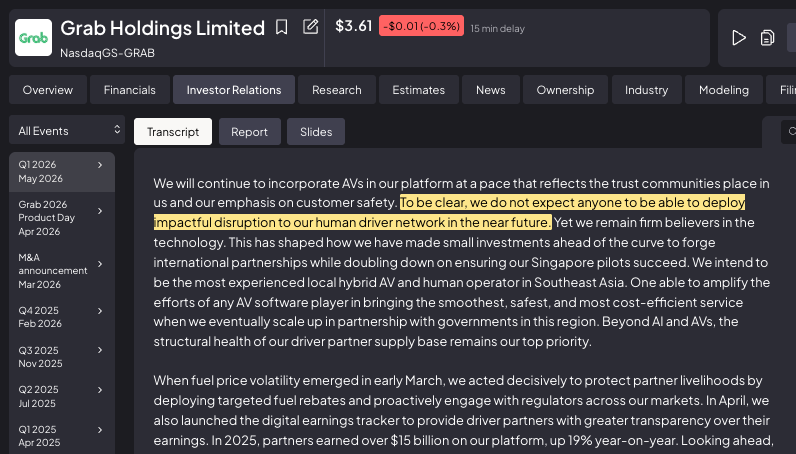

@fiscal_ai Why is Grab considered a reference? No operating income. Theyre not doing well.

English

@fiscal_ai $GRAB is looking like a great buy around these levels, flipping to profitable and as we see in North America the convenience of food delivery is like no other

English

@theMadridZone @diarioas From frypan to fire... Mourinho won't deliver. Let's close the chapter of Mourinho coming to this team. His return to teams have not always ended well.... I'm all out for his success though... I just want Madrid to be feared again. Look at Olise mocking us... 😩😩😩

