Ray Zucaro

23 posts

Ray Zucaro retweetledi

February Market Thoughts (PART 2): Add on!

By Raymond Zucaro

3/7/2026

Iran follow on.

There is no way to sugarcoat this, and sorry to any boomer-cons who are on my distribution lists. There was no 4D chess—he messed up and he MESSED UP BIG.

For someone who spends so much time trying to make the White House and new ballroom look “royal,” well, you “royally screwed up” your foreign policy.

Iran didn't have to take out actual oil production—they just had to choke it off so it shuts itself down. The issue is that wells need to constantly run, and what is produced needs to be offloaded to make space for new inventory. That's the choke point: if production can't leave and the storage facilities fill up, you have to shut down production.

A recent sell-side report notes that since the end of February, 76 million barrels of crude had accumulated, with 46 million barrels on tankers, 22 million barrels at refiners, and 8 million barrels in commercial storage. That works out to about 4.5 days of regional exports.

As of today, Saturday March 7th, we've already seen Iraq have to reduce production. Kuwait appears to have nearly filled its storage capacity. The region as a whole, with rerouting, has about 26 to 33 days of storage ability before large-scale shutdowns hit. Different countries have different capacity windows, with Iraq at the low end with 7 +/- days and Saudi with 38 +/- days. Both Saudi and UAE are able to use some pipelines to bypass the Hormuz choke point, but overall capacity of those pipelines is 5 to 7 million barrels per day for Saudi and just 400k barrels per day in the case of UAE. So, while nice, it will not solve the 16 million +/- that transit the choke point on a daily basis.

While the entire world focuses on crude, we think natural gas is actually the more immediate short-term choke point. Liquefied natural gas is harder to store given the very cold temperatures needed to maintain its liquid form. The natural gas market has a very “just in time” production, shipping, and usage cycle. As such, shutdowns will happen much quicker, and restarting production will be more difficult (and time-consuming)—not from the extraction process but from the cooling/liquefaction process.

How will economies adjust to this supply (price) shock? We think you will see very quick demand destruction and industrial stoppage. More essential economic aspects will take precedence (think consumer electricity), but heavy industries will shut down as the economics of production no longer work.

With higher prices we would not be surprised to see remaining exporters restrict supply to satisfy local demands, even from such nations like the United States.

Trump insurance and oil futures

To address some of the blockage, the Administration is scrambling to deal with the choke point issue. Trump floated providing insurance (through the US Government’s Development Finance Corporation) and using the US Navy to escort ships through the passage.

We have seen reports that providing insurance for what the private market has pulled back from alone would imply coverage of approximately $350 billion. The use of Navy assets would also bring them closer and put them in harm’s way, and unlike the last time the US Navy assisted in navigating the Strait of Hormuz during a conflict (the Iran/Iraq war), the proliferation of drones and missiles has certainly changed the calculus of what US naval assets would actually provide.

Late Thursday, the Trump administration talked about using oil derivatives to help lower the price. While we are not experts, we do know the (actual) lack of underlying physical supply at time of delivery will have much more short-term impact than selling futures for markets like Japan, Singapore, and South Korea, when they are unable to power industry.

Some quick thoughts on Winners and losers. *Not investment advice, just current high level thoughts!!

Losers:

US inflation, Higher; Oil and natural gas prices feed into many parts of the inflation basket, and they flow through very quickly. Puts any incoming FED Chairman in the hot seat if they really wanted to quickly lower rates. We think at the very least it will make them pause timetable.

US Treasury rates/supply: Lots of supply will push rates higher. The Supreme Court tariff loss, the need to pay interest on collected funds, actually paying for conflict (estimated to be $1 Billion dollars per day!!!!!!!!!!!!!!!)[1], Gulf States facing lost revenues from selling reserves. We see a supply/demand imbalance.

UST add on: Weaponization coming back to bite one in the posterior region? Less demand from large producers, no longer seen as “safe” asset. Good for other stores of value?

Petro Dollar? Whether factual or not, the perception that these countries agree to sell oil in dollars in return for protection could be called into question. If not selling oil in dollars, MAYBE less demand for US Treasuries????? Maybe less investment from the Gulf Region into US securities across the board? Valuation adjustments??

Japan; As you know from our past pieces, Japan faces SO many problems (higher interest expense, higher defense spending, demographics). We now have the combination of supply/price shocks, which will add significantly to the challenges facing this nation.

South Korea; heavy energy importer

Singapore; heavy energy importer

Europe; Qatar has been an important energy resource replacement for the EU (Qatar is about 6%, US 60%, Russia 13%, Algeria 8%)—especially with the potential removal of Russian supply. Heavy industry—already suffering from much higher input costs—will face an even larger supply/price shock. While national governments provided financial buffers during past price shocks, their balance sheets are now getting more stretched. Not to mention our concern that producing nations might slow exports to ensure domestic supply or to inflict further economic pain. Read: USA and Russia.

Ukraine; The USA has bitten off a lot to chew. With name-calling like referring to Zelenskyy as “P.T. Barnum”[2]and now the need to focus any and all weapon production on current USA and core nation needs, we are pressed to see any prospect for deliveries at current levels going forward.

Airlines; Fuel expenses super-impact financial metrics, and while often hedged, hedges roll off and increased end-consumer prices will lead to demand destruction.

Mid-Term elections and remaining Trump term; As some of the world’s best political pundits note, elections are games of adding coalitions. We currently see this as alienating the Right-wing base and with a sweep of House and most likely Senate, the last two years of the current administration will be (rightly?!?!) bogged down in impeachment hearings.

