@Technicalchart1 What's the big deal if the originals are lost ..certified copies of registered property documents are sufficient for all purposes

English

Moid Ansari

3.9K posts

@MoidAnsari11

Engineer | Advocate(Hyd HC) | Momentum Investor (Ride the trend till it ends) | Bibliophile | Lover of old film songs and urdu shayari|

Geopolitical issues seems will become a regular and ongoing thing. Stock markets took a long consolidation because of persistent FII selling which may still keep happening; However now when there is so much value in so many sectors and stocks that the fund managers, institutions and HNIs may not wait, rather will do aggressive value buying. Where there is value, it should now catchup sooner than later. Life and stock market has to keep moving on.

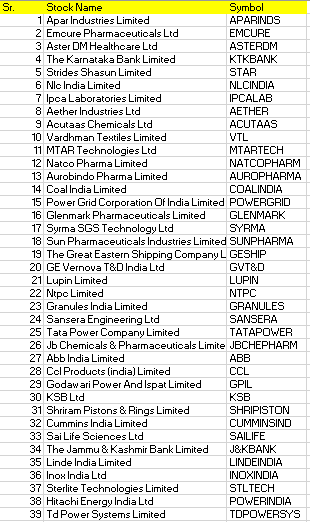

Acutaas Chemicals – The Inflection Playbook | Where Growth Engines Meet Strategic Bets - Not just another chemical company. It’s quietly evolving into a platform across pharma, batteries & semiconductors. - Why it matters 1 | Growth Engines = Cash Generators ▪️CDMO scale-up – 3 projects (₹50–100 Cr each) commercial by Q4 FY26; oncology contract visibility till 2033+ ▪️Battery additives – ₹177 Cr capex; exports start Q4 FY26; full ramp FY27 with China+1 demand ▪️Specialty expansion – Baba Fine Chem not about today’s demand, but as a strategic wedge into semiconductors 2 | Margin Drivers = Quiet Compounding ▪️Mix shift – more CDMO & battery = richer margin profile ▪️Cost optimization – sustainable efficiency gains, already reflected in gross margin uplift ▪️ CDMO premium – higher margin base embedded structurally vs intermediates 3 | Strategic Bets = Optionalities ▪️Semiconductor JV (Korea) – KRW 30 bn project; execution underway; commercial production late 2026/early 2027 with Japanese/Korean majors ▪️Baba Fine Chem leverage – the Trojan horse into Japan’s semi ecosystem ▪️Next-gen battery additives – ₹40–50 Cr capex; commissioning FY27 → optionality beyond current VC/FEC cycle 4 | Financial Backbone = Growth Without Dilution ▪️FY26 capex ~₹250 Cr, fully funded via internal accruals ▪️Net cash position + strong OCF = expansion without equity raising ▪️Solar power projects cut energy costs, improving sustainability 5 | Guidance & Outlook ▪️Management reiterated ~25% topline growth for FY26 with further margin expansion ▪️Sequential improvement expected as CDMO & battery chem projects go live from Q4 FY26 ▪️FY27–28 = convergence of battery chem + semiconductor + CDMO → structural rerating potential 🧭 Investor Compass View ▪️FY26 = Execution year → Deliver on CDMO commercialization & battery additives capex. ▪️FY27–28 = Inflection zone → Battery chemical ramps, CDMO scales, Semiconductor JV commercializes. ▪️Market perception → Still priced as a chemical company. ▪️Reality emerging → A platform with optionalities (Pharma + Battery chem + SemiConductor) that can drive multiple expansion beyond earnings growth. No Buy/Sell recommendation #StocksInFocus #StocksToWatch #actuaaschem #amiorganics

[Memo FY26] Pleased to share Stalwart PMS' latest memo covering our views on: 1. Market correction & current setup 2. Update on a few portfolio holdings 3. Portfolio performance 4. Portfolio characteristics & sectoral allocation 5. Deciphering PE Multiple as a Valuation tool Link in the comments!