quantumup

9.3K posts

BofA⬆️ $XPEV PT to $29 from $27 and said, "1Q25: core biz in line; expect new models to lift GPM and ASP, new PO USD29, Buy - XPeng expect to launch Humanoid robot sales in 2026" [BofA ests +VE EPS (RMB) of 2.53 in 2026.] $TSLA $BYDDY $LI $NIO $ACHR BofA also said, "Management expects to deliver 102-108k units of vehicles in 2Q25 (+238%-258% YOY) and book RMB17.5-18.7bn in revenue (+116%-131% YoY). Factoring in 1Q25 results, we increase our 2025/26E volume sales estimates for Xpeng by 2%/7%. We now expect the 2025E non-GAAP net loss to narrow to RMB830mn (from a RMB877mn loss). We raise our 2026E non-GAAP net profit estimate by 39%. Our new PO is SD29/HKD113/share (vs. prior USD27/HKD105.3) on higher sales (see details inside). We reiterate our Buy rating as we expect a strong model pipeline in 2025-26." On Humanoid Robots, BofA said: "Xpeng expects to launch sales of its humanoid robots in 2026 for industrial and commercial clients. The company expects that it can leverage about 70% of its EV technology for the development of humanoid robot. Currently, the company's R&D team of EEA (Electrical Electronic Architecture) for EV is in charge of humanoid robot EEA development, R&D team of EV powertrain in charge of robot joint development, and EV autonomous driving team and robotic team in charge of development of the "brain" of the robot."

