Bastiaan

1.5K posts

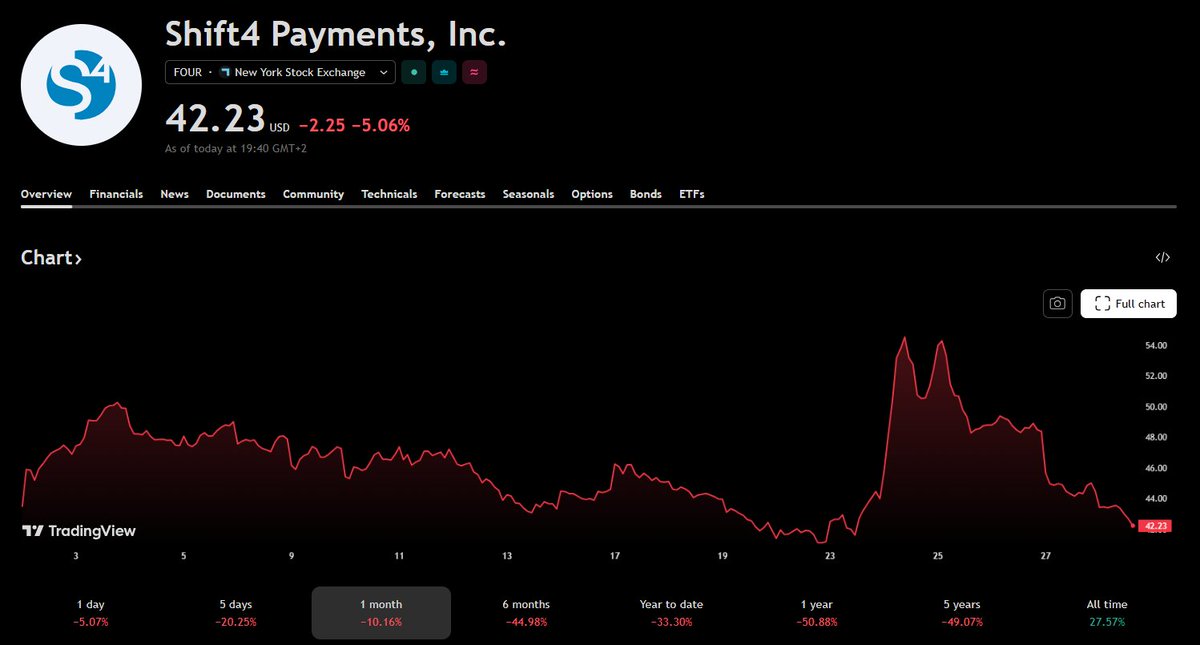

we are back to where we started :) Just try to remember the FOMO you had while we climbed 20% in a day. It is a lot cheaper now.

It is again an extremely asymmetric opportunity.

