Sabitlenmiş Tweet

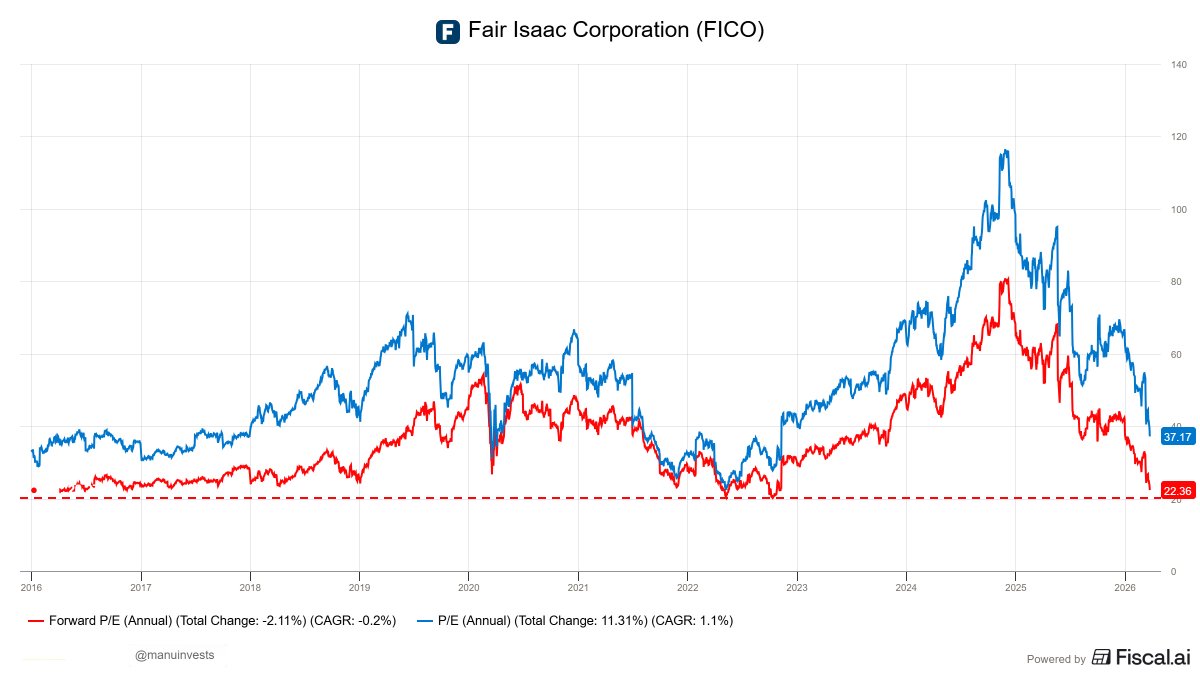

A quality valuation analysis on $FICO

Current price: ~$1,150.

FY26 non GAAP EPS guide: $38.17.

NTM P/E: ~29.6x.

TTM FCF: $718M.

TTM FCF yield: ~2.7%.

As you can see, $FICO is no longer priced like the untouchable monopoly it was in early January when the stock was around $1,666, or even above $2,000

A lot of the multiple compression has already happened, while the business itself is still growing at a very healthy rate.

Before we get into valuation, let’s look at why $FICO is such a good business

BUSINESS QUALITY

$FICO is really two businesses: Scores and Software.

Scores is the crown jewel, and it is one of the best business models in the market.

FICO says its score is the industry standard measure of consumer credit risk for over 35 years and is used by 90% of top U.S. lenders.

That is not a normal software moat

That is infrastructure.

