Sabitlenmiş Tweet

Morris Ho

989 posts

Can oil services stocks catch up?

Oil's terrible 2010s decade led to underinvestment in new fields as oil producers' cash revenues dried up. While most of them remained profitable (despite lower earnings), their investments in new fields obviously dropped.

Indeed, which CFO would take the risk of heavily investing in new fields in preparation for the next bull market while others don't, as the bear market can last longer than expected? Being wrong with others is generally fine in the corporate world, but being wrong alone can cost you your job.

This is when oil services firms struggle, as a decade of high oil prices and investment euphoria led to increasing demand for their products and services while the following one looks more like a hangover as existing contracts slowly expire and new orders become rare.

In that case, not only do sales volumes drop, but pricing power does too. Indeed, while during an oil bull market clients queue up to buy their products, allowing them to impose their pricings, during a bear market this tendency reverses: Oil services firms have to be accommodative with their clients if they want one of those rare contracts.

This is why, while owning oil services firms seems like a terrible idea when oil is at a cycle high, buying them close to the low could provide an interesting risk-reward.

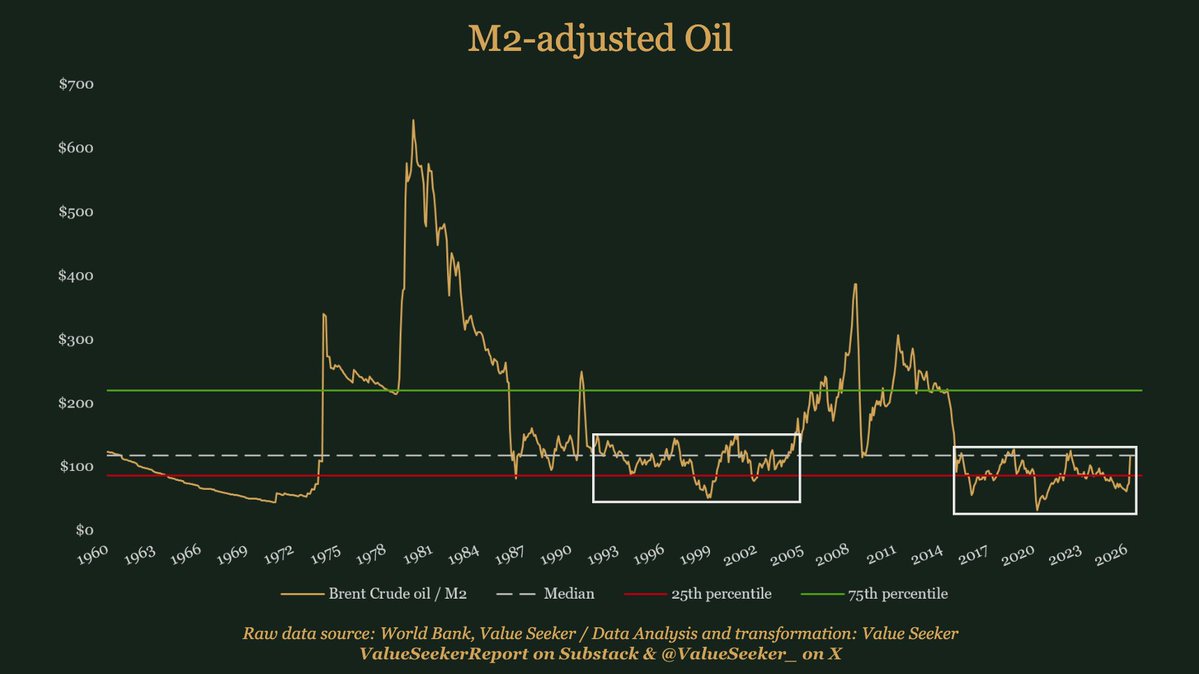

How to determine those cycles? Adjusting oil for money supply growth is a simple but powerful way to do it. Looking at the second chart below, one can notice that the bottom seems closer than the top, despite the recent rise in oil.

As we were exiting a period of depression for the oil sector since 2020, oil services firms were already quite likely to see their turnover rise. The investments in new production capacity that had not been made in the past 15 years would somehow have to materialize to avoid future supply deficits in the coming decade.

So, a bull case already existed since 2020, while the narrative remained pessimistic.

Then came the conflict in Iran, the blockade of the Hormuz Strait, and the destruction of production and transport capacity in neighboring countries, which sent the price of oil higher, rapidly switching the narrative from an "oil glut" to an "oil shock”.

We therefore end up in a situation where:

• Investments in new production capacity were already necessary to sustain pre-conflict production levels,

• Additional capex will be required to rebuild what has been destroyed or damaged due to the conflict,

• Political leaders are likely to push for more diversification among supply sources, ideally closer to home and farther from conflictual regions, leading to the creation of new supply capacity and investment needs.

