Red Knight Finance

1.7K posts

Red Knight Finance

@Redknight8811

Semiconductors, Photonics, AI and other Technology related Stocks.

Katılım Eylül 2021

893 Takip Edilen440 Takipçiler

New stock alert 🚨

Not sure if anyone has seen me posting about it this week but I decided to take the plunge (albeit super late)

#HDD Hardide Plc

Another fantastic UK company a bit like #FTC in terms of right place right time

What do they do?

They develop advanced tungsten coatings to in simple terms improve and reduce corrosion of metal parts

Some examples why I am excited below:

Space 🛰️ - Hardides CVD technology (chemical Vapour Deposition) coats atom by atom so it’s incredibly precise, this can allow it to protect the insides or complex satellite components, also as it’s extremely thin (as I said atom by atom) its relatively cheap to send to space compared to anything else

My hope is that Hardides coatings are picked up by the likes of SpaceX as it’s much easier to protect vs sending someone up to fix!

AI 🤖 Hardide has a product called Hardide-W which is tailored for the precision and chemical sensitivity required in chip manufacturing, again giving it exposure to an incredibly bullish market

Defence 🛑 Hardide-A is the key product here, tungsten coatings are used across the entire defence supply chain and with larger percentages of GDP being spent on defence PLUS remember the us is banning tungsten sourced from China for military use in 2027

Finally, the financials 💰 management expect revenue to be ‘materially ahead of expectations’ so at £30m market cap this could be the next BIG UK unicorn, right place right time with excellent exposure to almost everything

Also you might say does the tungsten price not hurt their economics? Management hedged which is a huge tick ✅ for execution and leadership.

English

@UKsterlings Well, another reason was learning about Palantir(PLTR) and how it did like close 20x within a year got my attention 😂

English

@Redknight8811 Yh the uncertainty in crypto is also what shys me away from it now

English

What made you start investing. Was there a single moment where you was like it’s time to start?

For me, I lost 50k over the last 3 years gambling and in crypto I said to myself at the start of the year, this year has to be different and learnt about isa’s and investing smartly

English

@JonkooTrades Yeah, pretty much. So, I don't even bother having any exposure there.

English

Is the rare earth stock game just a massive Pump -> Dump -> Repeat scheme?

Just see these stocks like $USAR $UAMY $CRML etc doing massive gainers just to give back everything next day.

Any thoughts?

The Trend Sage@JonkooTrades

So wtf did $CRML shit the bed for in the last hour of trading? Looks like a bunch of shorts since it flipped to “hard-to-borrow” on my broker. Also with 30% short interest, reminds me a little bit of $ONDS here. $CRML is a great business as well though, not sure why this never holds a pump. Anyone has ideas?

English

@HunterAllen4 I am new to this space. and I found you on first day, trust me, you're doing fine.

English

I feel like for someone with almost 6700 followers the algorithm is terrible.

I’ve got a few good posts but nothing is sustainable like others I see. People literally out here changing one word and people aren’t calling them out?

I provide value.

I give daily setups and I give small cap opportunities.

Do I need to make a separate chat for my unusual volume calls?

Should I just FOMO into what works on here.

Hear me out, providing value to you all is most important always.

X COMMUNITY AND YOU ALL ARE FIRST

I’m just confused. Im frustrated. Maybe x is confused by my niche too.

Waiting game guys..

English

@HunterAllen4 @antibearthesis Do you see ONDS as close to like for example Lockheed Martin or Raytheon? in the future I mean. price wise...

English

@antibearthesis I agree w you on everything except having $ONDS on the bottom is a disgrace to humanity this is generational buy still and still will be when it’s 20$

English

$TSSI

But this is a generational setup under $20 🤔

$TSSI — up ~2800% over 5 years, +135% YTD, and still flying under the radar.

Now look at the STORY:

~$245M revenue

+71% gross profit growth (Q)

+535% net income growth (Q)

+89% operating income growth (Q)

+380% EPS growth (Q)

+133% EPS growth

$118M current assets

$43M net cash

All at ~$465M market cap.

