Newsquawk@Newsquawk

Morning all!

- US President Trump said Israel violently lashed out at Iran's major facility and that the US did not know about the attack, while he said there will be no more attacks by Israel on South Pars.

- US President Trump said the US will retaliate by massively blowing up the entirety of the South Pars Gas Field if Qatar's LNG is attacked again.

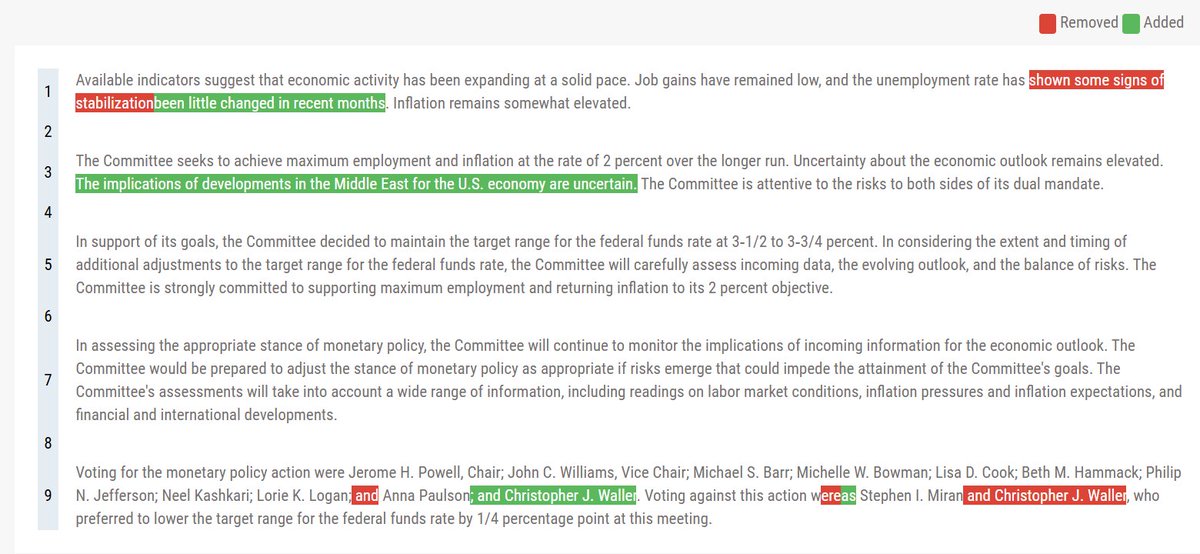

The Fed left rates on hold as expected in an 11-1 vote split, while dot plots were largely unchanged, with little reaction seen.

- Fed Chair Powell noted how the Fed will not look through energy-induced inflation lightly and stated that rate hikes in the future were discussed, but caveated that it is not the base case for the vast majority.

- BoJ kept its short-term interest rate unchanged at 0.75%, as expected, with the decision made by an 8-1 vote as Takata dissented and voted for a 25bps hike.

