P.R Gailliez

356 posts

P.R Gailliez

@PRGllz

Work in Restructuring | Investment & discussions | early 20’s

Katılım Nisan 2023

68 Takip Edilen69 Takipçiler

Chris Hohn’s full international portfolio as of end of March:

$GE 18%

$SAF.PA 16%

$V 13%

$AIR.PA 11%

$DG.PA 10%

$MCO 9%

$FER.MC 8%

$SPGI 8%

$CP 5%

$GOOGL 5%

$AENA.MC 4%

$CLNX.MC 3%

$CNI 1%

$SAP 1%

$MSFT 1%

English

@fiscorainvest @returnoncap And the current price is interesting imo

English

@returnoncap Didn’t realize $SAF.PA was that big of a holding for them.

English

@Invesquotes It depends how pricing is done. In the case of Fico, it can be abusive. But for airports (for example), one part of pricing is regulated (landing charges etc..), and the other is not (shopping etc..). If they can find balance, it’s fine.

English

One of the things I’ve learned over time is that it’s very very tough to do well investing in a no/low growth business

It’s very tough for a mgmt team to add value without growth and it’s also very tough for the market to rerate a low-growth story higher when there are so many things that are growing (capital is scarce)

I’ve made many mistakes by believing a low-growth story could do well. It can, but most often than not it doesn’t and there’s a lot of growing fish to pick from

English

@DividendDynasty No. But again, if you bought at the right price, it isn’t a sell either.

English

@BramVGenechten What pushed you away ? Valuation ? (Which I could understand, it’s rarely very cheap)

English

@PRGllz Unfortenately not.

Couple of times almost pulled the trigger, but never actually did.

English

Fortinet's FCF/share evolution is the direction of the stock price.

Cash flow is king.

$FTNT

English

@realroseceline It started when dividend dude changed his name.. 🫠. Hasn’t felt the same since…

English

Ngl, X is becoming way more boring. Feels less interesting and more repetitive than it used to be. 🌹

English

@DrewCohenMoney Nice of you to add this, it was going to be my comment 😅

English

Btw inside and outside investment is not a finance concept, but an accounting one applied to partnerships.

I am taking the broader logic behind it though

English

I never hear anyone talk about this, but there is a difference between "inside" and "outside" investment. It also is why it can be "okay" for a company to buy their stock when it is a high valuation.

A good companies investment opportunties are almost always vastly higher ROI than the investing opportunities of outside investors

A fast casual chain might have a 3 year cash on cash return of 50% but trade at a 3% cash flow yeild

It be best for this fast casual chain to deploy all of their capital into building more stores (inside investment), not buying stock (outside investment).

Because of how incredibly wide the disparity of inside vs outside investment opportunities are, buying back stock is almost always a worse investment

HOWEVER, when a company has more excess cash than internal investments demand, they should return capital to shareholders

When they do so, they can either dividend it out or purchase shares.

The former has generally worse tax implications.

If they buyback stock, it is done not as an investment, but rather as a return of capital.

This does imply they may buyback stock at high valuations (like Apple purchases at ~30x versus their orginal buyback purchases <20x).

However, there really is no other great alternatives at that point for them, as stacking cash for potentially years for a better valuation is also not a great capital allocation policy.

(If an investor believed the stock was overpriced, they could sell pro rate equivalent to the repurchases and own the same amount of the company still, but will have pulled cash out in a more tax efficient manner).

The bigger point though is that an outside investors investment opportunties are almost always vastly worse than the investment opportuntieis within a business.

And we see this clearly with $CSU. They acquire private businesses for 1-1.5x revenue. Even after the SaaS sell-off that is 3-4x turns cheaper than almost all SaaS (and their stock trades at ~3x).

If you know the history of $CSU, this has been an old battle with investors. CSU wanted to keep a hurdle rate of ~20% and investors kept saying there is nowhere we can invest and get 15% consistently, so drop the hurdle rate.

They demurred.

But this exemplifies nicely the difference between outside and inside investment.

Mr Deep-Value@mr_deepvalue

One of the more interesting ways to value Constellation Software $CSU is simply asking: “Would Constellation itself buy Constellation at today’s valuation?” Given their acquisition discipline over the years, that feels like a more useful framework than most sell-side models. I did a very rough pass and my impression was: Probably not. At least not anywhere near the current market cap. Something materially lower, perhaps closer to $30 b, started feeling more like the sort of valuation range they themselves historically look for when allocating capital. Could easily be missing nuances here as I didn’t spend long on it, but I’d be curious whether anyone has done a deeper version of this exercise. It feels logically consistent to value a serial acquirer using the hurdle rates it applies to every other business it buys.

