@nikogeorge Big inflection point. SCOTUS clarity + a Schedule III move would finally align policy with economic reality. 280E relief alone could reshape the entire sector.

I believe Monday, Dec 15 could be a pivotal day for cannabis.

The SCOTUS cert decision on Canna Provisions drops—regardless of the outcome, the same day or Tuesday would be the perfect moment for President Trump to announce moving cannabis to Schedule III, ending the Biden-era delays and the 280E tax burden that's hurting an industry supporting over 440,000 American jobs.

Thoughts?

@CannabisFn@HighNewYork@cannabis_cult@benzinga@Leafly $MSOS

#Schedule3#Trump#WeedStocks

1/4

⚖️ December 15, 2025 could be the biggest day for U.S. cannabis since Raich in 2005.

SCOTUS will decide whether to hear Canna Provisions v. Garland—a direct challenge to federal authority over 100% intrastate, state-legal cannabis.

Granting cert could mean the end of federal prohibition. 🧵⬇️

Been spending a lot of time digging into Nebius Group ($NBIS) over the past few weeks. It’s rare to find a company that is:

• Growing revenue 300–400% YoY

• Has tens of billions in anchor contracts already signed and being deployed

• Yet trades at very reasonable forward multiples

Key notes from my research (mostly public info + filings):

Core business = full-stack AI-centric cloud infrastructure, primarily large GPU clusters plus the developer platform.

Q3 2025 revenue $146M → +355% YoY. Guidance implies 2026 run-rate of $7–9B. Current clusters sold out into 2026.

Two contracts largely de-risk the story:

• $19.4B multi-year take-or-pay with Microsoft (Azure capacity from Nebius’s New Jersey site)

• $3B five-year deal with Meta

Management expects 20–30% EBIT margins on both — well above typical hyperscaler economics.

Nebius is one of the few independent providers able to deliver material volumes of NVIDIA GB300 racks in 2026 outside AWS/Azure/GCP, and the first in continental Europe to bring them online.

Valuation appears attractive on a sum-of-the-parts basis. The market assigns nearly all of the ~$22B enterprise value to infrastructure and close to zero to everything else.

Other notable assets:

• Avride — 83%-owned autonomous-driving company (Level-4 permit). Commercial robotaxi rides live in Dallas via Uber app. Early-2025 third-party round implied ~$6B standalone valuation.

• Toloka — profitable AI data-labeling / generative-AI data engine

• TripleTen — fast-growing edtech/bootcamp business

• ~28% stake in ClickHouse (open-source analytics DB, private valuation >$2B, frequent IPO candidate)

• >$1B net cash + small strategic Nvidia stake

Rough 2027 estimates emerging on the Street:

≈ $12–14B revenue

≈ 25% EBITDA margin → $3–3.5B EBITDA

15× (conservative) = $45–52B EV for infra alone

Add $7–10B for non-core assets → $55–60B total EV in 2–3 years

Today the company is ~$21B EV. That prices in much of the already-contracted growth.

Risks are large and obvious — multi-billion capex, power procurement, execution on new sites, likely future equity issuance — but Microsoft/Meta prepayments + current cash largely fund the 2026 build-out, so the balance sheet isn’t stretched today.

~3× 2026 guided ARR and ~6–7× 2027 EBITDA. Feels inexpensive vs. most private/public pure-play GPU cloud peers, especially with the European regulatory moat and extra optionality.

Not investment advice, just sharing my work. I’m long and plan to hold for years. The mix of (a) hyper-growth already under contract and (b) several billion dollars of additional assets currently valued near zero feels highly asymmetric.

Curious for pushback or extra color — especially from anyone close to European data centers or the autonomy ecosystem.

DYOR / NFA

#NBIS#AI#investing $NBIS

posted for subs trade on the company i think is most uniquely positioned to benefit from this ---with some structural components for outsized gains if it plays out