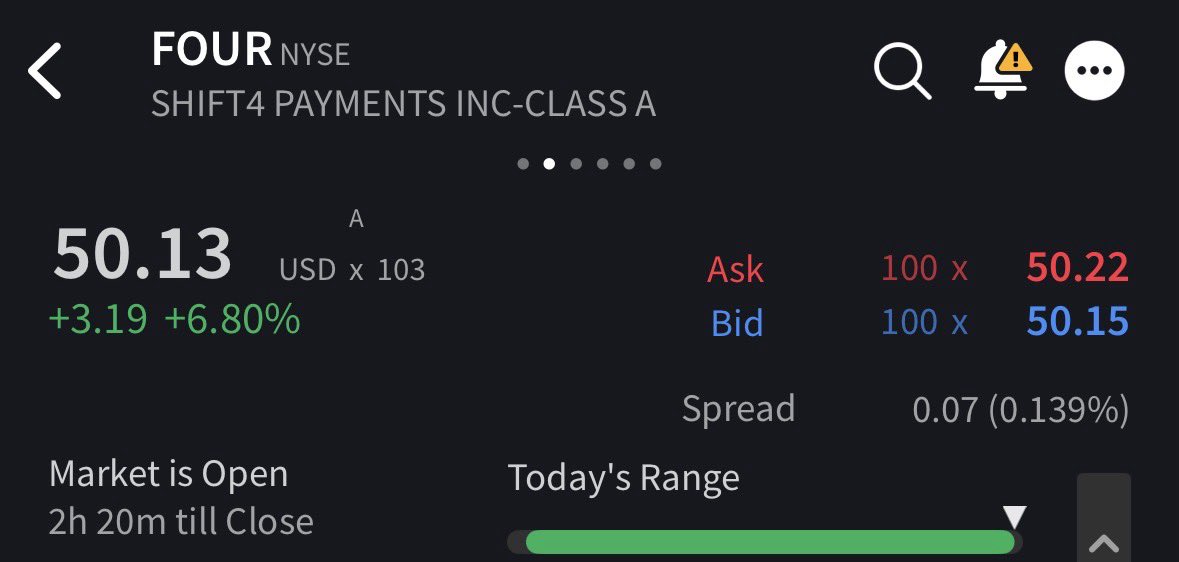

$FOUR

English

@NestBetter Luckily it's a seasonally weaker quarter and the exposure is not that material (both direct to MEA and European sales from middle-eastern travellers). And of course all in all not a structural headwind.

English

$FOUR's global blue is going to have some really ugly numbers.

English

Hereby announcing a - so far - temporary hiatus from X/Twitter. It is not adding the value I for long experienced here, and while a good source for information on investing, there are things more important in life. The time it occupies no longer makes up for the value I expect to receive in return.

Make sure to follow us on tresorcapitalnieuws.nl, we'll publish our thoughts on investing there on a weekly basis, for free.

English

Bastiaan retweetledi

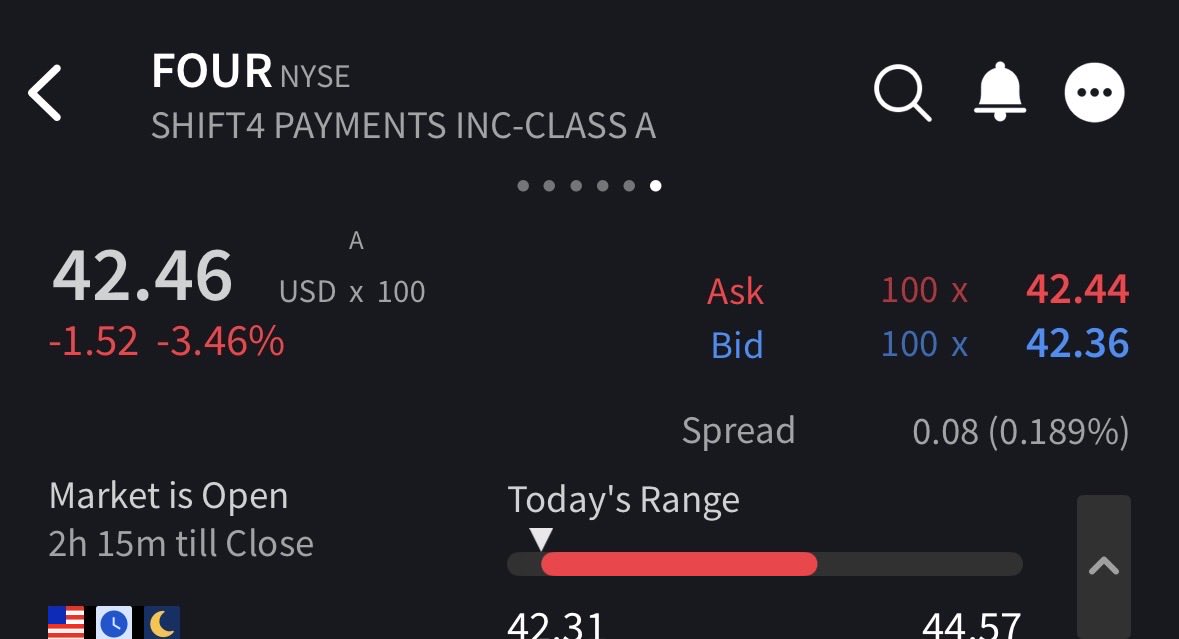

Added more $FOUR at $42.8.