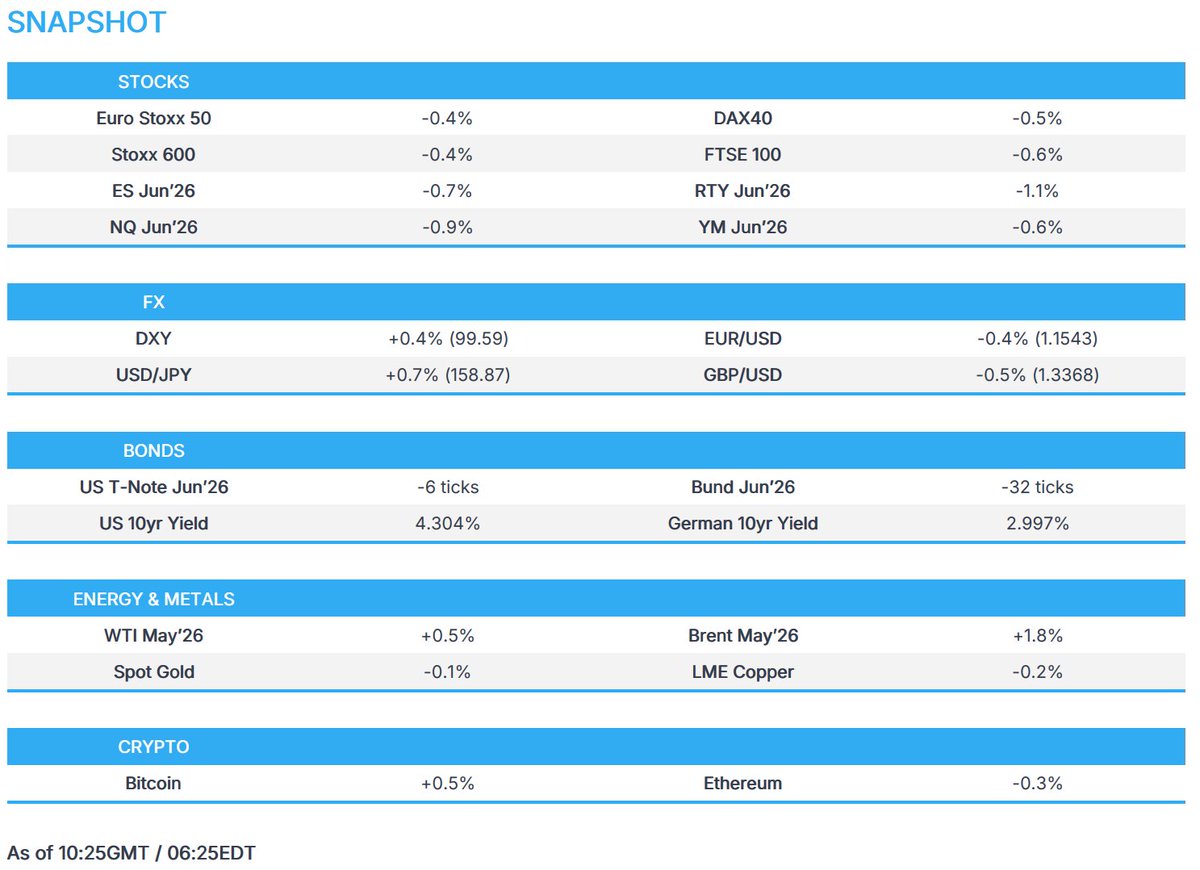

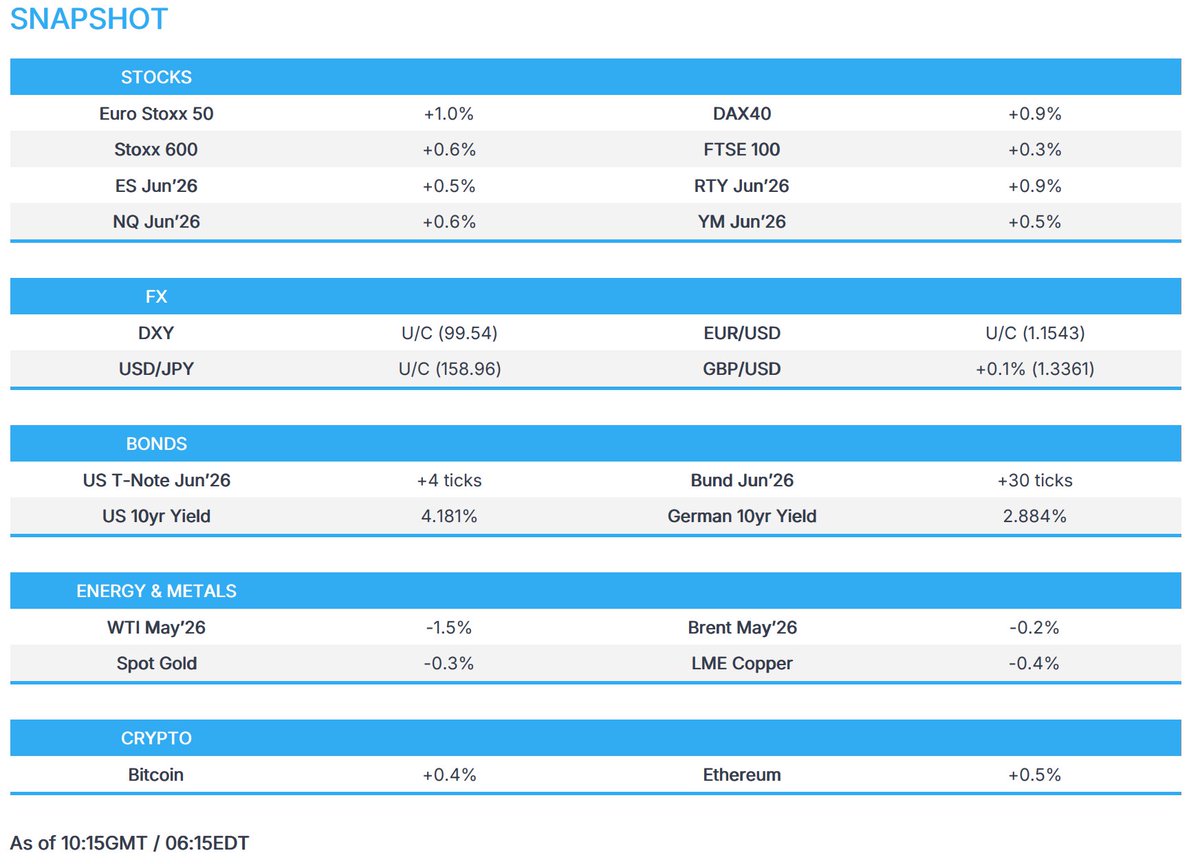

- APAC stocks declined as the region took its cue from the losses stateside; European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 1.7%.

- Looking ahead, highlights include UK Jobs/Average Earnings (Jan), US Initial Jobless Claims (Mar/14), Atlanta Fed GDP, New Zealand Trade Balance (Feb), Riksbank, SNB, BoE & ECB, Policy Announcements. Speakers include BoJ's Ueda, SNB's Schlegel, Riksbank's Thedeen & ECB's Lagarde. Supply from Spain, France & US. Earnings from FedEx & Alibaba.