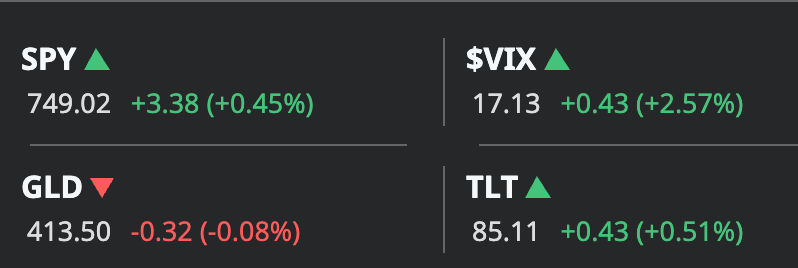

The market is pushing into record territory, but it isn't a blind rally. The simultaneous rise in bonds ($TLT ) and volatility ($VIX) suggests while traders are riding the bullish wave, they are keeping one foot firmly planted near the exit door by buying protection.

English