Winners, *Not investment advice, just current high level thoughts!!

Many in EM. Nigeria, Angola, Argentina, Brazil, Venezuela, Colombia. Think Energy exporters.

US Shale oil: One bright spot for the USA is the higher prices will pull in production.

End of Globalization; Frankly good for Emerging Markets. More infrastructure build-out to address the fallacy of “Just in time” mentality. Nearshoring. More push to spheres of interest.

Russia: As mentioned above regarding Ukraine. (Much) higher price for exports. US rolling back sanctions[3], expand use of energy as weapon[4].

[1] iran-cost-ticker.com

[2] bbc.com/news/articles/…

[3] theguardian.com/us-news/2026/m…

[4] reuters.com/business/energ…

English

@simbadlem Hard to say another other than it being positive. Overall production has increased meaningfully and not prices are MUCH higher.

English

February Market Thoughts

By Raymond Zucaro

2/28/2026

February market thoughts

Well as avid readers know, I kind of march to my own drum. This month I would like to start off with an old joke.

A Soviet and an American are seated next to each other on a plane traveling from Moscow to Washington DC. The American says, I have to hand it to you, your propaganda is very impressive. The Soviet smiles and thanks him but replies that it's nothing compared to American propaganda. Confused, the American tells him, "but we don't have propaganda." The Soviet smiles and says "exactly"

In unrelated news, the Ellison family won their proxy battle for Paramount—Netflix gracefully backed out but pocketed a $2.8 billion breakup fee[1]. This acquisition adds some interesting pieces to Oracle founder's growing media empire, which already includes household names like CNN, CBS, 60 Minutes, and TikTok, to name a few.

We were lucky to have been asked to return on the Best Geopolitical podcaster, The Duran, the video can be found here (link)[2]

Well as another month finishes up, the “no new wars president begins another conflict”. As we closed last month’s thoughts the war drums began ringing hard. We will expand our thoughts more on this topic below.

State of the Union and state of play.

The State of the Union was really a nothingburger; frankly filled with so much false information that we were reminded of our opening joke.

The Republicans, with control of the executive, House, and Senate, have not been able to advance the SAVE Act to clamp down on voting anomalies. And the Supreme Court's dragging its feet on Voting Rights Act changes, pushing them long enough that any changes won't have enough time to be implemented ahead of the mid-term elections. We're now fully convinced that any advances this administration makes going forward will be minimal, if any.

Iran; everyone has a plan until they get punched in the mouth[3]

We do not think Iran will be anywhere near as quick and surgical as Venezuela was. We worry that with the seeming success of that operation, the administration has become swollen with hubris. Unlike the clear winners and losers of the Venezuela piece, it is too early to tell here—but the wildcard is energy. If this stays limited to episodic strikes and proxy flare-ups, we get short-term oil spikes (risk premium stuff, $5-10/bbl pops) and volatility without lasting damage. But if Iran escalates to structural disruption—say, sustained threats to the Strait of Hormuz, major hits to export hubs like Kharg Island, or prolonged outages knocking out 2-3+ million bpd consistently—then we're talking something bigger: persistent higher oil prices, global supply chain hits, and real economic drag that could fracture coalitions fast. That's the line where episodic turns structural, and hubris meets reality.

Tariff Loss; fiscal gut punch

As we've been warning, the possibility that Trump’s weaponized use of tariffs could be struck down by the Supreme Court was very real. In a split 6-3 decision on February 20th [4], the Supreme Court ruled that Trump had indeed exceeded his authority. This significant rout puts a large part of Trump's economic policy in question.

First off, this ruling puts what Fitch Ratings[5] has estimated at $240 billion already collected[6] certainly in question going forward. Fitch notes that's equivalent to 0.8% of GDP being struck down. Many companies have already started filing lawsuits to recover what was illegally collected.

So, in sum, going forward Trump cannot use that mechanism to collect tariffs, and furthermore, what has already been collected will most likely have to be paid back, creating a massive fiscal hole. A sudden reversal of revenue that was plugging gaps in the budget post-tax cuts, forcing either spending cuts, more borrowing, or scrambling for new levies. Even the Court called it a “mess,” and that's putting it mildly—this isn't just policy whiplash; it's a straight-up fiscal gut punch that could keep real yields from spiking too much and nudge the dollar softer over time.

Trump quickly pivoted, assigning blanket tariffs first at 10%[7], then over the following weekend bumping them to 15%[8]. Ironically, for large key markets, the current tariffs are well below what Trump had wanted against key economies like China and Brazil, where the net tariff will actually be lower.

Frankly, it's not even clear to us that the new tariffs Trump implemented are legal, but we'll leave that discussion for the experts and the courts. We would suggest a review of this article (link)[9].

Well we will say we had expected a short-term spike in interest rates on the back of this, but the quick implementation of new tariffs and the drumbeat of war caused a flight to quality (buying US Treasuries).

Marketing (and Asset class) observations

During the month of February, we did a lot of marketing, speaking with people in the United States and also outside the United States.

One strong observation: we noted that international clients and prospects are much more open to true global investment. Hearing comments along the lines of “I would not vacation in some of those markets, let alone invest there” left us at times speechless. Frankly, after speaking with some of the largest US-based pension funds and hearing zero—if any—emerging-market fixed-income exposure, it leaves us questioning their myopic stance.

We also recently attended a very interesting industry-focused seminar on Emerging Markets. Speakers and panelists included some very large EM-focused asset managers, as well as a mix of strategists and even one very senior director and co-head of the Americas for one of the top three rating agencies.