English

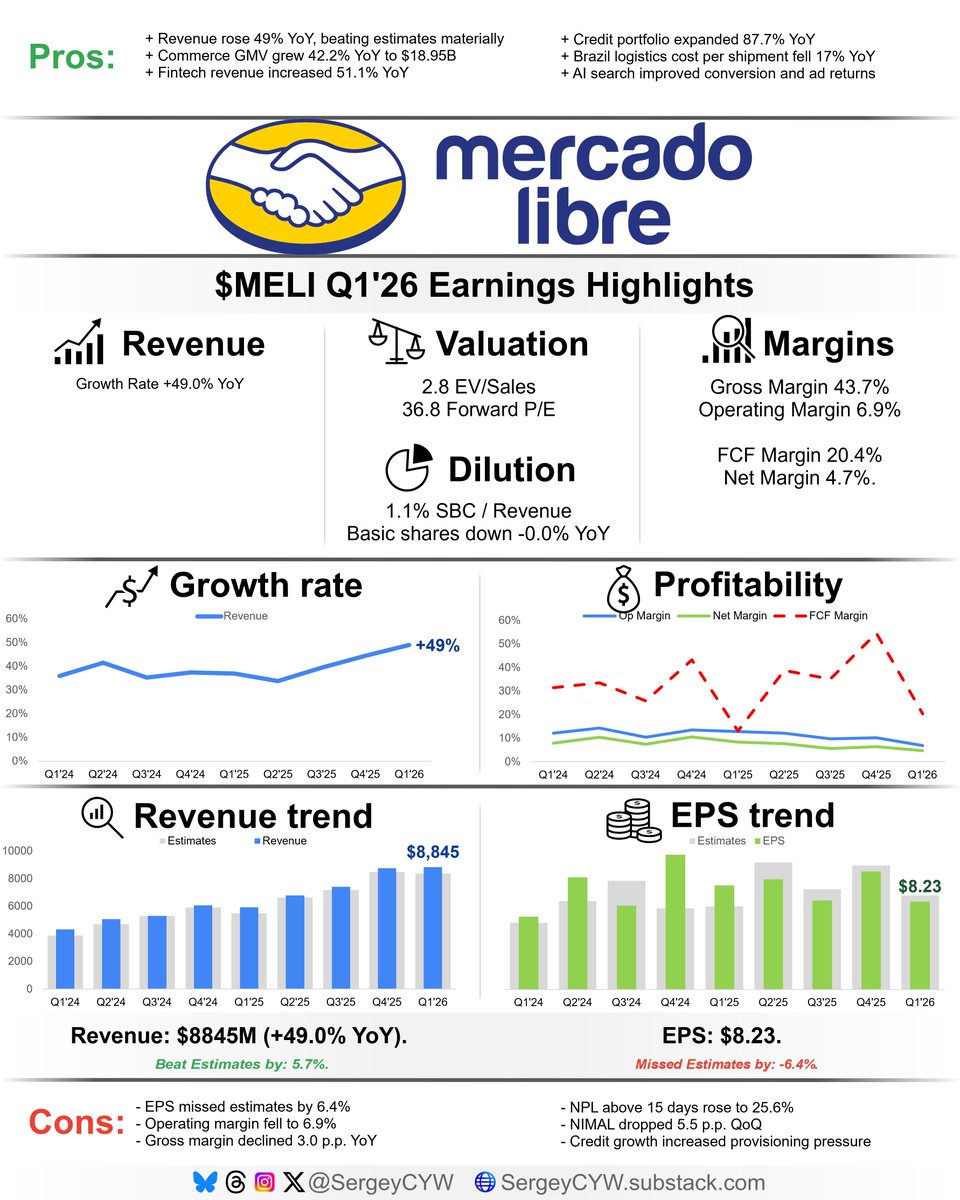

My thoughts on $MELI Q1 2026

The quarterly report was strong, despite the stock falling -4.3% after earnings and being down -28% from its 52-week high.

The stock is trading at valuation multiples close to ATL, with EV/Sales at 2.8x and Forward P/E at 36.8x. Given the accelerating revenue growth of +49% YoY, this is a very low valuation. The issue the market sees is declining margins: operating margin fell -19% YoY and net income margin declined -15.6%.

Is this really a problem and a sign of growing competitive pressure?

Martin de los Santos, CFO: “The margin compression reflects our choice to invest in strategic initiatives, and the results of each investment reinforce our conviction that we’re taking the right steps to build the largest and most engaged commerce and fintech platform in Latin America.”

In reality, management sees enormous opportunities and is investing aggressively in future growth and strengthening the company’s competitive position. The results of these investments are already visible in the accelerating high revenue growth. The scale of the LATAM market is truly massive, and I remain positive on management’s initiatives.

Margin pressure is mainly driven by free shipping expansion, logistics capacity investments, and the growing share of credit cards in the portfolio, but these initiatives strengthen the company’s economic moat. Cost per shipment fell 17% YoY in local currency in Brazil, and management expects unit shipping costs to continue declining.

Brazil remains one of the world’s most attractive and competitive e-commerce markets. The introduction of free shipping in Brazil increased conversion by 1 percentage point YoY, and management stated that MercadoLibre is capturing an increasing share of the Brazilian market. Revenue growth in Brazil accelerated to +55%. Mexico, the second-largest revenue region, also accelerated to +62%. Chile is benefiting from higher free-shipping penetration and faster delivery.

E-commerce:

GMV growth accelerated to +42% YoY and +36% in constant currency (CC). Revenue growth also accelerated to +47.4% YoY and +39.0% in CC, outpacing GMV growth—which means MercadoLibre is monetizing existing traffic and transaction volume more efficiently. Commerce Take Rate increased to 25.7%.

The number of Successful Items Sold increased 47%, outpacing Commerce revenue growth. I view this positively, as consumers are increasingly purchasing lower-priced everyday items, making marketplace shopping a daily habit and deepening engagement with the MercadoLibre ecosystem.

The number of Unique Marketplace Buyers increased in Q1, while after a strong Q4 there is usually a seasonal decline.

Fintech:

TPV growth accelerated to +50% YoY and +54.5% in CC. Revenue growth reached +51.1% YoY and +54% in CC. Fintech Take Rate continues to rise, reaching 4.56%, improving monetization and creating a potential future margin driver.

The fintech segment strengthens the e-commerce ecosystem, while the expanding credit portfolio makes the marketplace even more sticky for users.

The credit portfolio is the key area investors should monitor closely. It nearly doubled to $14.6 billion, driven by credit cards, consumer loans, and merchant credit. Credit portfolio growth is outpacing revenue growth and creating noticeable pressure on margins.

New credit card cohorts require upfront loss reserves and time to mature, reducing NIMAL. Management stated that roughly two-thirds of the reserve-related margin pressure came from credit growth and the increasing share of credit cards in the portfolio.