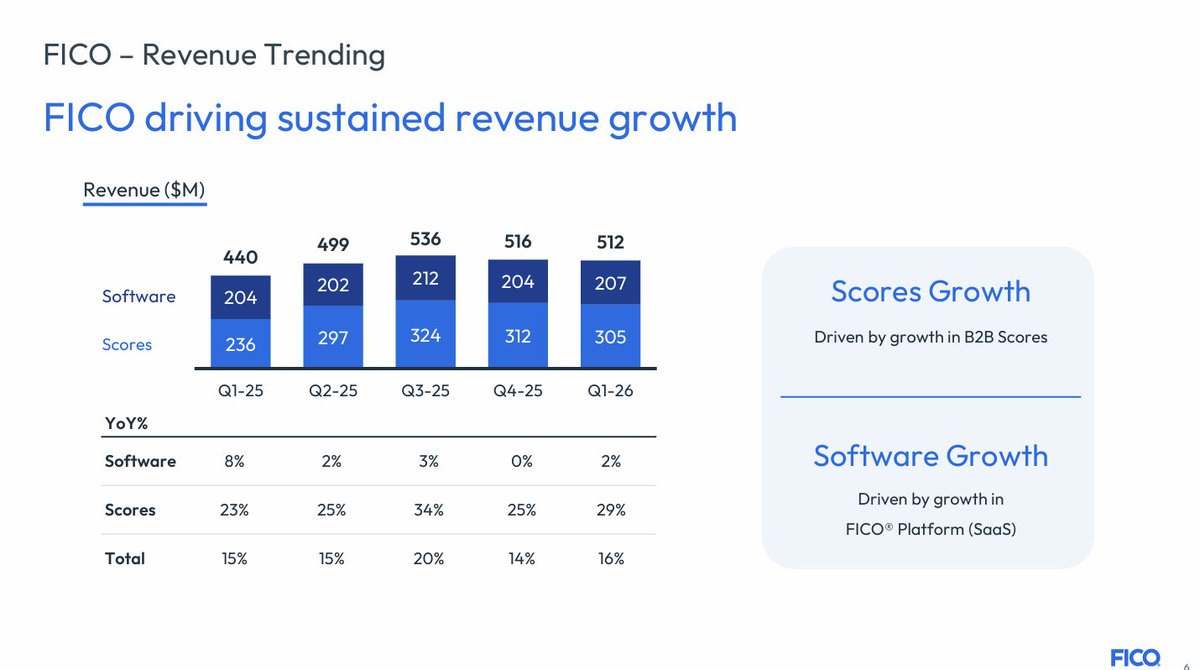

Q1 FY26 was strong:

Revenue: $512M, up 16% YoY.

Scores revenue: $305M, up 29% YoY.

Software revenue: $207M, up 2% YoY.

GAAP EPS: $6.61, up 8% YoY.

Non-GAAP EPS: $7.33, up 27% YoY.

The key point here...the Scores segment is still an absolute machine

Q1 Scores operating margin was 88%.

That is monopoly profitability...point

And the mortgage business is still doing heavy lifting.

FICO said mortgage originations were more than half of B2B revenue in recent quarters, and Q1 Scores growth was driven mainly by higher mortgage score unit price plus higher mortgage origination volume.

The market tends to ignore the Software side, but there is something real there too.

Platform ARR reached $303M in Q1, up 33% YoY, and platform DBNRR hit 122%.

That matters because it gives $FICO a second compounding engine beyond the core score monopoly

BALANCE SHEET

This is where you should be honest: FICO does not have a pristine balance sheet.

Cash and investments were $217.9M at Q1, while total liabilities were $3.66B, stockholders’ deficit was $(1.81)B, and leverage was 2.64x versus a covenant max of 3.5x.

So this is not a cash rich fortress like some other compounders

It is a highly cash generative business that uses leverage and buybacks aggressively

That works beautifully when the moat is intact...It becomes much less comfortable when the market starts questioning pricing power

CAPITAL ALLOCATION

$FICO continues to lean hard into buybacks.

In Q1 alone, it repurchased 95K shares for $163M at an average price of $1,707 per share.

Management explicitly shows a 20+ year history of continuous repurchases and states that share repurchases remain a key part of capital allocation.

This has helped turbocharge EPS growth over time.

But it also means you need to underwrite both the business and the leverage together.