AI infrastructure is exploding — and $TSSI is quietly building the backbone.

This is what people ignored in:

• Arista Networks at $15 in 2019

High growth. Early stage. Misunderstood.

$TSSI isn’t just a $20 stock…

It’s a micro-cap version of $ANET — positioned at the center of the AI data center buildout.

English

@ryansfinance Not sure about ONDAS. I mean, I like the stock but.. I don't see as much upside as the others.

English

If you had £20K and split it evenly into these 4 stocks ⬇️

$ASTS - 77 Shares

$IREN - 143 Shares

$ONDS - 599 Shares

$HIMS - 222 Shares

I would say you finish the year in the £50K-£100K zone 🚀

All of these at their current valuations tbey are severely undervalued and 8 months from now these prices will be a steal 👍🏼

Once my $IREN reaches £20K this might be the playbook I follow 🤔

English

@JSE_Invest How much is #FINV paying you for this? Money well spent. 😂

English

Here's a no brainer from latest letter - FinVolution ($FINV): The Best Value Money Can Buy

There is a company listed on the New York Stock Exchange that generated ~$374m in net income over the last year, has a net current asset value of ~$1.7bn (net-net), book value of ~$2.46bn, and a market cap of $1.2bn. It's a no brainer in my books.

The company is growing its international business at 32% a year, just launched a Mastercard-backed credit product in the Philippines, acquired a profitable Australian lender, is buying back stock at a record pace, and raised its dividend for the eighth consecutive year. Despite this, it trades at roughly 3.3x and a fraction of book. The company is FinVolution Group ($FINV). Almost nobody is paying attention, and I think the reasons are superficial.

The Balance Sheet

This is, like literally every single of my best investments historically, a matter of basic and simple arithmetic. A teenager can figure out that the company’s market cap is dislocated from its balance sheet.

As at 31 December 2025, $FINV reported total assets of RMB 25.4bn and total liabilities of RMB 8.6bn, giving you shareholders’ equity of RMB 16.8bn. That is around $2.3bn at current exchange rates. At around $4.70/share, the company’s market cap stands around $1.2bn. The simple math is you are buying the equity at about 0.50x book value; half price.

I’ve seen this before; normally said company’s operations are in a state of disrepair (e.g. Murray & Roberts), or cyclically unprofitable (e.g. Daqo; still a no brainer). The balance sheet quality here is genuinely unusual for a financial services company. Cash and cash equivalents stood at RMB 4.3bn. Short-term investments added another RMB 3.0bn. Together that is RMB 7.3bn of liquid assets, or roughly $1bn, sitting right there on the balance sheet. That alone pretty much covers a very large proportion of the company’s entire market cap. Total debt is modest at approximately RMB 1.1bn, so the company holds substantially more cash than it owes in debt.

The debt-to-equity ratio is 6.7%, which is negligible. The leverage ratio fell to a historical low of 2.4x during the year. Provision coverage sat at 517% at Q3, reflecting deep conservatism in how they reserve against loan losses. The interest coverage ratio, at 375x EBIT to interest expense, is absurd for a financial company. This is a fortress balance sheet by any reasonable standard and it doesn’t take a neurosurgeon to arrive at that conclusion.

Perhaps the most useful number for a value investor: current assets substantially exceed total liabilities. If you take short-term assets of approximately RMB 20.9bn against total liabilities of RMB 8.6bn, you have a net current asset surplus of over RMB 12bn. That puts $FINV in rare territory for any listed company, let alone a fintech, where it could theoretically liquidate its current assets, pay off every single liability on the balance sheet, and still have more than its entire market cap left over. A classic net-net, except it’s actually super profitable. That brings me to my next point.