English

@PRGllz Cool.

I agree. Always decent, never extreme.

Quality business and management.

English

@BramVGenechten Are you buying atm ? I’ve got a position but I’m a little uneasy on depreciation impact and P/Fcf levels

English

@marc_slans Hohn always. Just a better investor overall. Idk about Msft, but in general, he wins

English

@marc_slans Super complicated business. I don’t know how you can have an edge without being in the industry.

English

$ZTS Remember: stocks no longer have valuation floors. Zero is the floor.

English

@DividendLover93 Is this in yours (if so, very impressed) ? I’d need to be a veterinerian to feel confident enough to touch that one. Most of the businesses I own, I understand because of industry or because I’ve worked close to them.

English

Ahí está la gracia, el mercado ofrece una gran variedad de alternativas.

Zoetis además tiene cierta complejidad. Regulación, veterinaria, medicamentos, patentes, competencia farmacéutica no es precisamente un negocio sencillo de analizar.

Cada inversor tiene su círculo de competencia y creo que es muy importante respetarlo. 😉🍀

Español

Continua la caída en $ZTS y cae un 7% en la sesión de hoy. 🩸🙀

La tenemos a forward PER 11.81 y ofreciendo una rentabilidad por dividendo inicial del 2.76%. 🍀

Español

@0xtechquity If what you want is diversification, then $BRK makes sense. Otherwise, I would pile money in those two. They’re sleep well at night compounders.

English

I am about to make an important decision for my portfolio 🧐

I’m thinking about swapping $FICO for $BRK.B

I still think FICO is a great business, but I don’t like the current regulatory environment. What concerns me most is that growth is mainly coming from price increases (especially in the Scores segment), and I find it difficult to fully understand the moat of the SaaS business.

My choice is focused on the durability of the business. The most important for me. Berkshire would be also a great diversification.

What do you think?

English

@BramVGenechten Volume growth is not as important as pricing growth, and they are one of the rare businesses that have that. They’ve been rating debt since the 1910’s, and have compounded at 10% p/a since. It’s a sleep well at night investment (but sure, you won’t get crazy returns either)

English

@PRGllz True. Rock solid.

Only the slow growth holds me back.

What about you?

English

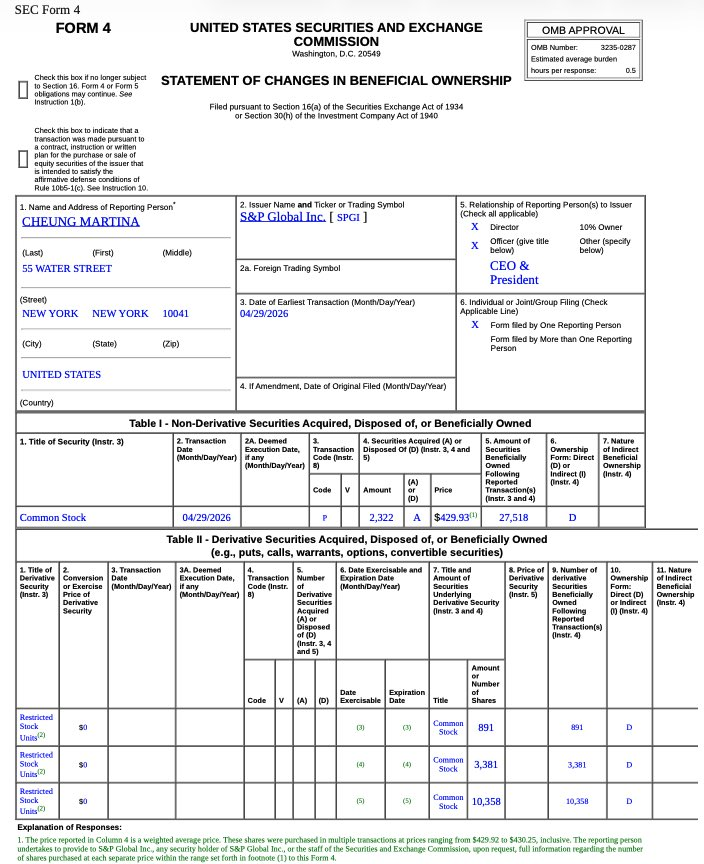

You can now buy $SPGI shares lower than the CEO did 2 weeks ago.

She bought for ~$1M.

English