GUIDANCE

FY26 guidance is still strong:

Revenue: $2.35B, up 18% YoY.

GAAP EPS: $33.47, up 22% YoY.

Non-GAAP EPS: $38.17, up 24% YoY.

Non-GAAP net income: $907M, up 28% YoY.

That is the part the market is wrestling with

The stock has sold off hard, but management is still guiding for a very strong year

THE BEAR CASE

The bear case is obvious: mortgage score competition.

VantageScore and the bureaus are pushing hard, arguing that competition can lower lender costs, broaden access, and save hundreds of millions annually

Equifax said more than 250 mortgage lenders were already taking advantage of its VantageScore offer, and more than 40 non GSE lenders were in production with only VantageScore scores for some portfolios

That is why the market suddenly stopped treating FICO like a sacred cow

If pricing gets structurally competed away, the multiple should stay lower than it was before.

THE BULL CASE

The bull case is that the market is overreacting to headline risk and underestimating how embedded FICO still is

FICO is not sitting still: it launched its Mortgage Direct Licensing Program, says it is engaged with resellers representing about 90% of U.S. mortgage volume, and introduced pricing options designed to reduce reseller markup and lender breakage fees

$FICO is also pushing innovation rather than just defending legacy pricing.

It partnered with Plaid for the next generation of UltraFICO, expanded strategic reseller participation, and keeps pushing FICO 10T as the most predictive and inclusive score.

So the key question is not if competition exist

It is whether competition permanently breaks FICO’s economics, or just trims the excess while leaving the franchise dominant

NOW TO VALUATION

At today’s price of about $1,150, $FICO trades at roughly 29.7x FY26 non GAAP EPS guidance of $38.17.

Rather than use Graham’s formula, I think the better way to value $FICO is to ask a simpler question:

What does the stock look like if EPS compounds from here, and what multiple does the market pay at the end?

Let’s use FY26 non GAAP EPS guidance of $38.17 as the base.

If FICO compounds EPS at 10% for 3 years:

FY29 EPS would be about $50.8.

At 25x P/E = $1,270 price target, or about 4% CAGR

At 30x P/E = $1,524, or about 10% CAGR.

At 35x P/E = $1,778, or about 16% CAGR.

If FICO compounds EPS at 15% for 3 years:

FY29 EPS would be about $58.1.

At 25x P/E = $1,453, or about 8.6% CAGR.

At 30x P/E = $1,743, or about 15.4% CAGR.

At 35x P/E = $2,033, or about 21.5% CAGR.

If FICO compounds EPS at 20% for 3 years:

FY29 EPS would be about $65.9.

At 25x P/E = $1,648, or about 13.2% CAGR.

At 30x P/E = $1,978, or about 20.4% CAGR.

At 35x P/E = $2,308, or about 26.7% CAGR.

If FICO compounds EPS at 25% for 3 years:

FY29 EPS would be about $74.6.

At 25x P/E = $1,864, or about 18.0% CAGR.

At 30x P/E = $2,237, or about 25.5% CAGR.

At 35x P/E = $2,609, or about 32.1% CAGR.

What this tells me is simple:

If $FICO becomes just a 10% grower and the market only pays 25x, upside is limited.

If $FICO can still grow EPS 15%–20% and hold a 30x multiple, returns are very attractive from here.

If the mortgage fears fade and the market re rates the stock closer to 35x, the upside becomes very meaningful

So this is no longer a buy anything, it’s a monopoly stock

It is now a quality business with controversy, which is usually where the interesting setups start.

FINAL TAKE

$FICO still has one of the best underlying businesses in the market:

mission critical product,

88% Scores margins,

recurring buybacks,

strong FY26 guide,

and a real second engine in Platform software.

But the stock is no longer priced for perfection, because the market is finally questioning whether the moat is as wide as everyone assumed.

That is exactly what makes the setup interesting.

Today at around $1,150, $FICO looks less like a forever expensive compounder and more like a high quality franchise that may finally offer a real entry point.

English