The Income Statement

Full year 2025 group revenue came in at RMB 13.6bn, up 3.8% on the prior year. Net income was RMB 2.55bn, up 6.6%. These are modest headline numbers, and they obscure what is actually happening underneath. The China business, which still represents about 75% of revenue, decelerated meaningfully in the second half. Regulatory authorities issued new guidance aimed at reducing consumer financing costs, which compressed volumes and required tighter underwriting. Q4 net revenue fell to RMB 3.02bn from RMB 3.46bn in Q4 2024, and net profit dropped to RMB 415.5m from RMB 680.8m. The 30-day loan collection rate dipped from 88% to 86%, and the CM2 flow rate (a measure of credit migration into delinquency) rose from 0.61% to 0.77%.

Those are real pressures, and the company has guided for a 5% to 15% revenue decline in 2026 at the group level. That is the headline that has scared people. But context matters enormously here.

First, the China deterioration appears to have peaked. Management noted that early risk indicators peaked in mid-December 2025 and began stabilising. They are deliberately tightening underwriting toward higher-quality borrowers, protecting unit economics and keeping vintage loss rates stable at 3%. This is a company choosing to shrink volume to protect margins, which is exactly what a well-run lender should do in a tougher credit environment. The take rate held steady at approximately 3%, and funding costs continued to fall, down 20 basis points quarter-on-quarter to 3.4%. These are not the metrics of a company in distress.

Second, the international business is on an entirely different trajectory.

The International Inflection

This is where the real story sits, and it is the reason I think the current valuation is so disconnected from the underlying trajectory.

International revenue reached RMB 3.3bn for the full year, up 32% year-on-year. International transaction volume grew 38.6% to RMB 14bn. In Q4, the international segment contributed 31% of total revenue, up from 21% in Q4 2024. Unique borrowers in international markets grew 133.8% year-on-year to 3.8m. In the Philippines, the new borrower base grew more than 3x year-on-year, and embedded e-commerce partnerships (Buy Now, Pay Later) now account for roughly 43% of Philippine transaction volume, up from 30% a year ago. Indonesia has achieved profitability. The Philippines has achieved profitability. Both markets are scaling rapidly with strong unit economics.

What interests me most is the delta between the two segments. China revenue is decelerating, and international revenue is accelerating. In FY2024, international was 19.4% of total revenue. In FY2025, it reached 24.6%. In Q4 2025, it was 31%. Management is targeting 50% international by 2030. At the rate things are moving, they could get there ahead of schedule.

There is a mathematical inflection point approaching where international growth fully offsets or exceeds China’s decline. Run the numbers (again, this is a fairly basic calculation): if China revenue falls 10% and international grows 30%, on their respective bases from FY2025, total group revenue is roughly flat. If international outperforms that, group revenue grows.