It was interesting for us to hear as many of them echoed our observations: that EM fundamentals and growth prospects—on their own but especially in relation to the “developed” world—have not been this robust in a long time. The rating agency noted that issuers in the Emerging Markets have had a much better upgrade-to-downgrade ratio than they are seeing in many developed markets. They pointed out that much of what is driving the current “developed” market boom—the AI industry—is interestingly pulling along many emerging markets, as much of the capex and build-out related to AI draws on resources found in abundance in Emerging Markets. And let's not kid ourselves—this isn't just about raw commodities anymore. We are talking real yields in the US that are still elevated enough to keep the dollar from completely collapsing, but any path toward softer real yields (FED easing, fiscal mess from the tariff unwind) would turbocharge EM inflows. A weaker dollar has historically been rocket fuel for EM—cheaper debt servicing, better export competitiveness, commodity tailwinds, and capital chasing higher returns outside the US. We've seen it play out in 2025 already with EM equities crushing it partly on currency effects alone. If real yields trend down and the dollar follows suit, this super cycle doesn't just start; it accelerates hard. The largest asset manager on the final panel expects this to be the first year in a five-year super cycle for EM.

Unfortunately for many of my fellow North Americans, we think the rest of the globe sees this trend before many of them do.

[1] bloomberg.com/news/articles/…

[2] youtu.be/Vs616WN_714?si…

[3] youtube.com/shorts/91dO9YM…

[4] supremecourt.gov/opinions/25pdf…

[5] fitchratings.com/research/sover…

[6] nbcnews.com/business/busin…

[7] bbc.com/news/articles/…

[8] cnn.com/us/live-news/t…

[9] cato.org/blog/new-trump…

YouTube

YouTube

English

Ray Zucaro retweetledi

Japan remilitarization. New Fed Chair. Cuba blockade w/ Raymond Zucaro @RayZucaro

youtube.com/watch?v=Vs616W…

YouTube

English

Ray Zucaro retweetledi

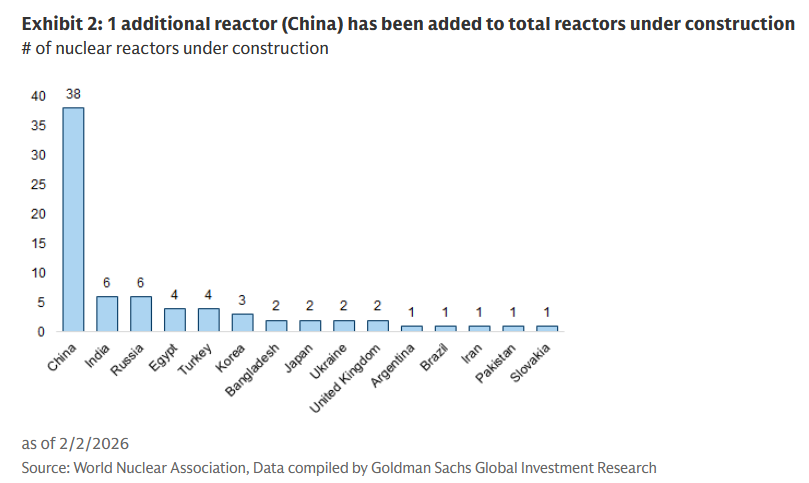

In the last 2 months, China has started construction on another 8 nuclear reactors bringing the total to 38. The US meanwhile issues press releases and strongly worded LOIs

zerohedge@zerohedge

This brings the total nuclear reactors under construction in China to 30, followed by India (6) and Russia (5). There are no new nuclear reactors under construction in the US currently.

English

January Market Thoughts

By Raymond Zucaro

1/31/2026

As avid readers of our monthly thoughts, you know one of our favorite lines is that the Trump Administration and their flooding the zone makes it hard to keep on top of all the news flow! While we do not think things are as bad as EU Foreign policy chief Kaja Kallas thinks—with her quote that it is a “good moment” to start drinking[1], we do share some of the exhaustion of trying to keep up with so much information!

Venezuela, so far so good

It feels like the capture/kidnapping of Nicolas Maduro was a very long time ago, but it did actually take place this month! We have written extensively on the topic, first back in August (here)[2]and most recently post the January 3rd 2026 operation (here)[3]. We were even honored to been invited to discuss our thoughts on one the best Geopolitical podcasters, The Duran (here)[4].

As we are writing this on January 31st, 2026, just 23 days since the January 3rd operation, a lot has happened in regard to Venezuela. Much in line with our forecast! In just 23 days, we have seen a fundamental modification of the hydrocarbons law[5](just as Exxon requested), which undoes the last 20 years, allowing private companies autonomy not seen since before the election of Hugo Chávez.

The US administration quickly rewarded Venezuela with General License No. 46[6], which substantially reduces restrictions for US companies operating in Venezuela. Venezuela announced a general amnesty law[7], which would cover all political prisoners from 1999 to present. Again, the Trump administration quickly rewarded Venezuela by “reopening” airspace[8], which will allow US airlines to once again fly directly between the US and Venezuela—as such, American Airlines has already announced their return to Venezuela[9].

On January 15th, 2026, US Secretary of Energy Chris Wright stated that Venezuela was able to realize 30% higher prices[10], than before the January operation. While only a very short amount of time has transpired, as we articulated in text and on podcast, we see a very bright future for Venezuela, all things considered.

