Sabitlenmiş Tweet

Rekter

2.6K posts

Rekter

@Rekter

Ex-JPMorgan trader. Institutional-grade analysis across crypto and equities. Risk is always better than regret.

Miami, Florida 🦩 Katılım Nisan 2024

116 Takip Edilen2.2K Takipçiler

$BMNR

I haven’t posted on this ticker too much. More active in the comments.

I did do a post about Tom Lee and BMNR earlier and I think it’s worth a read.

That said, I’m very concerned that as $ETH increases the mNAV is not closing the gap. I get the mNAV pulling away from 1.00 as ETH drops, but as it’s increasing and still pulling away? Very concerning.

My opinion something is fundamentally wrong with the value prop and a big firm must be dumping. Tom Lee really needs to address. The silence is contributing.

That aside, when ETH hits $5000, mNAV less than 1.00 or not everyone will make money, just not the premium we were promised.

English

$TSLA

Very obvious the last few months after touching $450 has been about neck breaking weak hands.

After today’s red rain of hell it only dropped less than 1%?

Clearly waiting for the upcoming ER and I think we see $500 and then $600 and then $700…

This next bull run will be epic!

English

$BULL

Basically one of the few bright spots in the market.

It retreated back 2%, but not before pushing over the 200MA on the daily for the first time since last July. That’s a statement.

The first touch is a knock and the second touch will be the door swinging wide open!

English

$CIFR

A bit overdone.

I’m not a big catching the knife guy, but this is similar to when a stock price shoots up to euphoria. Whatever the opposite of that is for a drop.

Big disconnect from reality imo for a company that has nothing to do with compute.

What do I know though!

English

Rekter retweetledi

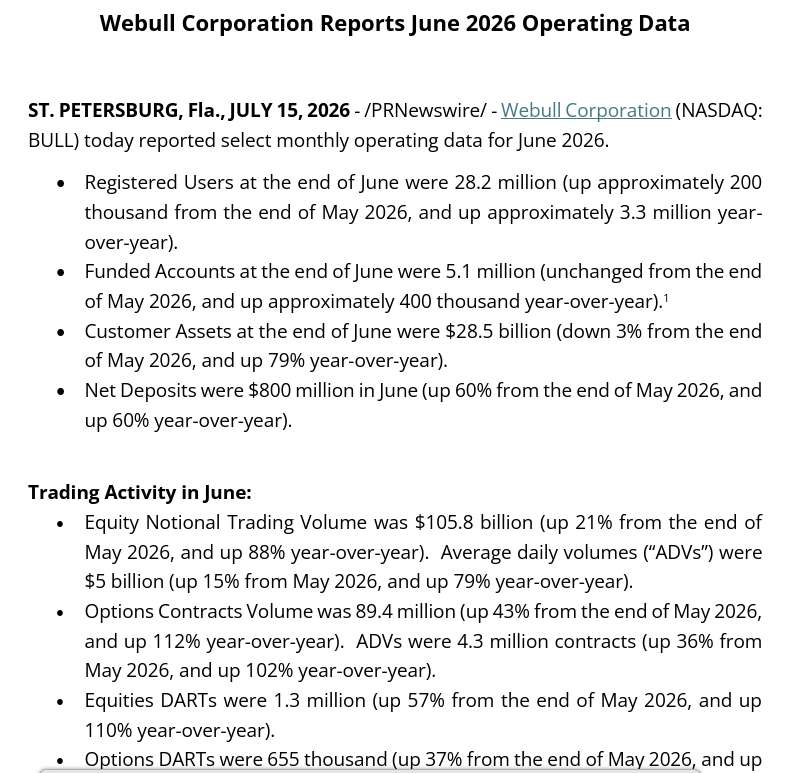

$BULL Webull Corporation Reports June 2026 Operating Data

English

Rekter retweetledi

$CIFR | Reversal Zone Update

Today’s low: $18.69, right at the 0.618 Fibonacci support, where buyers stepped in.

From -6% to green.

More work to do, but a good start.

Let the price action talk.

Asaf Naamani@AsafNaamani

$CIFR | Reversal Zone + Potential Bullish Cup & Handle Price is IN the corrective wave reversal zone at $18.80-$20.98. A hold and a confirmed reversal are what I’m watching next.

English

Rekter retweetledi

$BMNR

MNAV = 0.81

NAV per share = $19.74

$BMNR $16.00

$ETH $1,922

Dansk

$BMNR

MNAV = 0.83

NAV per share = $19.85

$BMNR $16.51

$ETH $1,934

🤔

Dansk

Rekter retweetledi

@ChrisMurphyCT Bro. We’re falling behind the crypto race. Bigger fish to fry homie!

English

The CLARITY Act is the bill supported by the crypto industry to increase their reach into our banking system and broader economy.

There are many problems with the bill, but most egregious is that is essentially legalizes Donald Trump's crypto corruption scheme.

Let me explain.