The share of Credits NPL >90 days increased to 17.6%, which is negative and needs close monitoring. However, in Argentina, NPL metrics in the 15–90 day category improved compared to the prior period.

MercadoLibre implemented LLM-based technologies into marketplace search in Q1 2026. The rollout is already live in Brazil, Mexico, and Argentina. The impact is visible across the entire sales funnel: higher conversion, stronger advertising efficiency, and higher engagement.

At the moment, MercadoLibre sees the rapidly growing LATAM market as a major opportunity and is taking advantage of this by increasing logistics investments and expanding the credit portfolio. I believe this is the right strategy at this stage, which over time should translate not only into high revenue growth but also into improving profitability.

In my view, Q1 was a strong quarter that only reinforced my conviction.

English

@realroseceline why do they have similar margins to Amazon ? shouldnt fintech help

English

$MELI

The market is focused on margins compressing, operating income declining 20%, and some experimentation with the credit products but underneath the surface this may have actually been one of the strongest strategic quarters in $MELI history. Revenue grew 49% to $8.8b, TPV grew 50% to $87b, and GMV grew 42% to $19b.

This is not a mature company struggling to grow a few extra percentage points. This is a company already operating at massive scale while still growing like a startup. The really important thing is that growth is actually accelerating in several key areas even while they are intentionally sacrificing short term profitability. There’s a big difference between weak margins caused by weakening demand and weak margins caused by aggressive reinvestment.

The entire philosophy behind this quarter is actually pretty simple. $MELI believes Latin America is still extremely early in the digital commerce and fintech transition, so management is choosing to maximize long term ecosystem dominance instead of optimizing near term margins. Honestly, when you look at the underlying numbers, it becomes pretty hard to argue against that logic.

The average American makes around 40 online purchases per year while the average Latin American makes just 7. Even buyers on $MELI only average around 11 purchases annually today, which means ecommerce penetration still looks extremely early. If management believes that number can eventually double or triple over time, then aggressively investing today probably makes a lot of sense.

The lower free shipping threshold in Brazil is probably the clearest example of this strategy. Most investors initially saw it as margin destruction, but $MELI clearly views it as long term habit formation. After lowering the threshold, Brazil GMV growth accelerated to 38%, items sold growth accelerated to 56%, and unique buyers accelerated to 32%, the fastest growth in five years.

What stood out to me most was that daily active users are now growing faster than monthly active users. That usually means engagement itself is deepening, not just user acquisition. Anyone can temporarily buy growth through promotions, but when conversion, frequency, and retention all improve simultaneously, it usually means consumer habits are actually changing. That’s where internet businesses become extremely powerful.

What makes this even more interesting is that the economics are already improving faster than expected. Unit shipping costs in Brazil declined 17% versus 11% last quarter, and almost half of the profitability hit from the lower shipping threshold has already been offset through efficiency and scale of logistics. They said that lower cost shipments are already breakeven.

This is basically the classic ecommerce flywheel playing out in real time. Lower shipping costs improve conversion, better conversion drives higher order density, and higher density improves logistics efficiency which lowers costs further. Over time, the ecosystem becomes stronger and more profitable because scale itself becomes the advantage. That is exactly why companies like $AMZN became so dominant over time.

I also think people massively underestimate the importance of the logistics network itself. $MELI now operates more than 50 fulfillment facilities and fulfillment handled 55% of shipments during the quarter while growing 39%. The moat is no longer just the marketplace or app itself. The moat becomes warehouses, delivery routes, seller relationships, underwriting data, payments infrastructure, advertising infrastructure, and consumer habits all compounding together into one ecosystem.

1/ 👇

English

@InvestingVisual why do they have similar margins to Amazon ? shouldnt fintech help

English

$MELI posted a very strong quarter, yet the stock is down ~10%.

Likely due to rapid credit portfolio growth and looser risk parameters. Not necessarily bad, but worth watching.

Credit revenue:

• 2020: $0.2B

• 2021: $0.8B

• 2022: $2B

• 2023: $2.5B

• 2024: $3.6B

• 2025: $5.8B

Investing visuals@InvestingVisual

$MELI Q1 2026 earnings: • Revenue $8.85B vs Est. $8.37B • Net Income $417M vs Est. $426M • TPV $87B vs Est. $80B • GMV $19B vs Est. $18B The compounder keeps compounding.