Greenland, “the day the music died” [11]

As we alluded to before, we saw escalation risk around Greenland in the wake of the January 3rd Maduro operation. We saw a marked increase in the Trump administration’s pursuit of Greenland. We saw threats of confiscation of European US military bases and promises of mass selling of US Treasures[12]by EU and NATO members. This on the back of Trump stating on his Truth Social platform a harsh put-down of the UK and specifically Keir Starmer. His use of terms like “total weakness” and “Great Stupidity”[13] we believe marks the real end of NATO—however, the patient may live on a little, but we think the wound was mortal. We have yet to see a clear Greenland structure, but it is clear to this author that the US is retrenching and does not respect the EU/NATO partners.

Metals and DXY; “all that glisters is not gold”[14]

January also saw a parabolic rise in both Gold and Silver. We're not putting ourselves out there as experts here, but just looking at charts, we do feel the rise was Too Fast and Too Furious[15].

That said, we see the overall trend in precious metals in much the same way we see the trajectory of the US Dollar Index as measured by the DXY[16] (but inverse!). Looking back to 2007, the rise in Gold prices tracks the money supply growth at a fairly high correlation ratio[17]. We do not know what triggered the most recent outperformance, and we are reminded of the 1980 Hunt Brothers[18]episode, where a short squeeze drove prices to nosebleed levels—perhaps on the back of Chinese export bans[19]this time around.

Now tying this back to the DXY and our view, especially on the US dollar: This Administration has consistently said they want a “strong dollar, ”[20] but we think you have to parse their words carefully. Back in July, Scott Bessent stated, “the price of the dollar has nothing to do with a strong dollar policy,” and “the strong dollar policy is, are we doing the things over the long term to ensure that the US dollar remains the reserve currency of the world.” When they say they want a strong dollar, our interpretation is that they want the US dollar to continue to be the world’s reserve currency—but that does not mean they do not want a lower US dollar relative to the rest of the world.

As the dollar weakens against large currencies, you can envision countries intervening to slow their respective strengthening (selling their national currency and purchasing US Dollars), thus creating foreign demand for US Treasuries. We expect the trend of a weaker dollar to continue, and looking at historical charts, we can see 90 and 80 as well within 20-year Fibonacci retracements[21]. Our view is that this Administration would like to use a combination of weaker USD and tariffs to help return domestic manufacturing to the US.

We were recently asked by a savvy client if a weaker dollar would impact Emerging Markets in a negative way, especially regarding new issuance. Our view is exactly the opposite—we think a weaker US Dollar will help expand the Emerging Market fixed income asset class. The historical cardinal sin of Emerging Markets has been to issue debt obligations in one currency and earn taxes or revenues in another currency. A weaker US Dollar, all other things being equal, would actually benefit Emerging Market issuers. Anecdotally, we have seen one of the most robust Emerging Market new issue markets in history, with CreditFlow Research[22]stating $49.031 billion of new issuance in January 2026.

FED, let’s see how things come out from the Wa(r)sh.

On the last trading day of the month came the long-awaited announcement of who Trump would nominate to replace Powell this coming May. While not our first choice, we really wanted to see David Zervos[23], the colorful Chief Market Strategist from Jefferies—Warsh will satisfy what Wall Street wanted from Trump. A former Fed governor who married well and, according to Trump, has the look of “central casting”[24]he was very involved with the Fed’s decisions during the Global Financial Crisis (GFC) that started in 2008.

He's no stranger to the (over budget) building, having served as the youngest-ever governor back then, and lately he has been sounding more pragmatic on rates, criticizing the post-crisis easy-money hangover but not ruling out cuts if growth stalls. That might give Trump the dovish tilt he's been screaming for, even if Warsh's old hawkish stripes (he pushed for tighter policy earlier than most in the GFC aftermath) make some wonder if he'll really play ball.

We are willing to give him the benefit of the doubt. But lately many of Trump’s decisions have left us scratching what little hair we have left.

China population, play your game. Implications

In December we were honored to be invited for the first time onto one of the best geopolitical podcasts, The Duran. That segment can be found here[25]and is separate from the earlier-mentioned segment that focused on Venezuela.

In this podcast we shared some of our global macro views and discussed our perspective on China specifically. We were amazed by the vitriol from the armchair warriors in the comment section, but we wanted to entertain some of those aspects to prove our point. One of the threads that popped up in the comments was that China’s actual population is much less than their supposed 1.4 billion[26]people.

Be careful what you wish for. Let’s say the actual population of China is HALF the reported figure, so 700 million people. In that case China would go from being the world’s second most populous country to being the world’s second most populous country! At 700 million they would still be twice the US (assuming 350 million people), 3.27 times larger than Brazil (assuming 214 million), and 4.90 times larger than Russia (assuming 143 million people) [27].

Power production

According to Ember Energy[28], China today has electrical generation of 10,066 TWh vs. the US with 4,401 TWh, the entire EU at 2,727 TWh, India at 2,054 TWh, and Russia at 1,195 TWh.

As a ratio to population—again using 700 million for China—that would put China in the global lead with a ratio of 1.44 vs. the USA at 1.26, Brazil at 0.36, and India a distant 0.14. Even prominent sources like Elon Musk note that China is adding capacity at a multiple of what the USA is adding. He posted, “China electricity generation is still growing super fast, with solar being the largest incremental contributor, and will exceed America by a factor of 3X either this year or next”.[29]

If Artificial Intelligence is truly the future and it does indeed have a voracious appetite for power, wouldn’t that put China at a significant advantage?

Mobile phones

Another look at a proxy for population: let’s look at mobile phones. According to the CIA World Fact book[30](one would assume they know, as they’re most likely tapped in), China has 1.87 billion mobile phones. The USA has 391 million, France 77.5 million, Russia 270 million, and 1.15 billion for India.