The way i look for it, i will find the bottom one of these days.

English

@atelicinvest @fiscal_ai @AcquirerHQ @evfcfaddict Jup! IFRS reporting. Additional -77m if you substract for that as well

English

English

Is 🇸🇪 Vitec Software $VITB really on an 11.7% TTM FCF Yield right now? 👀

English

@fiscal_ai @AcquirerHQ @evfcfaddict Not following these calculations at all? I see 1.1b in OCF, substracting capex gives me c. 650m in FCF.

Interest costs also not that significant to have such a delta between unlevered and levered?

English

@AcquirerHQ @Picolinie @evfcfaddict $1.083B SEK FCF on $9.11B SEK market cap = 11.8% FCF yield

Technically correct on strict FCF yield definition, but levered Free Cash Flow yield is far lower.

English

@tembelvitesi What will trigger it though?

Shorts got balls of steel here. Record high SI, undemanding valuation, buybacks, reset + sandbagged guidance, take-private target... And for what? An additional -10%-20%? Looks greedy

English

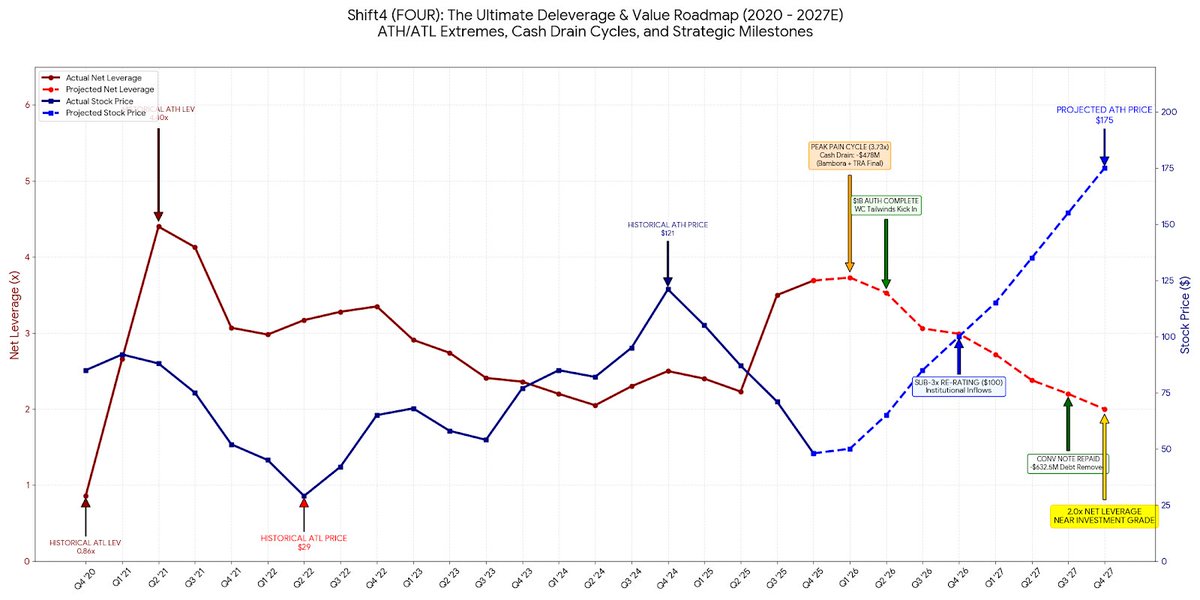

Are we setting up for a massive short squeeze on Shift4 ( $FOUR )? Let’s look at the numbers.

Short interest is currently sitting at 16.2M shares. But what is the real float shorts can play with?