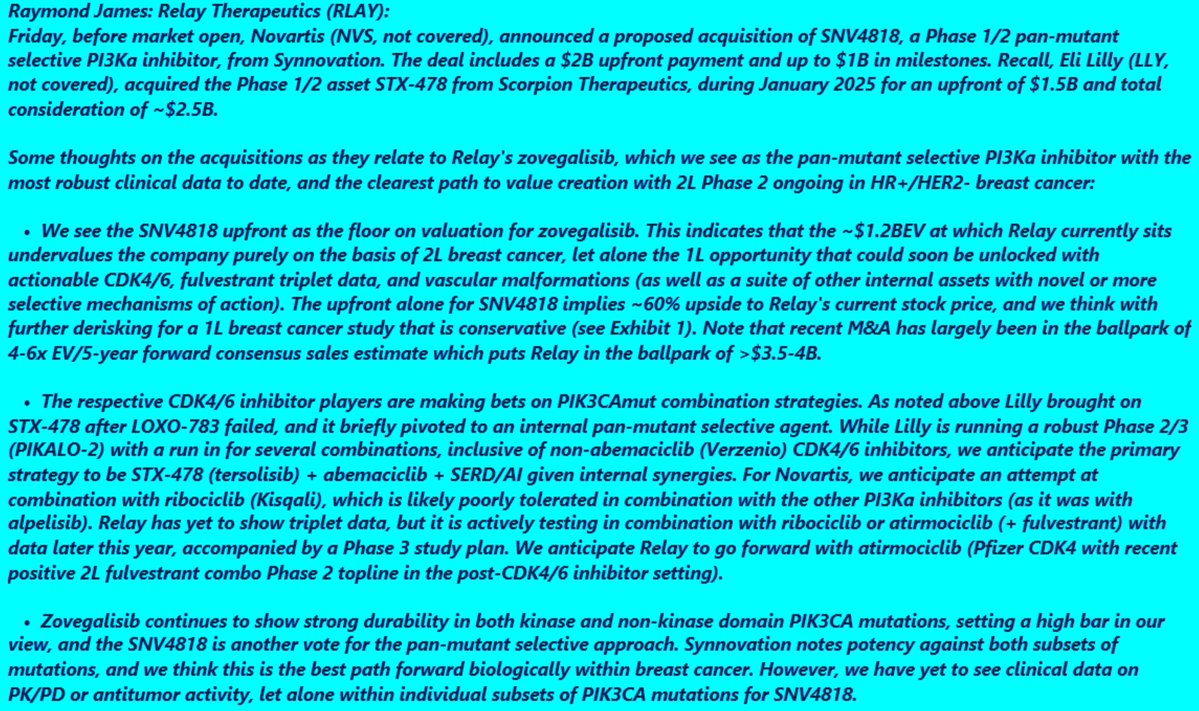

Citizens reiterated $RLAY Market Outperform/$15 $CELC $NVS AZN Citizens said — Relay Therapeutics is set to present, for the first time, Ph2 data for the 400mg BID fed zovegalisib cohort at ESMO Targeted Anticancer Therapies Congress 2026 on Monday, March 16. The ongoing ReDiscover-2 Phase 3 trial is evaluating 400 mg BID administered with food. Relay will look to demonstrate efficacy comparable to prior data (@600mg) to support the RP3D selection and further validate the ongoing registrational program. We maintain our Market Outperform rating and $15 DCF-derived price target.

Stifel reiterated $RYTM Buy; $131. $LLY $NVO Stifel said in its note::We remain Buy rated on RYTM, and while the failure of EMANATE is a disappointment, this indication expansion opportunity was not core to our thesis on the stock, which centers around the blockbuster Imcivree opportunity in HO and the longevity of RYTM's franchise with bivamelagon/RM-718 as life-cycle extenders. Candidly we had thought that at least one sub-population in the EMANATE basket study could've resulted in a fileable dataset. That said, in our model we only had~$100MM risk-adjusted sales from EMANATE indications in 2031 (~$300MM in 2034), which is obviously modest compared to HO which we believe can be >$2B globally at peak. Moreover, there was an efficacy signal here and there still is the opportunity for RYTM to try to leverage learning from EMANATE and address multiple of these sub-populations with one of their next-gen MC4Rs, which appears to be the plan.

Guggenheim🏁 $STOK Buy/$60 $BIIB $PRAX DRUG UCBJY UCBJF JAZZ Guggenheim said in its initiation report: Our investment thesis on STOK centers around our positive view of its lead asset, zorevunersen, a first-in-class antisense oligonucleotide (ASO) designed to restore SCN1A haploinsufficiency, the root cause of Dravet syndrome (DS), by upregulating NaV1.1 expression. Key pillars of our thesis: (1) zorevunersen is the first drug showing disease-modifying potential in DS with benefit not only on seizure frequency but also on cognition, behavior and adaptive function, also supported by EEG biomarkers; (2) the ongoing Phase III trial is well-powered and largely de-risked by solid Phase I/lla and OLE results, and by propensity-score-weighted analyses vs. natural history, which further support the disease-modifying hypothesis. The company expects to complete enrollment in 2Q26, with top-line results in mid-2027, potentially enabling the initiation of a rolling NDA submission in 1H27. We expect zorevunersen to be approved with a broad label (addressing the full DS clinical spectrum beyond seizure control) around YE27/early 2028; (3) as the first DS therapy with disease-modifying potential, we think zorevunersen can command premium pricing. The collaboration with BIIB brings global commercial expertise ex-North America. If approved, we estimate ~$2.5B global peak sales for zorevunersen in Dravet. Not included in our model, STK-002 (OPA1 ASO), currently in a Phase I trial, may provide further upside (initial Phase I results are expected by STOK~YE26).

Citizens $TSHA Market Outperform/$8 $NGNE $NVS ACAD AVXL ALPMY Citizens said—Taysha (TSHA, MO, $8 PT) and Neurogene (NGNE, NC) are moving into registrational studies and both show significant promise. Both registrational studies are well-designed, according to Dr. Davies, to capture improvements in clinical benefit and leverage primary outcomes that are objective measurements of performance outcomes and not patient/caregiver reported or effort based, which are less meaningful.

JPMorgan⬆️ $SRRK's PT to $50 from $47and reiterated at an Overweight rating. $RHHBY $BIIB LLY NVO JPMorgan said in its note—We continue to recommend SRRK into the balance of 2026 and believe apiteg romab should be approved with a broad label (2yo+) and see a strong launch in SMA given the clinical data and high unmet need. We see the drug growing to be a >$2B product in worldwide sales over time. Notably, we recently attended the Muscular Dystrophy Association (MDA) conference (Mar. 8-11, 2026; Orlando, FL) in-person and had the opportunity to attend several sessions focused on spinal muscular atrophy (SMA) where KOLs emphasized the urgency to diagnose and treat early (i.e., time is muscle); we heard in our conversations with KOLs that the focus for apitegromab's use, if approved, will be on patients who are showing functional decline despite treatment with currently available SMN-targeted therapies.