As a ratio to population—again using 700 million for China—that would put China with 2.67 lines per person vs. the USA with 1.11, France with 1.16, Russia with 1.88, and India with 0.78.

Car production

How about car production? China produced 31.2 million[31]vs. the USA with 10.6 million, France with 910K, Russia with 982K, and India with 6 million.

As a ratio to population—again using 700 million for China—that would put China with 4.47% cars per person vs. the USA with 3.02%, France with 1.36%, Russia with 0.69%, and India with 0.41%.

Per Capita GDP (PPP)

How about one more? Let’s look at GDP on a purchasing power parity basis. According to the IMF and the World Economic Outlook[32], China has a GDP (PPP) of $41.02 trillion, USA $30.6 trillion, France $4.53 trillion, Russia $7.14 trillion, and India $17.71 trillion.

As a ratio to population—again using 700 million for China—that would put China with per capita GDP of $59K vs. the USA with $87K, France with $67K, Russia with $50K, and India with $12K.

So, in summary, what does this all mean? Frankly, it means nothing. For all those doomsayers looking for negatives to latch onto, be careful. If China’s population is really as low as some of you say, then they have already largely caught up with the developed world—and given the strong and growing infrastructure in power alone, they are well positioned to be the global leader for the foreseeable future.

Iran

As we finish out the month, we are once again hearing the saber-rattling of yet another potential Middle Eastern conflict. As someone who watched their generation sold lie after lie—about WMDs, spreading democracy, and quick victories and saw friends return home forever changed, haunted, we are not supportive of what we see unfolding. Promises of "no more foreign wars" and bringing our troops home have once again been replaced by talk of boots on the ground in far-off lands, fighting battles that serve others' interests far more than our own. Enough is enough. We very much agree with John Mearsheimer: “… it is not in our national interest to have this conflictual relationship with Iran”[33].

[1] politico.eu/article/eu-chi…

[2] x.com/RayZucaro/stat…

[3]x.com/RayZucaro/stat…

[4] rumble.com/v74d7gy-can-de…

[5] bbc.com/news/articles/…

[6] ofac.treasury.gov/media/934886/d…

[7] reuters.com/world/americas…

[8] apnews.com/article/venezu…

[9] news.aa.com/news/news-deta…

[10] spglobal.com/energy/en/news…

[11] youtube.com/watch?v=PRpiBp…

[12] (11) Richard Werner on X: "The Dutch Minister of War may not realise, but he can only "offload" US Treasuries in one threatening move, if the Fed agrees. He may not realise that European investors only ever received a promise on a promise: US Treasuries were never handed over & never left the country." / X

[13] reuters.com/world/europe/t…

[14] goodreads.com/work/quotes/26…

[15] imdb.com/title/tt032225…

[16] marketwatch.com/investing/inde…

[17] x.com/SilbergleitJr/…

[18] scottsdalemint.com/articles/2024/…

[19] x.com/WhaleInsider/s…

[20] bloomberg.com/news/articles/…

[21] x.com/RayZucaro/stat…

[22] creditflowresearch.com

[23]@jefmacrostrat; jefferiesmacrostrategy.com/subscribe/

[24] x.com/Juliedonuts/st…

[25] rumble.com/v72ymx2-weapon…

[26] en.wikipedia.org/wiki/Demograph…

[27] worldpopulationreview.com/countries

[28] ember-energy.org/latest-insight…

[29] x.com/elonmusk/statu…

[30] cia.gov/the-world-fact…

[31] visualcapitalist.com/mapped-global-…

[32] worldometers.info/gdp/gdp-by-cou…

[33] (x.com/BergerPosts/st…

YouTube

English

December Market Thoughts

By Raymond Zucaro

1/10/2026

A little (personal) background

I've noticed that straying from the party line these days triggers not just disagreement, but outright intolerance—name-calling (Putin puppet, conspiracy theorist), even physical threats.

This has only hardened my resolve to act like an umpire in all things: calling balls and strikes, no matter who dislikes the call.

Decades ago, a family member in charge of an estate took liberties with the assets. When the missteps were raised with their parent, the response was simple: "That's my child—I can't call out bad behavior." That single event left a lasting mark. My surname may translate to "sugar," but I've never been one to sugarcoat. I aim to stay objective and truthful, whether you like it or not.

So much to say!

Throughout the month, we start jotting down ideas for potential things we can discuss in our monthly thoughts. With the velocity at which global events have unfolded over the last month, we do think they are worth mentioning but because of so many topics we will not do as deep of a dive as usual. We do not mean to imply any point is “not important” or trivial, all are incorporated into our Mosaic {1} of creating a current global picture.

In Latin America, a continued “step to the right {2}” saw José Antonio Kast win a resounding victory over Jeannette Jara of the Communist Party in Chile's presidential election. In Honduras, Nasry “Tito” Asfura managed a slim victory over Liberal Party candidate Salvador Nasralla. The twenty-seven-thousand-vote margin that gave Tito his less-than-1-percentage-point win came amid the great political capital burn of Trump having pardoned the U.S.-convicted former President Juan Orlando Hernandez{3} on drug and weapons charges. With both Colombia and Brazil having presidential elections this year, how the political leaning map of Latin America{4} fleshes out could be very interesting, and we will expand a bit on our thoughts in a Brazil later section.

For the first time in their 88-year history, Volkswagen{5} closed a production plant in Germany. All the while, BYD{6} , the Chinese automaker, continues to make global inroads. Currently operating in 95 countries, they are building strategic beachheads in key global markets like Thailand, Hungary, and Brazil to service the respective spheres of influence.