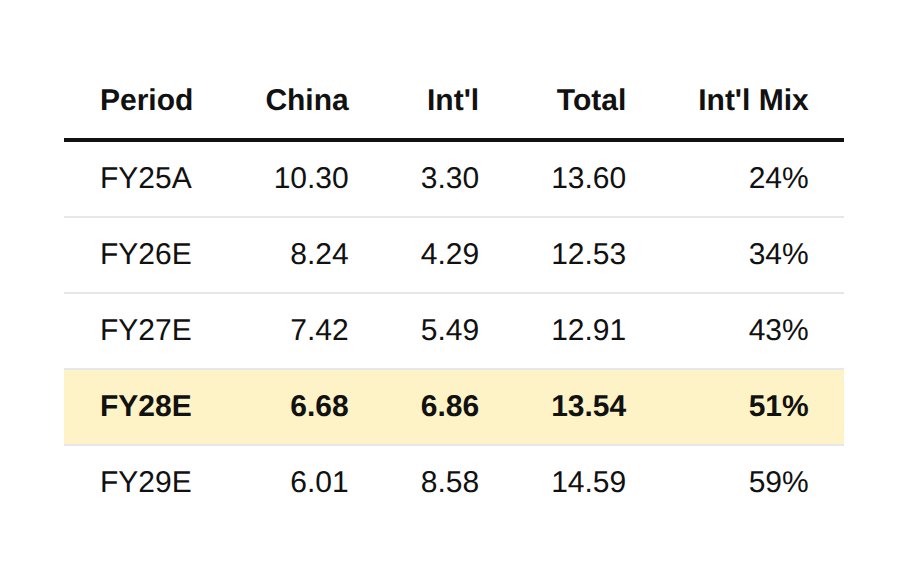

The deceleration in China and the acceleration outside of it are converging, and the gap is narrowing quarter by quarter. The market is pricing FinVolution as though the China headwinds are the whole story. They are only half the story, and they are the shrinking half; the aggressive growth story is about to become the main event. See the attached table as indicative; these assumptions are my own, but I don't think they're unreasonable. The assumption does not factor in any potential M&A upside over the next few years.

The inflection should occur in FY2028. My model suggests that the moment international revenue surpasses Chinese revenue happens two full years ahead of management’s generic 2030 ambition.

Likelihood and Factors

This inflection has a high probability, with the timing only slightly flexible. The driver here is pretty basic math: China is structurally contracting by design, while international has multi-country tailwinds and proven product-market fit. We would have to see meaningful reversal in the rate of international, say down to 20% from the >30% current (gaining momentum) while also assuming the China business stabilises completely (in any case a positive) and it never declines another yuan (more realistic is sustained slow bleed), for the intl and China revenue segments contribution to only equal out by 2030. Given the momentum in the Philippines and Australia, the 2028 timeline I give seems more realistic.

The knock-on impacts cannot really be overstated from a market perspective. When this inflection hits, FinVolution’s identity inverts. Today, it is viewed as a distressed Chinese lender with some side projects. By 2028, it becomes a fast-growing, diversified multi-national fintech with a substantial legacy cash-cow business in China. At the current valuation (3.3x P/E), the market is pricing in the China decline (Column 2) but is ascribing zero probability, or mathematically, negative value, to the multi-billion RMB acceleration (Column 3) that is guaranteed to eclipse it.

The Mastercard Partnership and Strategic Expansion

On 8 April 2026, FinVolution and Mastercard jointly launched the Luvit Card in the Philippines. This is a virtual and physical credit card, backed by Asia United Bank as BIN sponsor and MatchMove as technology partner, that allows users to make purchases across Mastercard’s entire global merchant network and repay in instalments. Users can be approved in minutes through FinVolution’s proprietary AI underwriting.

This is a significant product expansion for several reasons. It moves FinVolution beyond pure unsecured digital lending into card-based credit, which has much higher daily usage frequency and stickier customer behaviour. It plugs into Mastercard’s global acceptance network, which means FinVolution’s Filipino borrowers can now transact with millions of merchants worldwide. This now gives FinVolution a product architecture that can be replicated across its other Southeast Asian markets.

The Luvit Card is part of a broader pattern. FinVolution has built partnerships with 128 financial institutions across its markets. It has facilitated over $171bn in cumulative loans. It has served 40.7m users. It operates across China, Indonesia, the Philippines, Pakistan, and as of Q4 2025, Australia, following the acquisition of Fundo, a Sydney-based digital lending platform holding an Australian Credit Licence.

The Fundo deal is interesting because it represents FinVolution’s first entry into a developed market. Australia’s unsecured lending market is approximately (AUD) $33bn. Fundo was already profitable and highly automated, which made it a natural fit for FinVolution’s LEGO+ global technology platform. The company intends to use its risk pricing and operational efficiency to scale Fundo significantly. From a strategic perspective, having a presence in a developed, well-regulated market alongside its emerging market operations gives FinVolution both a diversification benefit and a credibility benefit that the share price currently assigns zero value to.

Capital Allocation and Shareholder Returns

In 2025, FinVolution returned approximately $182m to shareholders through buybacks ($107m) and dividends ($74.5m). That represents a 50% payout ratio on net income. The Q4 buyback alone was $40.7m, the largest quarterly buyback in the company’s history outside of the concurrent buyback with the convertible note issuance.