Wedbush⬆️ $LRMR's PT to $12 and reiterated at an Outperform rating. $BIIB $SLDB LXEO PTCT Wedbush said—Last week, LRMR completed an upsized $100M offering following receipt of Breakthrough Therapy designation for nomlabofusp in Friedreich's ataxia. After incorporating the raise, we are also increasing our 4Q25 spending to tie with YE25 cash ~$137M. LRMR remains on track for a ~June 2026 nomlabofusp BLA submission and presuming Priority Review is granted, this could translate to an approval decision as soon as ~February 2027. We continue to assume commercial launch in 2Q27. While we acknowledge recent FDA decisions have been a source of concern for investors, we are encouraged LRMR continues to hold an active dialog with the agency. Most important remains continued alignment on key elements of the nomlabofusp BLA review package. The net of our updates yields a new $12 target (prior $11) and we remain Outperform rated on LRMR.

H.C. Wainwright keeps $XERS at Buy; $10, and said in its 2026 [JPM] Conference Takeaways Packet: [ $CORT $TEVA ] Upcoming Catalyst • March 2, 2026: Formal 2026 guidance and outlook following strong 2025 preliminaries. • 2026: Initiation of XP-8121 Phase 3 trial in hypothyroidism. • 2026: Continued commercial execution across Recorlev, Gvoke and Keveyis. Analyst View • Rating maintained Buy • 2025 revenues (~$292M total revenue; 4Q25 annualizing ~$344M) make 2026 consensus appear achievable or beatable, with Recorlev outperforming and ~700 patients already on therapy. • Recorlev’s growth trajectory suggests revenue could track closer to management’s long-term targets, while consensus remains conservative. • XP-8121 represents a differentiated weekly hypothyroidism therapy with $1B+ peak sales optionality, adding pipeline leverage to the commercial story. • The market still underappreciates XERS’ longer-term revenue goals (2030 target: ~$750M+) and pipeline optionality, despite a growth profile that compares favorably to peers. Actionable Takeaways • Bull Thesis: Recorlev’s growth trajectory suggests revenue could track closer to management’s long-term targets of $750MM+ by 2030, while consensus remains conservative. XP-8121 represents a differentiated weekly hypothyroidism therapy with $1B+ peak sales optionality. • Bear Thesis: Timeline for the XP-8121 Phase 3 trial remains an uncertainty. Payer access for Recorlev and the ability to maintain current patient-titration trends are the primary commercial risks that could stall the EBITDA inflection. If growth was to stall, valuation may look closer to the group than undervalued. • What is Currently Priced into XERS Stock: The market still under-appreciates XERS’ longerterm revenue goals and pipeline optionality. Consensus remains conservative on Recorlev growth, ignoring the potential for the stock to re-rate as a high-growth, diversified specialty biopharma player.

TD Cowen reit'd $ANNX Buy~after full data from the P3 trial of ANX005 in GBS were presented@ PNS. TD says, "the additional analyses support approval and adoption, in our opinion;" thinks 005's efficacy, rapid onset, clean safety/convenient dosing will lead2 rapid/broad adoption:

RBC Capital reiterated $FDMT Outperform-$26, and said Boston NDR Strengthens Its Conviction That GTx Will Have a Role in the $15b Retina Market $OCUL $EYPT REGN KOD RGNX - ABBV ADVM SNY RBC Capital additionally said: We hosted the CEO, CCO, and Head of IR for a Boston NDR. Our key takeaways include: 1) FDMT reminds us that durability in wAMD is in demand by docs and longer-lasting therapies are rewarded with higher revenues, 2) Mgmt thinks retina clinics will find a GTx business model to be financially sound, 3) FDMT sounded confident GTx will have role amongst a wide breadth of patients which may be differentiating vs the TKIs, 4) FDMT is open to ex-US partnerships for 4D-150, and 5) path to approval in CF could feature a small single-arm study with a natural history control. Overall, we think FDMT has an ideal benefit/risk profile for wAMD/ DME, data updates show consistent GTx safety/durability, plus we like that strategic focus has been further sharpened around ophthalmology/CF with the recent workforce reduction. While shares are +102% YTD following a positive update in DME, wAMD pivotal progress, CF funding and changes in the macro environment, we continue to see shares as undervalued with a ~$100m EV. Reiterate Outperform, Speculative Risk rating.