Adding to the global move to spheres of interest, rumors of an add-on report to the heavily cited National Security Strategy{7} , and the supposed existence of a “classified version”, have the U.S. proposing the creation of a new grouping to take over from the G7, called the “The Core 5” {8}. Excluding Europe and tacitly acknowledging the “notion of an Asian Century,” remember one of our favorite and often-used tag lines: “Skate to where the puck is going to be, not where it has been”. {9}

There are several others, but we will push them to next month as there are some more pressing topics we would like to discuss.

Eating Crow

As this write-up is meant to both reflect back on what was 2025 and look forward to what could be 2026, we wanted to first start off with what we got completely 100% wrong. In our first-quarter write- up{10} , we actually believed what Trump had said while stumping. In hindsight, it's embarrassing to admit—given what has happened in the 9 months since—but at the time, we had hopes of seeing some type of global peace dividend.

Well, instead we get promises of even more war! With bombings and airstrikes {11} on Iran, Iraq, Nigeria, Somalia, Syria, Yemen, and Venezuela—and just this week, promises to increase the Department of War’s budget by 50%! {12}

…That said, we did get a lot right!

In our 4Q’2024{13} piece, we did start discussing how we foresaw the end of Globalism and the rise of spheres of interest, how tariffs would begin to shape global capital flows, and how we were fearful of economic weakness in Europe, with an emphasis on Germany. From forewarning on Greenland to even foreshadowing a return to a revised Monroe Doctrine. I think we actually got a lot more right than wrong!

When opportunity comes a knocking, Venezuela

We published some very quick thoughts on Venezuela on January 4th. Those thoughts can be found here (link) {14}.

We would like to expand on what we wrote earlier this week. In the few days that have passed since this incident, we have seen many media talking heads on CNBC, as well as Twitter experts, saying that many years and billions of dollars are needed to see any meaningful increase in production.

We are NOT in that camp. We are old enough to remember the First Gulf War, which saw Iraq invade Kuwait back in 1990. We saw production of oil go from 1.9 million barrels per day (b/d) in 1989 to ZERO in 1991, but we also saw that oil production returned to 1.9 million b/d by 1993. We urge our audience to recall the Scorched Earth {15} withdrawal that saw over 600 wells set ablaze.

There has been no carpet bombing in Venezuela, there have been no wells set ablaze by retreating military occupiers. What has taken place is neglect and, frankly sabotage {16}{17}{18} by forces against the Venezuelan Government.

Many of those same doomsayers question the true amount of oil reserves that the country has. The official number is 300 billion barrels. Yes, we know the oil in Venezuela is very heavy and sour (meaning high sulfur content), so per barrel it's less valuable than Saudi light or West Texas Intermediate, but for now let us just focus on the number of barrels of reserves.

Let us use what Rice University Latin American Energy Institute’s Francisco Monaldi {19} estimates as the true recoverable amount.

Monaldi estimates the true recoverable amount is closer to 100 billion barrels — so roughly one-third of the commonly thrown-around number. However, we must point out that at 100 billion barrels that would still rank above Russia with 80 billion and on par with Kuwait (which is also around 100 billion), over two times the USA (45 billion), and 23 times more than Canada (4.3 billion){20} .

Let’s put that into a financial perspective. As we mentioned above, Venezuela oil is heavier and has a higher sulfur content and as such has historically traded at a discount to Brent of around $20 per barrel. As of January 10th 2026, Bloomberg shows us a price of $63.34 for yesterday’s close.

So just for fun, we will take an even larger discount of $30. So $63.34 minus $30.00 equals $33.34. And since I like round numbers, let’s round down again to $30 value.

30 times 100 billion is $3 trillion. As someone who deals with numbers a lot, and as we have seen our collective governments engorge on debt, I think many have lost the magnitude between millions, billions, trillions.

To help illustrate:

3 million is 3,000,000

30 million is 30,000,000

300 million is 300,000,000

3 billion is 3,000,000,000

3 Trillion is 3,000,000,000,000

Also, to help put this into a different perspective, using the reduced reserve estimate and looking at current oil production of around 1 million b/d: IF production were able to get to 3 million b/d (triple the current rate), given that number of reserves they in theory could produce at that amount for 91 years (100 billion / (3 million per day * 365) ≈ 91 years).

But Exxon CEO said…

That Venezuela is uninvestable{21} !?!?! Well, again, this is the author’s opinion. We think you heard a lot of whining and posturing. We do not think we are alone in the surprise that the Trump administration has blurred the lines between government and the private sector.

We have known oil companies to operate in some of the scariest, most inhospitable, and far-off regions—like Syria, the North Sea, Iraq (Kurdistan), the Ecuadorian jungles, and areas controlled by Colombian paramilitary groups. What we think is that Big Oil is looking for Daddy Trump {22} to offer some type of guarantee or capital. Just look at what Trump did in regard to Intel, the chip maker, taking a 10% stake in the company estimated to be around $8.9 billion.

If Venezuela were so uninvestable, why did Chevron stay? How about Repsol or Eni? Why were the Chinese and Russians still there? Even putting the heavy oil of the Orinoco Basin aside, there’s plenty of low-hanging fruit in the conventional basins — Maracaibo and Monagas — both of which are exactly where Chevron still operates. And finally, not to be mean, but while Chevron chose to stay in Venezuela… they chose to leave California .

So yea we actually do think Venezuela is a big deal.

Plata o Plomo

Plata o Plomo{25} — a Spanish expression meaning "silver or lead" (in other words, money or bullets). In pop culture, the phrase became widespread thanks to the Netflix series Narcos, which focused on Pablo Escobar. As many know, Escobar was a ruthless Colombian drug businessman who built his empire on violence, fear, and intimidation.