The dividend was raised 10.5% to $0.306 per ADS, marking the eighth consecutive year of dividend declarations. At the current share price, that implies a trailing dividend yield of roughly 5% to 6%. Add the buyback yield and you are looking at total shareholder yield approaching 12% to 15%.

The company also executed approximately $38m in buybacks in Q1 2026 alone, with roughly $74m remaining under the current $150m buyback authorisation. Management personally invested $1.9m in share purchases during the year, which is a straightforward alignment signal, albeit minimal. Note too, as I’ve mention in previous letters, the Chairman and co-founder owns ±30% of the shares outstanding.

In June 2025, FinVolution completed a $150m convertible senior notes offering, which provides additional financial flexibility without meaningfully diluting existing shareholders at these price levels.

Valuation

Here is where I get pretty enthusiastic. At $4.65 per ADR and approximately 250m ADRs outstanding, the market capitalisation is roughly $1.15bn. TTM net income is approximately $350m (RMB 2.55bn converted). That gives you a P/E of approximately 3.3x. The price-to-book ratio is approximately 0.50x.

To restate the obvious: you are paying 3.3 times earnings for a company that is profitable, well-capitalised, growing its international business at 30%+, returning half its earnings to shareholders, buying back stock aggressively, has more cash than debt, and trades at half of book value.

The consensus analyst price target is around $7.60 to $8.30, implying 60% to 80% upside from here. Analysts have a unanimous Strong Buy rating. This is unusual for a Chinese-listed ADR, where most analysts tend to be cautious given the geopolitical and regulatory overhang.

The most conservative way to think about valuation is asset-based. Shareholders’ equity is $2.3bn. Even if you apply a 50% haircut to everything on the balance sheet that is not cash or short-term investments, you still arrive at a value above the current market cap. Net cash and short-term investments of approximately $850m cover roughly 75% of the entire market cap. You are effectively paying a few hundred million dollars for a business that generated $350m in profit last year.

On an earnings basis, even if 2026 revenue falls 15% (the bottom end of guidance) and margins compress somewhat, the company should still earn somewhere in the range of $250 to $300m. At the current market cap, that is a forward P/E of roughly 4x. For reference, the S&P 500 trades at around 22x earnings. US-listed Chinese fintechs as a group trade at 4x to 6x. FinVolution is at the bottom of the range, despite having one of the best balance sheets and the most credible international diversification story in the sector.

The Risk

I do not want to pretend there are no risks. There are several, and they are real.

Chinese regulatory risk is the obvious one. The interest rate caps and consumer protection regulations that suppressed volumes in H2 2025 may tighten further. FinVolution has guided for a revenue decline in 2026 for a reason. The credit environment in China is uncertain, and the broader macro picture (property, consumption, confidence) remains unresolved.

The ADR structure carries its own risks. The VIE (variable interest entity) structure that allows Chinese companies to list in the US is a legal grey area. Geopolitical tensions between the US and China could theoretically lead to delisting, although FinVolution has not been flagged under the HFCAA audit requirements to date.

Southeast Asian regulatory risk is also worth noting. The Philippines recently introduced new interest rate caps that management acknowledged would cause near-term moderation during a transition period. Indonesia and Pakistan both have their own regulatory complexities.

And then there is the simple fact that this is a consumer lending business. Credit risk is inherent. When the cycle turns, losses rise. The CM2 increase in Q4 2025 is a reminder of that.

But here is my view: the risks are known, they are priced, and they are arguably over-priced. When a company trades at 3.3x earnings, 0.50x book, with a net cash balance sheet, a 50% payout ratio, >45% insider ownership, 30%+ international growth, global partnerships with Mastercard, and entry into a fifth country, the market is pricing in a significant degree of permanent impairment. I see temporary headwinds in one market being offset by structural acceleration in several others that are increasingly more important and relevant from an income statement perspective.