As of Q4 '25, outstanding shares were 84.6M. After factoring in the 4.35M retired in Q4, plus the 3.35M retired between Jan 1 and Feb 26, we are down to 81.2M shares excluding unvested RSUs.

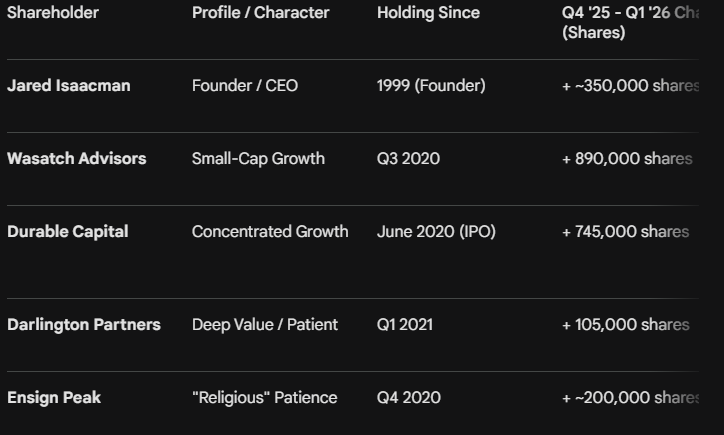

Now look at who holds those. You’ve got a massive block of high-conviction investors who definitely aren't selling or lending:

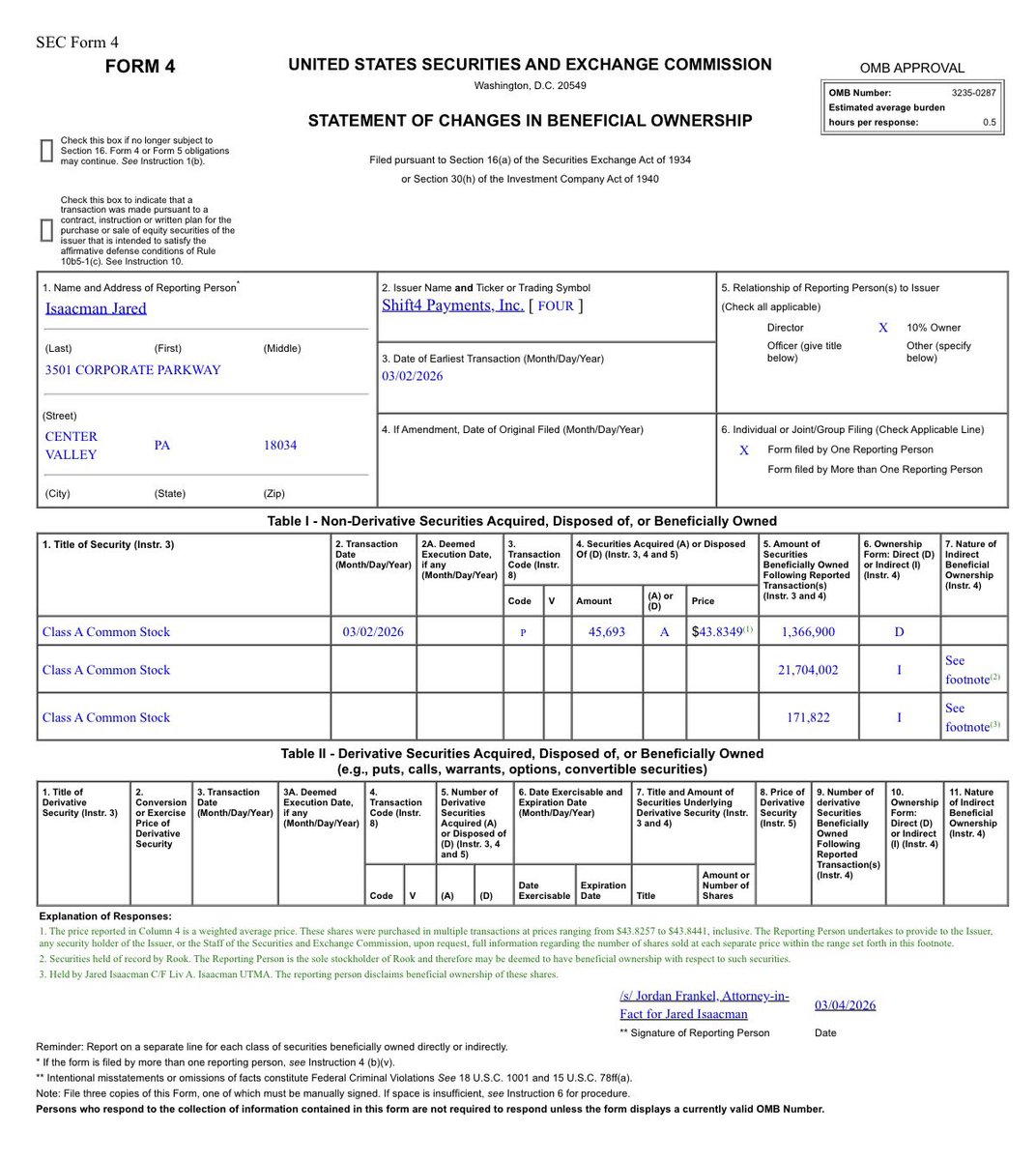

• Jared Isaacman: ~23.5M

• Wasatch Advisors: ~6.8M

• Durable Capital: ~6.6M

• Darlington Partners: ~5.6M

• Ensign Peak: ~2.6M

All of those increased their position in the last quarter with a total sum of 2.3M.

That’s roughly 45.1M shares locked up. So what’s actually left? Just 36.1M shares in play.

Now, imagine what happens when management uses the remaining $500M buyback authorization to retire another 10-11M shares.

We’ll be left with a real float of 25-26M against a 16.2M short interest.

That is around 63% short interest on the real float.

Do you really think shorts can survive that? I have no idea, and honestly, I don't care.

As a long-term holder, I’d love to see management @tlaubers deplete the current authorization, announce a new $1B buyback, and ruthlessly optimize working capital (including expanding AR factoring) to front-load these repurchases while the stock is heavily discounted for the max shareholder value.

English

@Picolinie @CXODanielZ Daniel was in the Netherlands!

English

@Picolinie @tembelvitesi It didn’t even feel like the same person as last week! Chris was very thoughtful and clear at 25Q3 call and previous conferences. Either he was drunk last week or wanted to crash the stock. That’s the only explanation I am able to come up with for the word salad from last week

English

Back in $50s, i still have this urge of wanting it to drop so i can add more.

So many good stuff from CFOs talk today. Almost confirmed all of my thesis.

All costs are in, no upside yet. $FOUR

Next 3 months is probably best time to buy.

English

@kab604 @tembelvitesi Fair correction! Read that a bit too fast 😅

Still positive though

English

@tembelvitesi @Picolinie Fixed cost capital structure* (fixed rate debt afaik)

English

@MyGrowthStocks That 20% is LTM based with '24 overhang that still included post-covid recovery.

Guidance and actual growth for GB in '25 was HSD/LDD

Mgmt explained the decel to 5% on the call (China/Japan and FX). It's also likely a conservative stance, but disappointing nonetheless

English

@Picolinie Global Blue was growing revenues at 20% YoY before the acquisition. How is it possibile projected at 5% now after just 1 year?!?