In our Venezuela-focused piece from earlier this week (again, here is the link{26} ), we wanted to revisit and flesh out a bit more on potential losers. As we foreshadowed back in the 4Q of 2025 and again earlier this week, we thought rhetoric around Greenland would significantly heat up—and lo and behold, just yesterday, January 9, 2026{27} , while taking questions surrounded by many in the oil industry there to discuss Venezuela, a reporter asked Trump about Greenland. The exact quote was: “I would like to make a deal the easy way, but if we don’t do it the easy way, we’re going to do it the hard way.” Plata o Plomo.

Another country we would like to expand upon is Brazil. As we mentioned in the piece earlier this week, we do worry that Brazil could increasingly be in the crosshairs of this administration. Of the original 4 BRICs {28} (Brazil, Russia, India, and China), the most vulnerable — in terms of internal divide, upcoming presidential elections, and, as we always say, “Geography is Destiny” — is clearly Brazil. Among its regional peers, it’s the only one that could vie for any meaningful influence. In the gran game a divide and conquer starts with your weakest link.

We hope things go the easy way but need to be cognizant if they go the hard way.

So what does the Future hold?

This year will see, for sure, a change at the helm of the Fed and possibly some shuffling of other Fed governors, depending on how the Supreme Court rules. But by hook or by crook, we have a high degree of confidence that this administration will use every tool they can to lower interest rates {29}.

We also think we will continue to see a weaker dollar, as it provides an advantage to US-based companies trying not only to compete against imports but to make US-made products cheap to the rest of the world.

As we have now been pounding the table, we see this move away from globalization as wonderful for Emerging Markets. Countries will be better able to compete and flourish where they have a natural advantage, and the global move to spheres of interest will continue to create opportunities (and pitfalls). But having an active manager—as opposed to an index—will now become more important across all asset classes, but especially in Emerging Markets.

[1] en.wikipedia.org/wiki/Mosaic_th…

[2] genius.com/Richard-obrien…

[3] nytimes.com/2026/01/03/wor…

[4] x.com/eliant_capital…

[5]nytimes.com/2025/12/16/bus…

[6] byd.com/us/about-byd

[7] whitehouse.gov/wp-content/upl…

[8] korybko.substack.com/p/the-c5-would…

[9] brainyquote.com/quotes/wayne_g…

[10] rvx-am.com/wp-content/upl…

[11] militarytimes.com/news/pentagon-…

[12] @realDonaldTrump/posts/115855894695940909" target="_blank" rel="nofollow noopener">truthsocial.com/@realDonaldTru…

[13] rvx-am.com/wp-content/upl…

[14] x.com/RayZucaro/stat…

[15] en.wikipedia.org/wiki/Kuwaiti_o…

[16] bbc.com/news/world-lat…

[17] businessinsider.com/venezuela-blam…

[18] boereport.com/2025/12/15/ven…

[19] linkedin.com/posts/francisc…

[20] opec.org/assets/assetdb…

[21] x.com/Acyn/status/20…

[22] x.com/nicksortor/sta…

[23] newsroom.intel.com/corporate/inte…

[24]californiaglobe.com/fr/leaving-cal…

[25] youtube.com/watch?v=xl8zdC…

[26] x.com/RayZucaro/stat…

[27] x.com/WallStreetMav/…

[28] en.wikipedia.org/wiki/BRICS

[29] cnn.com/2026/01/08/bus…

YouTube

English

Venezuela Market Thoughts

By Raymond Zucaro

1/4/2026

Trumpire Part 2:

2026 has started off with a strong continuation of what we've been discussing for the last year; with our "spheres of interest" piece here (link ) and, more specifically, our August piece on Venezuela (here ). We just wanted to share some quick thoughts, and we are not making any moral judgments. As this author likes to say, our role is to be an umpire and just call balls and strikes, but given our profession, how (we think) the market will react.

A little background

The actions taken by the United States in the early hours of Saturday, January 3rd, 2026 with the “capture” of Nicolás Maduro and his wife, the former Attorney General of Venezuela and current deputy in the National Assembly, Cilia Flores.

As we stated in our August piece specifically on Venezuela and our November market thoughts (link ), the recent National Security Strategy published on December 4th, 2025 , laid out a clear vision of the Western Hemisphere in the eyes of the White House going forward. We saw the many moving parts and heavy military hardware arriving in the Caribbean as a telltale sign that the Trump administration and their interpretation of spheres of interest was well underway.

We would like to point out two interesting aspects of the recent action. We understand that the CIA had been operating on the ground for “a while,” and the lack of military response to the US extraction reminds us of the fall of the Assad regime in Syria. We believe that key power brokers were paid in some way to allow the removal of Maduro. We find it extremely interesting—in Trump’s press conference—that Rubio had been in close contact with Delcy Rodríguez, according to Trump and that she was willing to work with the US administration . We think one should discount her public statements that are for local consumption.

Why it seemed too easy?

Under Chávez and later Maduro, key political groups were given strategic parts of the economy to oversee, so while the broader population suffered, these key players had access to cash flow. We think the recent seizures of oil tankers changed the calculus for those groups and made the idea of giving up Maduro much smoother than it would have been otherwise.

Maduro was not driving this bus, Trump was…

The other critical thing Trump mentioned in his press conference was his comments about María Corina Machado. Trump stated, "I think it would be very tough for her to be the leader. She doesn't have the support within or the respect within the country." He described her as a "very nice woman" but emphasized that she lacks the necessary domestic backing.

