@HiddenGemsInves $SCR.NE was pretty good on the oil and gas business

English

UnclearConvictions

295 posts

@QualityCap0

Trying to write stuff that make sense... https://t.co/oUhV013xLX

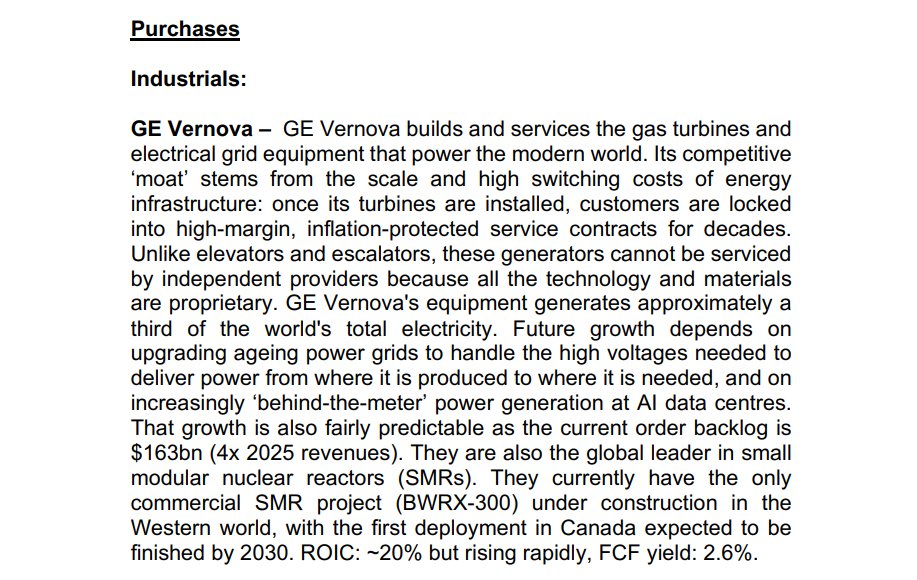

$MSFT is buying these gas turbines from $GEV for West Texas data center It cost $250 million unit