Conclusion

FinVolution is the kind of stock that value investors claim to want: genuinely cheap, very well-capitalised, with a credible growth catalyst that the market is ignoring, and management that, on top of already having >45% interest in the shares outstanding, is actively deploying meaningful capital through buybacks rather than just talking about it. It is also the kind of stock that most people will not buy because it is a Chinese ADR in a sector they do not follow, at a price that looks like it must be cheap for a reason. Sometimes things are cheap for a reason. And sometimes the reason is that nobody is looking.

English

@HunterAllen4 SOL is alright, and maybe TAO. Outside that is pretty grim though.

HYPE is ok too. I really like SEI and SUI too.

English

Crypto outside of $BTC $ETH is DEAD

What’s the point? Just to get rugged

English

@HunterAllen4 Small cap and just good up and coming caps.

Bonus if European.

All in the right sectors too.

Post some random photonics not yet mentioned by Serenity too.

English

What posts do you all want to see?

IPO low float updates

Small cap comparison

Just good up and coming small caps

Large cap dips to take advantage of

I’m all ears 👂

COMMENT IDEAS

ILL PICK A FEW

English

@HunterAllen4 I like this, only concerns being mostly Africa. I believe they already left some markets there too.

English

look at $JMIA 👇

A generational buy at $8

Down 36% YTD but up ~290% over the past year — quietly curling.

FINANCIALS:

$188.9M revenue (2025)

+34% YoY (Q4 growth accelerating)

~$818M GMV

+27% orders YoY

Net cash ~$70M+

All at ~$1B market cap

📊 2026 ESTIMATES:

~$200M–$230M revenue

~25–30% growth

Path to EBITDA breakeven by late 2026

This is early-stage e-commerce dominance in Africa.

Lean operations. Improving margins. Scaling demand.

2010 $AMZN 7$ vibes.

$JMIA is a mispriced e-commerce giant people are overlooking.

English

$CMCM

-174M market cap

$CMCM Down 22% this month — while still up 56% YTD.

Now look at the FINANCIALS:

~$164M revenue

+11% YoY growth

~$474M total assets

~$216M net cash

Profitable (18% gross profit margin Q)

Let that sink in…

Trading BELOW asset value.

This is where opportunity lives.

People ignored this setup in early:

• Alphabet Inc. 2009 $GOOGL

• Meta Platforms 2013 $META

Small cap. Growing. Cash-rich. Mispriced.

$CMCM isn’t just a dip…

It’s a platform trading like it’s already been written off.

Don’t miss the entry.

English

@HunterAllen4 Great. been thinking about this one too!!

English

🚨 $GSIT (GSI Technology) DD

Beaten-down SPEC EDGE AI + SRAM hybrid play with asymmetric upside.

High risk. High reward.

💰 METRICS:

• ~$234M market cap

• ~$60M+ net cash (debt-free)

• ~$25M TTM revenue (legacy SRAM)

• ~150 employees

• Microcap AI + semiconductor pivot story

📊 PRICE ACTION:

• -10% 5Y (long-term laggard)

• -15% 3M (recent weakness)

• +150% 1Y (AI rerating volatility)

• +12% this week (momentum returning)

🧠 WHAT IT IS:

Legacy SRAM semiconductor company pivoting into compute-in-memory AI (Gemini-II APU)

Think:

👉 GPU alternative for memory-bound AI workloads

👉 edge inference (low power / low latency)

👉 defense + satellite + autonomous systems

⚡ CORE EDGE AI THESIS:

• Cornell-validated research: ~98% lower energy use vs NVIDIA A6000 on RAG-style workloads

• Compute-in-memory architecture solves “memory wall” bottleneck

• Targets edge AI where GPUs are inefficient (power/heat constrained systems)

🛰️ DEFENSE + SPACE PIPELINE (KEY):

This is where the narrative gets interesting:

• U.S. Army SBIR (edge AI feasibility + $250K contract)

• U.S. Air Force / AFRL SBIR $1.1M (object detection, ISR, GPS-denied AI)

• U.S. Space Development Agency radiation testing funding (~$752K)

• Multiple DoD/DoW-backed AI edge computing programs

🚀 2026 CATALYST STACK:

• Gemini-II POCs now active (defense + perimeter AI systems)

• Sentinel autonomous drone/security system (DoD-backed)

• ~$1M gov-funded integration milestone incoming

• Pilot deployments + “design win” pursuit in drones/satellites

• SRAM legacy business still growing double digits YoY

📡 COMMERCIAL/TECH POSITION:

• Compute-in-memory AI chip (Gemini-II)

• ~15W edge inference capability (ultra low power class)

• Radiation-hardened SRAM heritage (space/defense advantage)

• Early “edge AI infrastructure layer” narrative

📊 COMPARABLE EXPOSURE WATCH:

$NVDA $AMD $MRAM $NXPI $IOT $OSS

⚠️ IMPORTANT REALITY CHECK:

• Still microcap

• Still unproven APU scaling

• Still long defense/space sales cycles

• Still operating losses on AI side

• Highly speculative execution story

🧩 BULL CASE (ASYMMETRIC):

If even a few defense/edge AI design wins convert:

👉 narrative shifts from “SRAM company” → “edge AI infrastructure chip”

👉 rerating potential is exponential off small base

This is a SPEC edge AI + defense optionality setup.

Not hype. Not guaranteed.

Just asymmetric narrative + catalyst stacking.

Is $GSIT an opportunity you’re overlooking?

English

@HunterAllen4 I see NVDA with a much better demand and upside than PLTR

English

You wake up today and are forced to pick between

$PLTR & $RKLB

OR

$NVDA & $ASTS

Which TWO stocks are you more bullish to hold for the next 20 years? 😤

English

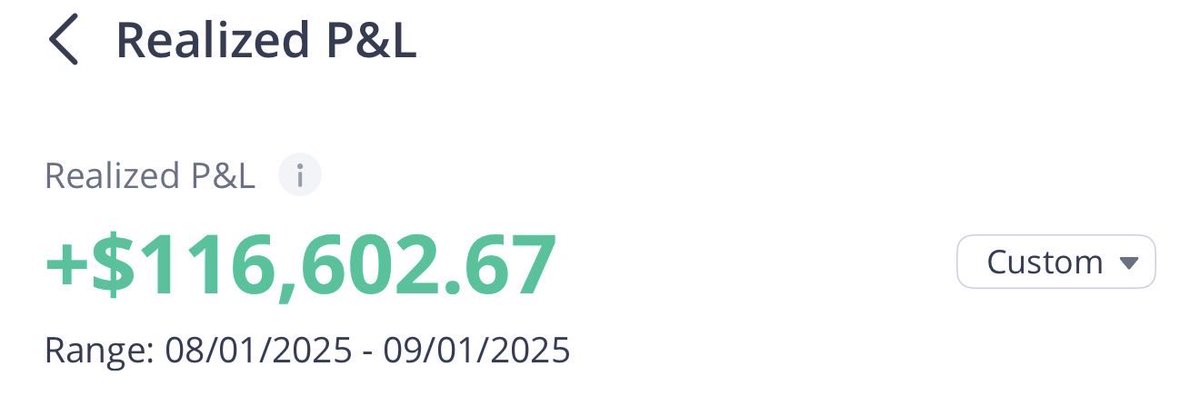

I’ve made over $116,000 in just 1 month using my custom CBC strategy.

So I made it a FREE TradingView indicator.

It tells you:

• when to buy

• when to sell

• when to stay out

I’ve been testing it for months, and it’s been printing. 📈

Like + Comment “CBC” - I’ll DM it to you.

(Must be following to DM)

$SPY $SPX

English

@NiohBerg All the worlds terrorism is caused by Arabs.

English

Most of the Arab residents were bought out of their homes and were more than happy to relocate - that's how awful this quarter was.

English

Jews had to pass through the narrow alley slum known as the Moroccan Quarter where they faced assault, harassment and all kinds of indignities. All of this just to access our holiest site.

Which is why in 1967 Israel bulldozed the entire quarter and made it into a plaza.

English