@Rayanbiotech@crisprspace It's not valued more "generously" because generosity implies that the market is being charitable to $BEAM. It's valued *higher* because they're much farther along, have a much better cash position, deeper pipeline, and proven management. And $PFE just opted in!

@VEGA_n1@crisprspace Your not wrong. You just proved my point, beam is the better company at this moment. However, it is valued much more generously than prime. Prime is just higher risk, higher reward. I definitely would have more confidence in beam at the moment, if thats what you’re asking.

@Rayanbiotech@crisprspace $PRME IPO'd at a terrible time so a lot of the cash issues are not their fault. The other companies benefitted from the 2020-2021 bubble. But losing a CEO is not good. But 2.5 yrs after IPO, $BEAM already spun out Orbital and had $400 in cash from deals. What has $PRME done?

@VEGA_n1@crisprspace well they are an early stage company and was founded years after beam. the way the company is run is very similar to beam and they even shared executive management at one point. prme just needs capital injection at this point and focus on cf.

@Rayanbiotech@crisprspace $PRME might have good technology, but there's very little evidence that they're a great company. What great decisions have they made? They fired their last CEO

@VEGA_n1@crisprspace Hard to say, both are great companies. It just depends on risk/reward. Beam is a pretty safe bet regardless of arbitration, but you’re going to get less returns versus prime if it is successful. Prime’s financials are my main concern and this arbitration won’t help unfortunately

This is a bad take.

$KALV was bought for its HAE on-demand drug.

It was a horrible buy considering on-demand usage will plummet with $NTLA and $PHVS prophylactic option coming.

@GeneInvesting@crisprspace yeah i don’t think beam wins out right either just because of the relationship of the companies and it wouldn’t make sense for beam because of all the prime copycats entering the market. I do think prime is going to face some consequence such as a 10% royalty and milestones.

Obviously some compromise was always in the cards. I don’t think the market ever expected prime to when outright/100%.

The beam outperformance lately has way more to do with lucky cash inflow from RNA company buyout and the bigger news was the AATD accelerated approval agreement with FDA.

There is a reason Wedbush is in my Top 3 for worst biotech analysts of all time.. $NTLA

I’ll say this one more time: NO HAE PATIENT GIVES A SHIT AT WHAT THE BLINDED PERIOD SHOWS

“We continue to view the inability to discontinue dosing… a commercial limitation…”

WTF 🤬 ZERO patients went back to their prophylactic medication once allowed to after Week 28 and safety was essentially perfect.

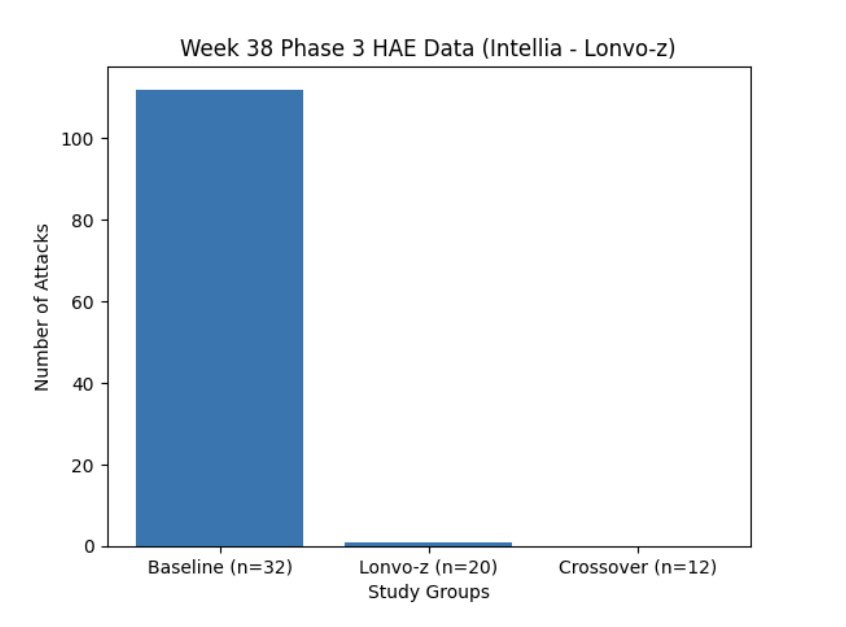

The month of Week 36 saw 32 patients experience a total of 1 attack. Baseline values would’ve expected ~112 attacks per month (a 99.1% decrease in attacks).

Does Wedbush understand how to look at data? Or do they just use AI to sift through surface level information 🤷🏻♂️

“Nierengarten kept his neutral rating and 12 price target on Intellia stock.”

Offering price was Grade F imo. $NTLA

This is strike 2 I’m personally giving to the management (first was handling of Grade 4 events/mitigation in ATTR CM).

They had 2 better options:

1) Use your ATM

2) Wait for June conference where you can hopefully show a bit more data

$15+ should’ve been the goal here and not getting close was a big failure imo.

@AlexHumphries25@GeneInvesting Yeah rough math puts peak sales of wilson’s, aatd, and smaller subset of cf at 1.2b peak sales.But if you take away 50% from deals we are looking at 600m revenue still with dilution.They got unfortunate that most big indications other than cf or some neuro are taken by others.

@Rayanbiotech@GeneInvesting would not be surprised if they go straight for a buyout from pharma, seems like a good deal at this stage, their current programs arent fantastic for their financials even if approved.

@AlexHumphries25@GeneInvesting I really do like prime, but their financials are not looking great. Even if they get partnerships it will likely result in loss of economics in its programs and dilution regardless. I also think that the arbitration with beam is a headwind. CF is really key for them but far away.

@GeneInvesting management is the reason this company is not in the 30s, lack of ambition and aggressive targets is my main crux, this is making me consider selling early, prime is managed far better and potentially higher upside in the same timeframe.

$NTLA stock price will recover to eventually $20+ in a couple of months as the market realizes hae will get approved 1H of next year and will have a speedy sales ramp up unlike ex vivo treatments. If no more safety signals for attr by then, buyout will be imminent at 6-8b.

@mo_tawfik89 The company definitely looks like it’s positioning itself for a buyout. They don’t really have much of a platform as they eliminated any chance of that when they got rid of aatd and the hemo B opt in (to be fair for the right reasons). Above 6b, I think it’s definitely worth it.

@GeneInvesting@lainspiron9071 The stock has previously sold off on good data, but then picked back up a couple of days or weeks afterwards. I don’t feel anything different from when the ph2 hae or the recent attr pn data was released. Unfortunate timing for the offering, but smart money will buy in.

I’ll just leave this here…

$NTLA bears: this data is ok 🤷🏻♂️

Me: you obviously didn’t look at week 36

Week 36:

• 20 Lonvo patients w/ 1 total attack

• 12 placebo to Lonvo w/ ZERO attacks

That’s 1 attack versus 112 at baseline (assuming 3.5 baseline average holds)

🟰 99.1% attack rate reduction