🚨

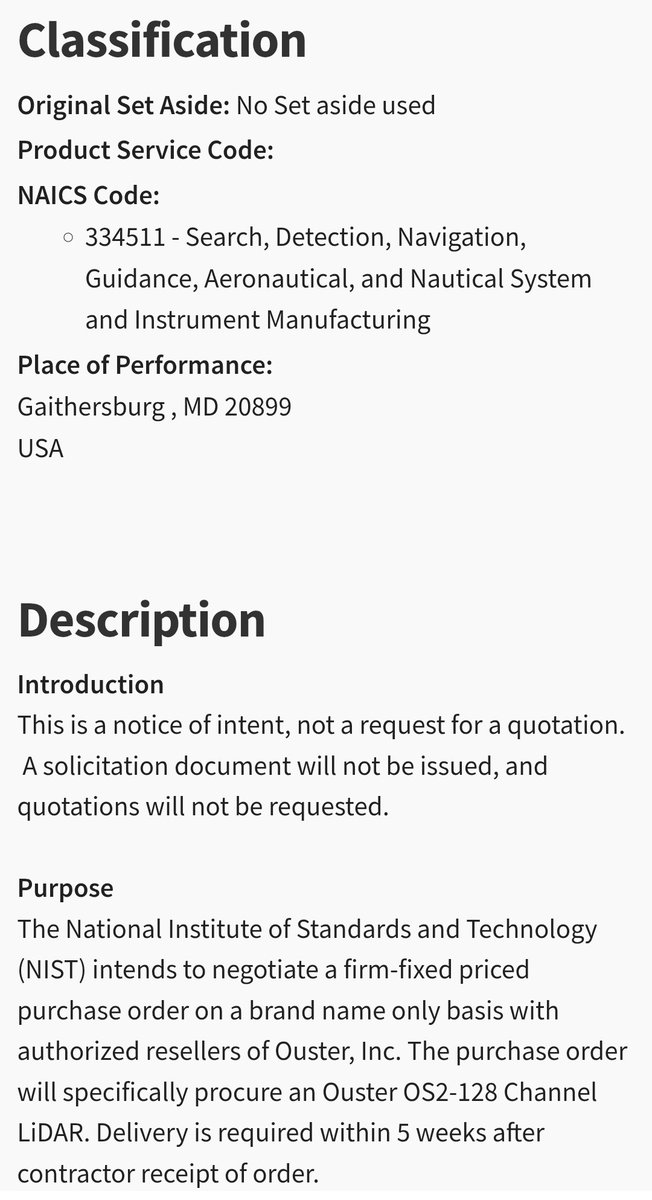

$OUST New Govt Contract found

This is pretty huge on the face of it and it's implications if you read the description.

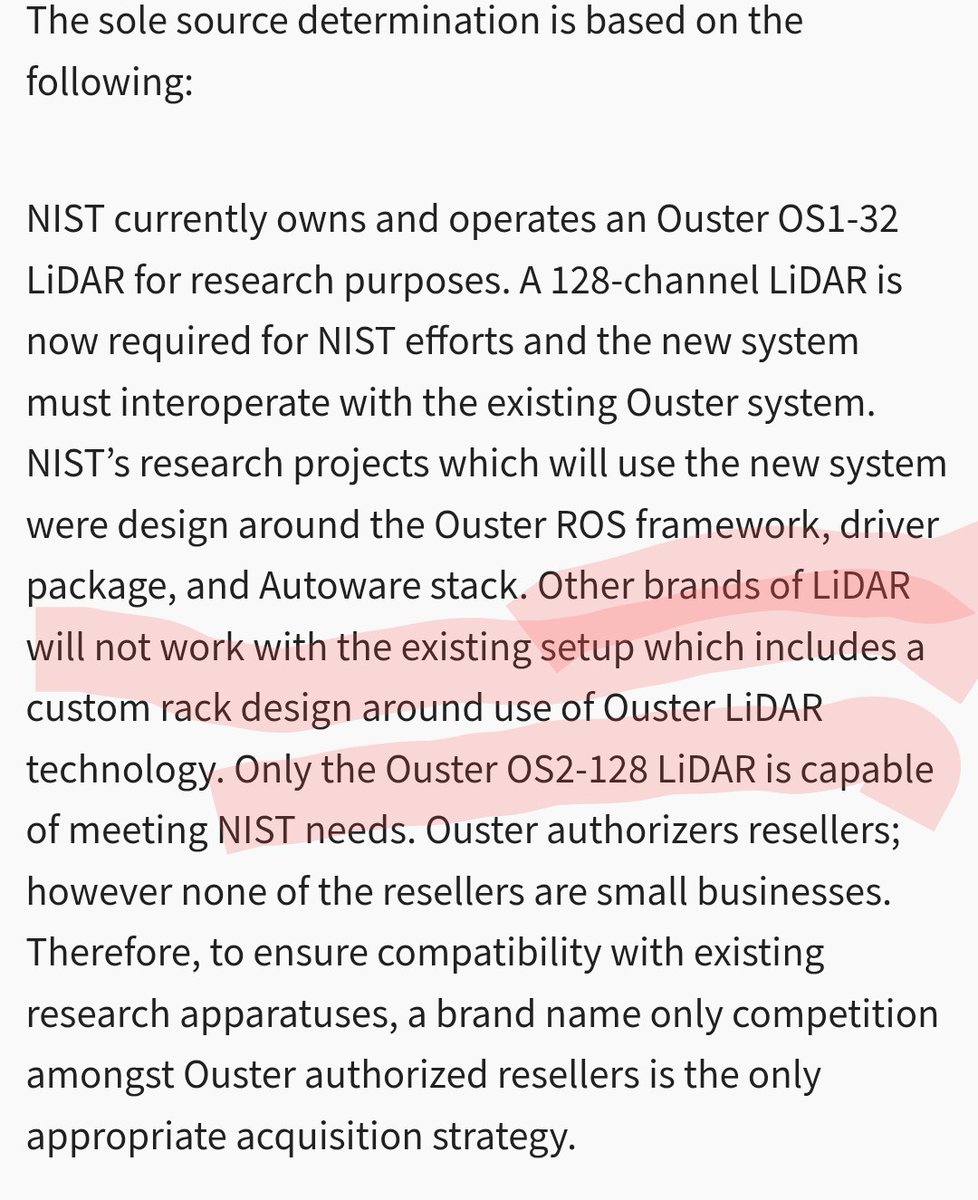

Yhe NIST is upgrading their Ouster Lidar equipment from 32 channel to 128 channel units Read the reasoning as well. sam.gov/opp/9ae29fb876…

@pennycheck@Wambscapital I’m holding a pretty large amount of this as well as the January options? Is it time for me to give up on it or at this point stay with it. My buy price was around 9.80 average

but yes getting dms hating on me for AIP when ive been uncovering next level dd on the name for months spending maybe over 20 hours of research and sharing all my findings for free and its still up 30% from when i said it was a high conviction buy is one of the funnest things about this app

No matter how strong of a thesis you have on a stock it is important to be willing to completely cut it out if you get information that goes directly against your thesis.

It why I exited $BKSY and didn't look back saving a huge loss if I would of held or worse yet bought the dip.