This is why, even if this conflict were to end tomorrow, I wouldn't be worried for my investments in oil services stocks. The conditions for them had already become positive, while the current geopolitical situation will likely fill the order books for a few years.

As always, while this thesis might end up being wrong (future will tell), the current valuations of those firms and the stage at which they are in their long-term cycles still suggest a positive risk-reward: Heads I win, tails I don't lose my shirt.

—-

Chart 1: Oil services firms: OSX Index (candles) VS Oil (white line)

Chart 2: Oil, adjusted for money supply growth

---

Originally published on my Substack: @valueseekerreport/note/c-237530116" target="_blank" rel="nofollow noopener">substack.com/@valueseekerre…

#OOTT $OSX $IEZ $VK $OIHV

English

@JLawStock I think the same direction, but I hold xle and xom rather than uso😫

Xom and xle are strong but they didn’t follow oil price action .

English

The goal is never to sound smart after the move.

The goal is to read the market before the crowd catches on.

On 22 Feb, in JLawStock Academy, I highlighted Energy, Materials and Industrials as key areas of focus.

On 1 Mar, I warned that the S&P 500 was developing a bear flag and that major indices were showing weakness.

Of course, nobody gets every call right — and that is not what our program is about. What matters is how you respond when the market proves you wrong: risk management, adaptability, and capital preservation always come first.

This is the kind of real-time market thinking we do inside JLA — sector rotation, technical context, risk-reward, and market structure.

See what we do inside JLA:

jlawstock.com/jla

English

I know its Saturday night and we're supposed to be taking a break

but I can't stop thinking about the blanket rerating of software stocks 😅

the AI revolution is going to leave big winners and big losers in its wake

there is a golden opportunity awaiting anyone who can filter signal through the noise now and figure out which companies will thrive/coexist with AI, or get eaten by it 🧐

I will be on the hunt 🫡

English

@theRooster007x @THEROARINGSIGGY @TheRoaringKitty @BPuppy80020 @grok what is this meaning ? Is it bullish for Unity stock price?

English

English

Sector wide selloffs, like we are seeing with software

Often create opportunity

Because the selloffs are never evenly or proportionally distributed

Some suffer worse than they deserve

Others don’t suffer enough

Therein lies the opportunity for those who can sniff it out 🧐

English

NodeStrategy now holds 200 NodeMonkes acquired for a total of 11.997 BTC🔥

22 BTC left in the treasury for sweeping🧹

25 Million $NODESTR burned🔥

NodeStrategy@ndestrategy

NodeStrategy has acquired an additional 8 Nodemonkes for 0.29237 BTC at an average price of 0.0365 BTC. As of 10/13/2025, we hold 200 Nodemonkes acquired for 11.997 BTC. We are now the largest on-chain holder of nm's outside of founding team.

English

Brc20铭文才是底层散户的机会,其他都是小姐,当然,很多坏逼KOL会利用这个趋势推广他们老鼠仓的仿盘协议和比特币生态应用,再说一遍,比特币不需要生态,就简单粗暴的公平铸造的brc20铭文资产,什么也干不了,也不需要赋能,也没有团队,而且已经上了交易所的不要在我评论底下推广,包括 $ordi $sats $rats 都不可能再起来了,因为定价权在狗庄们手里,你奶,就割,你就是反指,回归链上,不要给我推荐什么几把的符文什么的这些都是铭文fomo的产物,回归正统,比特币brc20协议,ordinals协议,就这两个,其他都是小姐协议,既然所有山寨都是价值为0,那我们就简单粗暴的来,追求极致公平的博弈,不要项目方,越复杂的抽水的人越多,就简单粗暴,这才是底层散户的打开方式

中文

@Gee__Gazza That’s why most people stay poor. They don’t deserve the win 😂

English

You’re supposed to sweep NFT collections AFTER the strategy wallet has started accumulating.

That enables the flywheel to kick in.

Otherwise you artificially raise price, strategy buys, lists higher. Floor dumps and no one buys the strategy nfts.

Hope this helps.

English

Punk #3053 bought for 0 ETH ($0 USD) by 0xed01...cf30 from 0xf0aa...cb16 (punk3770.eth) cryptopunks.app/cryptopunks/de…

English

GameSquare has completed its first stock repurchase under the previously announced $5M program.

The Company repurchased 833,124 shares for $599,148, with $4.4M remaining under the authorization.

Consistent with its capital allocation priorities, GameSquare expects to continue funding repurchases through its treasury strategy.

English

@jbondwagon @spencer Actual what the function of $birb

Why so hype ?

English

As part of our ETH treasury strategy with @Dialectic_Group and @MorphoLabs, $GAME is able to lend and yield using a risk-controlled approach.

In August, our onchain yield reached approximately 8%, compared to Coinbase staking at 1.89% APY.

English