Sabitlenmiş Tweet

駿HaYaO

8.7K posts

$MMM (3M) 3M (NYSE: MMM) announced a major planned expansion of U.S. manufacturing capacity for its 3M™ Expanded Beam Optical (EBO) interconnect technology, a high-performance optical connectivity solution for next-generation AI data centers. The expansion will more than double capacity with new advanced manufacturing equipment and additional production space. As AI clusters grow and data center architectures evolve to support faster data movement and higher bandwidth demands, adoption of optical interconnect technologies designed for high-density computing environments is accelerating. Yahoo Finance Alex An, VP of Data Center Vertical Business at 3M, noted that infrastructure is scaling at an unprecedented pace and customers need solutions that deploy quickly and operate reliably at massive scale. 3M EBO solutions leverage the company's material science expertise to enable durable, dust-resistant optical connections for high-density computing environments, improving connection reliability while reducing maintenance complexity in large-scale deployments. Yahoo Finance 3M EBO is already in mass production and has been commercially available since late 2024. The investment strengthens 3M's ability to support customers across the data center ecosystem — including hyperscalers, optical network equipment providers, and cable assembly partners. The fact that a materials science giant like 3M is more than doubling production capacity for AI datacenter optical interconnects reflects the sheer scale and growth velocity of this market. The "more than double" language implies a steep ramp in orders beyond existing capacity, and signals that Expanded Beam technology adoption is accelerating in high-density AI cluster environments. 3M is showcasing the latest EBO technology at OFC 2026 (booth #5233).

早安!3/23 外電綜合整理 - 6515穎崴:美系升目標 美系券商表示公司在AI GPU 之外,伺服器 CPU 與 AI ASIC 的強勁需求,加上SLT市場的市占提升,將提供穩固的營收支撐。隨著產能擴張,券商預期test socket營收今明年成長146%/87%。上修今明年EPS至$111.8/$220.5,介紹28年$260.6,以明年45xPE評價,同步升目標。 - CCL/PCB: 美系升目標:台光電、台燿、金像電、臻鼎 美系券商觀察CCL持續漲價,中低階漲3成,高階漲15%,Lead time拉長,AI需求暢旺排擠產能。T-glass供給緊俏,台廠切入Substrate CCL。而PCB也能順利漲價轉嫁成本,券商預期PCB廠如金像電毛利率持續擴張。最後,臻鼎部分,券商預期有望成爲Google TPU v8 ABF 載板供應商,同時也切入Nvidia Rubin。綜上,券商上修上述公司的財務模型,同步升目標。 - 2408南亞科: 美系重申EW 美系大行解釋上週降評主要理由,主要是看到CXMT可能恢復DDR4產能,+10k wafers/month,而且也會加速DDR5明年的供給。券商雖認為2Q26 還在價格上升期,但有可能見頂,重申EW。 - 6285啟碁:美系升目標 美系預期1Q營收季增5%。預估今明年衛星佔營收比分別為24%/28%。支撐毛利率表現在12.5%-12.9%。最新預估26-28年EPS為$8.9/$10.6/$13.2,以明年20xPE評價同步升目標。 - 3023信邦:美系重申正向 美系認為機器人、液冷、半導體等成爲今年主要成長動能,推升營收/毛利率表現,重申正向。 #下次會考

大摩3月18日发了MiniMax的更新,Overweight,目标价990港元,现价1238,倒挂20%。但报告本身还是值得看的。 M2.5模型过去30天在OpenRouter上消耗量涨了476%,直接冲到排行榜第一,主要是被OpenClaw这个Agent应用带起来的。M2.7模型在MMClaw基准上又比M2.5拉开一截,接近Sonnet 4.6,等于给这个飞轮又加了一脚油。 收入端确实夸张,从2025年7900万美元到2028年预期15.3亿,三年接近20倍,但到2028年还是亏的。DCF隐含2027年56倍P/S。 AI模型公司现阶段的估值锚就是token消耗增速,以及这个增速的加速度。

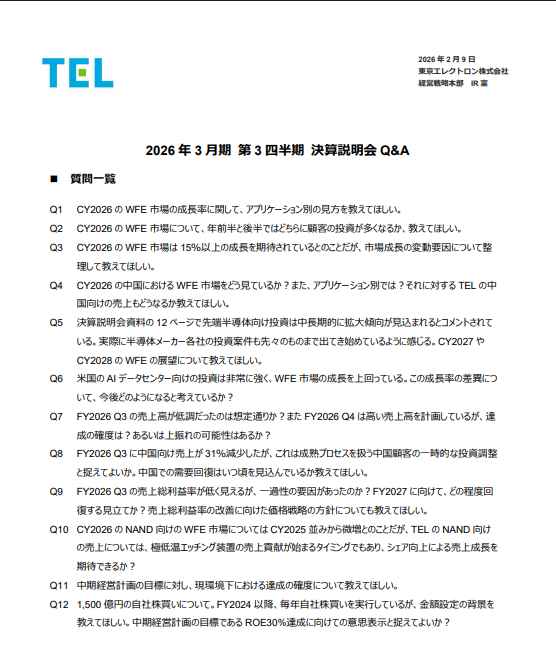

東京エレクトロン、NAND向け極低温エッチング装置について ↓ 顧客の工場稼働率が上がってきていて、これから新規装置の投資に結びついていく段階。極低温エッチング装置の売上貢献はCY2027に顕著になるかもしれない。 tel.co.jp/ir/irta3a00000…

Google is now the first cloud provider to integrate 1 GW of flexible demand into long-term utility contracts. Our ability to shift or reduce our energy demand when it’s needed can help utility companies balance supply/ demand and plan for future capacity needs. This is a big milestone for responsible data center growth and helps keep costs lower for local communities. blog.google/innovation-and…

Formal announcement of the TERAFAB project, which will be done jointly by @SpaceX and @Tesla, tonight around 8pm CT. Livestream on 𝕏. The goal is to produce over a TERAWATT of compute per year (logic, memory & packaging) with ~80% for space and ~20% for the ground.

Merchant InP laser market shares (Cowen est) "Three of the four major suppliers have described strategies to increase laser manufacturing capacity, the outlier being Broadcom, which has not explicitly commented on capacity expansion in a public forum, but which we believe is likely expanding capacity as well. Sumitomo Electric, which we estimate had ~22% of the merchant InP market in 2024, plans to increase InP production capacity by 2.4x from 2023 to 2028. More qualitatively, Mitsubishi Electric (~18% share) has described "partially shifting" its ~$1.5B in annual capital investment from power devices to optical devices. Finally, Lumentum (~30% share) has described increasing capacity by 40% from September 2025 to June 2026."