English

@oguzerkan why do they have similar margins to Amazon ? shouldnt fintech help

English

Let me be very clear: If you are dumping $MELI on these results, you shouldn’t be investing in stocks.

This is a $95 billion company growing 49% YoY…

Woes about margin compression is meaningless. When the runway is this long, the important thing is taking as much market share as possible early on.

They already proved they can expand margins if they want in 2024. They need to maximize their growth potential and shrink the contestable portion of the market as much as possible. This is the right strategy.

If they can do this, margins will naturally and effortlessly expand due to volume growth.

For reference, an average consumer makes 7 online purchases a year in LatAm, while an average American consumer makes 41 online purchases.

This number will converge toward the US average as economies in LatAm grow. This means that every captive customer will bring significant volume growth for which $MELI won’t pay anything to generate.

This is why growing market share at the expense of lower near-term margins is the right strategy for $MELI.

The market will eventually see it and re-rate the stock.

Long $MELI.

English

@StockSavvyShay @fiscal_ai why are their margins similar to amazon despite fintech ?

English

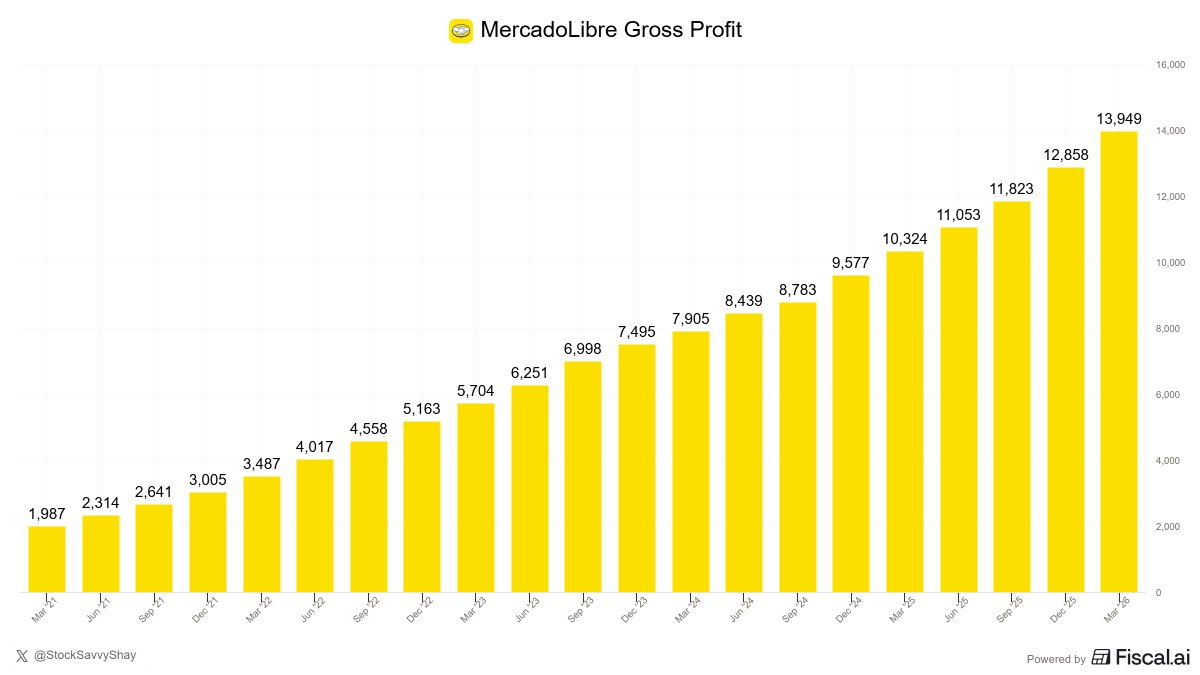

$MELI five years ago:

• ~$1,700/share

• ~$21B GMV with ~$1.9B annual profit

$MELI today:

• ~$1,700/share

• ~$71B in GMV with ~$13.9B in annual profit

Same price. Very different business.

Shay Boloor@StockSavvyShay

$MELI Q1 EARNINGS • Revenue $8.85B vs Est. $8.37B • Net Income $417M vs Est. $426M •TPV $87B vs Est. $80B • GMV $19B vs Est. $18B Free shipping and credit expansion squeezed margins.

English