Historical lesson learned(?)

As a long-term stakeholder in all things Venezuela, we share his views. Machado is a very polarizing figure who has long discussed political retribution against the followers of Chavismo, a stance that would make running a country as divided as Venezuela nearly impossible. We saw firsthand the myopic decisions of Pedro Carmona during the April 2002 coup in Venezuela and his "Acta de Constitución del Gobierno de Transición Democrática y Unidad Nacional," which was seen by many, including the author, as an attempt to erase Chavismo and purge the government of those sympathetic to Chávez and his Bolivarian reforms.

We view those types of actions, whether it be the 2003 Iraq Coalition Provisional Authority decree “CPA Order No. 1” to purge the entire government of all members of the Ba’ath, Hussein’s party, or Carmona’s actions—as extremely destabilizing in the short, medium, and long term. We were pleased, at least at this point, that the Trump administration does not seem to be making the same mistake here (yet?).

Implications for Venezuela

Ok so what does this mean for Venezuela and the Venezuelan people? In the January 3rd press conference, Trump was very clear that US oil companies were going to run the Venezuelan oil industry. Current daily oil production in Venezuela is estimated to be between 900k and 1.1 million barrels per day. With the lifting of sanctions, fresh investment, and new technology, we could envision daily oil production doubling in 1 to 2 years. While this may sound ambitious, we would like to point out that just over 10 years ago daily production was around 2.5–3 million barrels per day—and that is well below the country's peak daily production of ~3.7 million barrels per day back in the 1970s, interestingly before Venezuela nationalized oil production from some of those same majors that may return.

This return of oil production alone—Francisco Rodríguez, the former head of Economic and Financial Advisory for the Venezuelan National Assembly from 2000 to 2004 and Chief Andean economist at Bank of America from 2011 to 2016—thinks could drive strong growth. With a normalization of oil production, he believes “Venezuela could experience high, double-digit growth for several years. My {Rodríguez’s} estimates, which coincide with those of other economists, including those who work for Machado, is that Venezuela could see its GDP per capita in U.S. dollars triple in the next decade.”

But as we wrote in our first Trumpire piece, we do not know if many investors truly understand the investment potential of Venezuela beyond oil. The Kobeissi Letter estimates that iron ore reserves and rare earth elements alone represent $600 billion in value. This is in addition to their estimates of $800 billion for natural gas , $22 billion for gold, and $35 billion for bauxite . The list of natural resources that Venezuela possesses but is barely producing is staggering , and with the lifting of sanctions and even slight moves toward a pro-business stance, the recovery for the country and its people could become one of those economic miracles and turnaround stories that end up in future textbooks.

Winners and losers

What are some potential repercussions from this? Just some thoughts and not meant to be exhaustive:

Losers:

Colombia: more pressure against Petro in the run-up to elections on May 31, 2026. There are an estimated 2.8–3 million Venezuelans living in Colombia today. If there is a return to economic expansion, many of these people could return.

Nicaragua and Cuba: the bold actions taken by the Trump administration clearly show they will back their threats with action, and Marco Rubio—given his personal background—has a particular vengeance against these two leftist governments.

Avianca, LATAM, and Copa Airlines: if direct flights to and from the US and Venezuela are reopened (which seems likely post-sanctions lift), some of these high-margin routes could be impacted by the return of US airlines to Venezuela.

Denmark. Greenland: clearly, in Trump’s mind, this huge land mass with its resources and key shipping routes needs to be under US influence or protectorate .

China. Loss of influence in the Americas. While Venezuela was only producing +/- 900k barrels, what was shipped to China in the grand scheme of things was not that important and any supply could be easily made up by Russia or Iran. Furthermore Trump said in the 1/3/2026 press conference that Venezuela would continue to sell oil to China.

Canada: Canada has been a large supplier of heavy crude oil to the US. While many see US oil production as high by historical standards (which is very true), the kind of oil the US is producing is light oil due to the shale revolution. However, many of our Texas- and Louisiana-based refineries are geared toward heavy crude—they were, after all, originally designed to refine exactly Venezuelan oil.

Mexico: not really a loser (yet), but one to keep an eye on. While the pretense of drugs and Venezuela has seemingly fallen to the wayside, the real drug funnel into the US still remains Mexico and the well-funded, entrenched cartels.

Brazil: I saved the most controversial for last. Brazil is Latin America’s largest economy and, as such, the only real regional peer to the United States—clearly putting it in the crosshairs. Trump has a clear hatred of the BRICS, and we cannot forget that the B is for one of the founding members of the BRICS alliance. Trump has stated that the BRICS were founded to undermine the US dollar, and Brazilian President Lula has been a large proponent of setting up a financial system away from the US dollar. Finally, Mike Benz has done extensive work on how the USAID system actively worked against the Bolsonaro government, and Benz has stated that, had it not been for the work of USAID, Bolsonaro would be president today. He even testified to the Congress of Brazil (his work can be found here , here , and here ). Given these reasons, one could easily see the US turning the heat on the burner a bit higher as we get closer to the October 4, 2026 (first round) presidential elections.

Winners

US consumers, if Venezuelan commodities come back on market consumer prices in the US could experience downward pressure. Also, lower inflation gives the incoming FED more arguments to lower interest rates.

Argentina, Chile, Honduras, and El Salvador are all clearly in the “with us” camp. In the National Security Strategy report, they mention using all means to sway countries in this hemisphere. So whether it be currency swap lines, ex-presidential pardons, sweetheart trade deals, or the sword—this administration is making it crystal clear: you cannot go against the Trumpire.

English