Sabitlenmiş Tweet

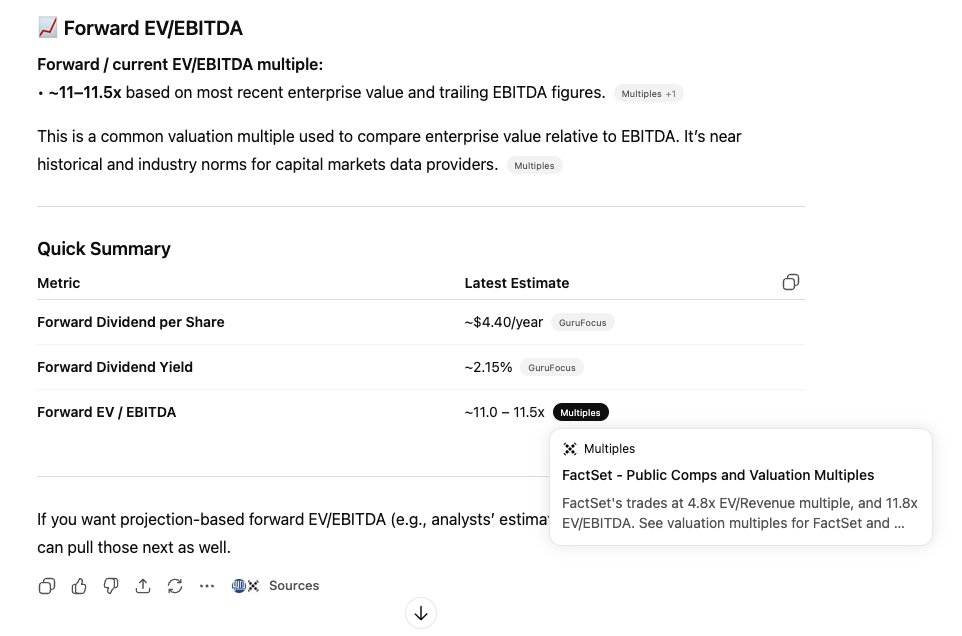

Nueva entrada en mi blog de Factset $FDS. Una breve introducción a la compañía, su entorno actual y qué puede estar perdiéndose el mercado.

Enlace en mi bio

Español

FP&A Investor

413 posts

@Nabulio91

Former Equity Analyst | Currently Senior FP&A Analyst at a Mining Firm | Value Investing | Buffett follower