Stifel reiterated $IVA Buy/$17 $MDGL $NVO VKTX ALGS Stifel said in its note: With an over-enrolled NATiV3 trial and new leadership, IVA outlined lanifibranor/Lani's unique best-in-class profile-highlighting its unique panPPAR mechanism-of-action that offers a multi-targeted approach to addressing both underlying metabolic drivers of MASH and liver-specific fibrotic damage. The Ph.2b NATIVE trial validated this three-pronged effect (apoptosis, anti-inflammatory/antifibrotic, insulin sensitization), demonstrating both MASH resolution AND fibrosis improvement at 6 months, with pivotal NATiV3 poised for enhanced activity at 72 weeks (data 2H26). As the latest-stage program in development, the expert KOL panel saw Lani's clear positioning within the current commercial offering (Rezdiffra/ Wegovy), which leaves many patients with insufficient response or unable to remain on therapy to see clinical benefit. In a developing/growing MASH market where future treatment will shift toward holistic approaches, we think Lani will be best positioned as an oral, once-daily, well-tolerated treatment that addresses underlying metabolic disease (particularly F2/F3 patients with T2D).

$PTGX Jefferies ⬆️PT$121 Icotyde (first-/ only-in-class oral IL23R peptide) first approval in mtos psoriais, earlier than expected. Importantly, label safety claims are super clean with limited AE &minimal testing considerations (one of key factors that physicians believe could impact adoption as a convenient oral). With to-date strong profile/ label, PTGX is confident that they can achieve all milestone/ royalty across I&I indications.

JPMorgan reiterated $PTGX Overweight; $93 and said, With shares pulling back from all-time highs in mid-Dec (-14% since Dec 12th), we wanted to re-evaluate the key levers in the story and discuss the set-up for the remainder of the year. $JNJ ABVX LLY ABBV PFE $TAK JPMorgan added: Here is our latest thinking: PTGX's valuation rides on solid momentum towards Icotyde's launch. The royalty stream from Icotyde is a solidified contributor to PTGX shares. The debate about peak sales at our desk has subsided relative to a year ago, with goalposts pointing at $10bn+, and even $15bn+. With approval and launch set for 2H in PsO, the royalty stream flowing into PTGX is becoming increasingly top of mind for investors. Investor inbound has historically focused less on the ramp, and more so on the peak sales opportunity. We expect attention to shift towards the ramp as we approach the back half of the year. Simple maths: 10% royalty on $10bn equates to $1bn. If we apply a 4-5x multiple, this roughly translates to a $5bn EV alone on the high end. As such, with most of PTGX's valuation tied to Icotyde, we believe the floor of the valuation remains solid throughout the year. With Icotyde launching in 2H, we believe investors to remain engaged. Rusfertide royalty stream remains one of the most under-appreciated components, given it is de-risked heading into potential approval in the back half. An opt-out in 2Q is inevitable and will unlock the next $400mn payout from its partner (JPM breakfast note). Simple maths: a 21% royalty on $1.5bn peak sales translates to $1.5bn EV based on a 5x multiple, which is another meaningful addition to Icotyde's contribution. As such, rusfertide remains the key disconnect in PTGX's valuation. Layering on top of the incoming royalty streams, PTGX could easily gain credit for the oral IL-17, as investors see a read-through from the prior work on Icotyde. Oral IL-17 will be the next major internal catalyst this year. With cash-on-hand becoming less of an overhang in the short term, there is less pressure to flip the next data card based on competitive reasons. What will be interesting is that the next lever could lean on the start of a Ph 2 in PsO (which signals PD is favorable in HV), or the release of Ph 1 data in a publication or at a medical meeting. With that said, the bar to get credit for oral IL-17 for PTGX, in our view, could be lower, as we expect investors to see partial read-though from Icotyde's success. Keeping the cards close to the chest after a HV trial might therefore make more sense. PTGX's move to unveil additional obesity programs at JPM two weeks ago was subtle, but interesting. The move to unveil amylin and dual G programs without much preclinical detail (Slide 51), with the next key move being a partnership, raise the question of whether this expansion is built to attract partners over the long run, or part of a bigger strategic goal in the near term.