English

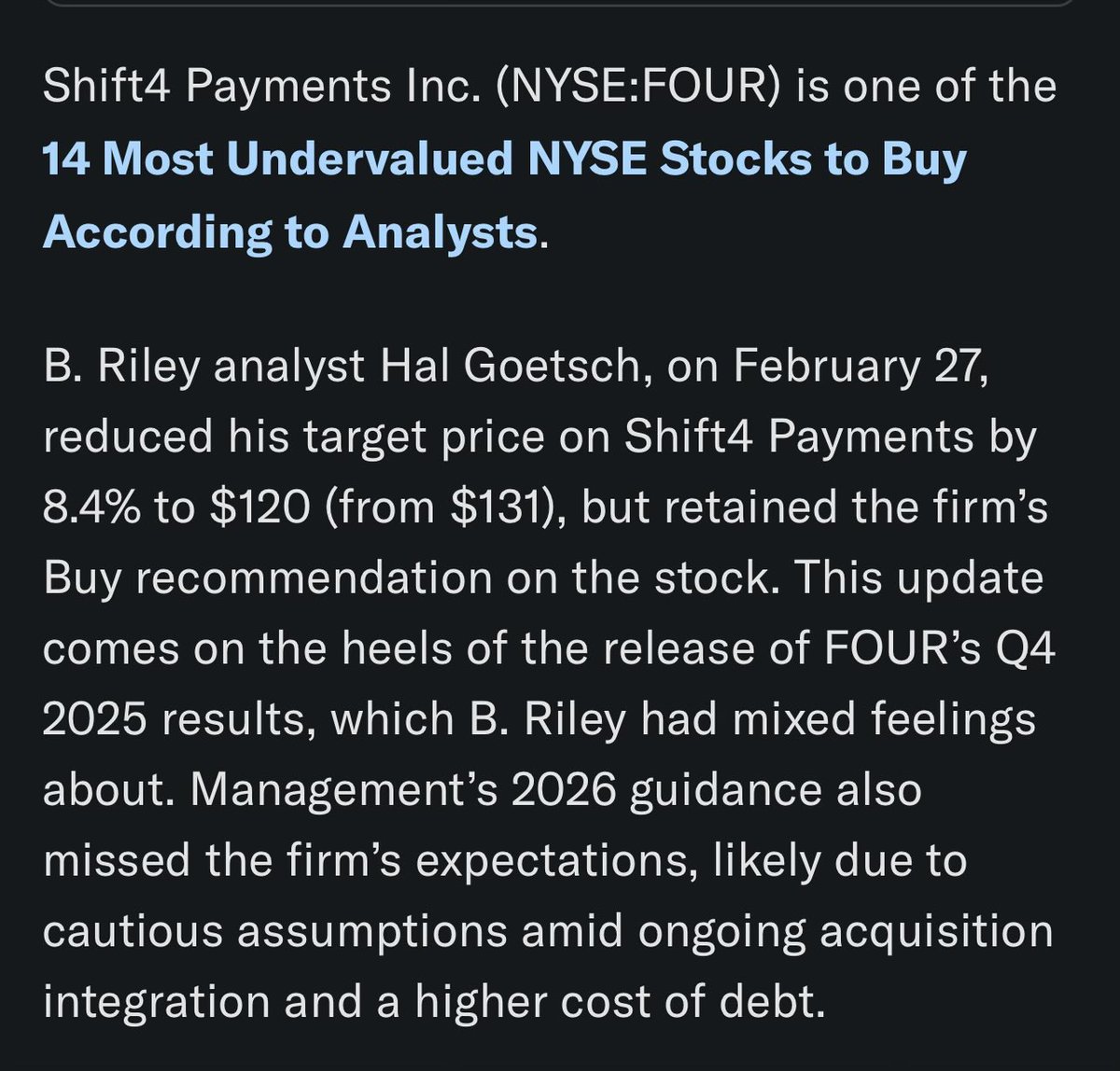

Some quick thoughts on $FOUR ER 💡

Q4 results mostly as expected. The issue is obviously poor guidance and '26 unexpectedly becoming a lost year

Details below, but main takeaway:

- Core payments good

- GB & management disappoint

- The long thesis survives

Now a 'show me' story

English

Conclusion

The post ER reaction is disproportionate

Using conservative assumptions, the IRR potential for the next 24m is asymmetrical

$FOUR isn't for everyone (M&A growth, debt load, etc.). But it's a fair business priced for distress while printing cash

I remain long 🐂

English