Oppenheimer⬆️ $CTMX to $12 from $10, reiterated at an Outperform rating, and says that data continues to support its view that CX-2051 could be a game-changer after CytomX reported updated expansion data. $ABBV $RHHBY Oppenheimer said—CytomX reported updated expansion data from CX-2051 (varsetatug masetecan) that, in our view, handily exceeded even the upside case outline in our recent scenario analysis. Confirmed ORR reached 32% at the 10 mg/kg dose with median PFS of 7.1 months, while the 8.6 mg/kg cohort showed a 20% ORR and 6.8 month PFS. Safety also improved with optimized prophylaxis. Grade 3 diarrhea fell to 10% in dose-optimization cohorts treated with prophylactic loperamide and budesonide, supporting the hypothesis raised in our KOL work that Gl tox would be manageable. These data continue to support our view that CX-2051 could be a game-changer for patients with colon cancer, and may have room to move up the treatment paradigm. Increasing PT to $12 (from $10). Reiterate Outperform.

Stifel⬆️ $TRVI's PT to $18 from $15 and reiterated at a Buy. $GSK VRNA - $MRK Here's what Stifel had to say in its note to investors: TRVI is poised to advance Haduvio into late-stage development after Ph.2 trials exceeded expectations in both IPF-CC and RCC, owing to its unique central and peripheral mechanism. Haduvio's efficacy was validated by way of highly successful readouts from both Ph.2b CORAL in IPF-CC and Ph.2a RIVER in RCC, likely attributable to its mixed kappa agonist/mu antagonist opioid MoA that targets cough both centrally in the brain and peripherally in the lungs—essentially granting the ability to target all forms of cough irrespective of disease etiology. Haduvio is the only agent to have shown benefit in reducing cough in IPF, a major detractor from quality-of-life/QoL in the terminal condition, as well as the only agent to be effective in RCC regardless of cough severity (unlike GSK/Bellus' P2X3 camlipixant which only was effective in "severe" coughers). TRVI plans to advance Haduvio into the pivotal development stage in 2026 with a thoughtful strategy to maintain future specialty pricing, focusing on IPF/ILDs first as the rarer conditions and targeting only treatment-resistant RCC patients as a follow-on label addition.

H.C. Wainwright⬇️ $SLNO's PT to $100 and reiterated at a Buy rating. $RYTM $RLMD H.C. Wainwright said—Soleno Therapeutics recently reported its 4Q25 and full-year 2025 financial and operating results: (1) total 2025 VYKAT XR net sales totaled $190.4M, roughly in-line with our forecast of $189.1M; (2) from the date of FDA approval on March 26, 2025 through the end of 2025, Soleno reported 1,250 patient start forms received, including 207 in 4Q25 alone, along with 630 unique prescribers, including 136 new prescribers in 4Q25 alone, and 859 active patients on drug as of end-2025; (3) VYKAT XR currently benefits from a high degree of market access, with over 185M lives covered representing ~60% of total lives; and (4) the VYKAT XR discontinuation rate related to adverse events was approximately 12% as of end-2025, in line with our expectations, and the rate appears to be steadying. In addition, we note that the company has responded to Day 120 questions received from the European Medicines Agency (EMA) and remains on track to potentially achieve European approval of VYKAT XR later this year. Soleno has achieved profitability and positive cash flow; the company reported an end-2025 total of~$506.1M in cash, cash equivalents and short- and long-term investments, after accounting for the impact of the $100M accelerated share repurchase program that was announced on November 11, 2025. We modulate our peak market share expectations for VYKAT XR in the U.S. to roughly 20% of the total Prader-Willi Syndrome (PWS) market, while noting that the failure of carbetocin and the recent pause of the pivotal trial of denatonium acetate appear to indicate a somewhat less populated competitive landscape within this indication. We reiterate our Buy rating, while modulating our 12-month price target to $100 from the prior $120 per share.