English

Rekter retweetledi

JUNE U.S. 🇺🇸 INFLATION DATA:

CPI 3.5% YoY, (Est. 3.8%)

CPI -0.4% MoM, (Est. 0.0%)

Core CPI 2.6% YoY, (Est. 2.9%)

Core CPI 0.0% MoM, (Est. 0.2%)

Français

Rekter retweetledi

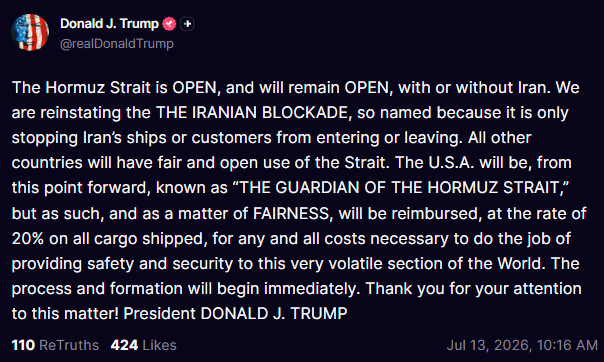

BREAKING: President Trump says the US is reinstating its blockade of the Strait of Hormuz for Iranian ships and customers.

Trump says the US will now be known as "The Guardian of the Strait of Hormuz" and will be "reimbursed" at a rate of 20% on all cargo shipped.

It appears the US is now imposing a blockade and fees to transit the Strait of Hormuz.

English

Overall Market & Sentiment —

Macro: The ceasefire is over, per Trump’s own words Friday, though he emphasized talks continue and Qatar has entered as mediator. Attacks in the Strait of Hormuz slowed shipping late in the week. Oil rose 5% to $71.61 WTI, still far below the $120 war peak but reversing the disinflation trend. The bond market sold off all week: the 10-year at 4.568%, up 8 of the last 9 sessions to the highest since May 22, the 30-year at 5.071%, the 2-year at 4.208%. The June FOMC minutes were hawkish, calling inflation well above the 2% objective. Rate-cut bets rose after the soft jobs report, with some desks putting September odds near 80%, yet bonds are pricing the opposite risk into Tuesday’s CPI. Consensus expects headline CPI near 3.5% year over year, while the Cleveland Fed nowcast tracks closer to 4%. PPI follows Wednesday, retail sales Thursday, and Warsh testifies before Congress. Housing softened as existing home sales fell 2.4% in June while the median price hit a record $440,600. The May trade deficit widened to $77.6 billion.

Micro: Earnings season opens Tuesday with the money-center banks: Goldman expected at $13.64, JPMorgan $5.60, Wells Fargo $1.72, Bank of America $1.10. Capital-markets banks are riding a deal boom while consumer lenders test whether Main Street matches the soft-landing narrative. Reserve builds and card losses remain the key tell. Delta beat, posting $1.56 versus $1.46 expected. The AI complex stayed strong: SK Hynix’s record $26.5 billion listing, Micron’s $250 billion U.S. investment plan, the Broadcom-Apple extension, Nvidia up 7.8%, Meta up 15%. Energy gained 3.1% on the week and is up 23% this year. Healthcare pulled back after all-time highs, with JNJ and UnitedHealth reporting next week. WD-40 rose 11% on earnings, EquipmentShare gained 17% on raised guidance. Polymarket filed with the NFA to offer margin trading on event contracts. ASML and Taiwan Semi headline next week’s tech reports.

Sentiment: Speculative excess continues building: record $1.42 trillion in margin debt, up 53.7% year over year, a $26.5 billion IPO pop, SpaceX entering the Nasdaq-100 months after the largest listing ever, and narrow mega-cap leadership while the average stock stalls. About 63% of S&P 500 stocks remain above their 50-day average, but the equal-weight index lagged the cap-weight by 150 basis points this week. Gold held near $4,113. Crypto sentiment continues improving with a green July, resilience through a broken ceasefire, ETF inflows returning, and bottom calls becoming more common. The market’s ability to ignore the ceasefire collapse is either strength or complacency, and record margin debt suggests investors have already picked a side.

Last week I said the second-half setup was mid-July CPI showing the energy unwind and bank earnings testing the rotation. Both arrive Tuesday morning, and the setup has sharpened into a genuine collision. The S&P 500 sits 0.6% from an all-time high, leaning on the narrowest leadership since May, funded by record margin debt, and betting CPI prints 3.5%. The bond market has sold off 8 of 9 sessions because the Cleveland Fed model says 4%, while oil just bounced 5% on a dead ceasefire. Both markets cannot be right, and Tuesday is the reconciliation. The banks report the same morning and show whether the consumer behind June’s 57,000 jobs is still spending or quietly cracking. Crypto also showed something new: it held its range through a war escalation, whales remain loaded near the lows, ETH is close to confirming its turn, and July remains green. If CPI comes in cool, the S&P breaks to new highs, the Fed regains its easing path, and the crypto bottom callers look early instead of wrong. If Cleveland’s 4% is right, yields push toward 4.75%, narrow leadership loses its cushion, and record margin debt unwinds the way it always does: fast. One number, Tuesday at 8:30 a.m. The whole summer is riding on the second decimal place.

English

$ETH

At ~$1,775, within a 52-week range of $1,388 to $4,954. Ethereum ground out another green week, up about 2.7%, spending the whole stretch in a tight $1,737 to $1,798 band and kissing $1,796 Friday morning, within a few dollars of the $1,800 gate that Polymarket gave 86% odds of hitting this month. The two-week bounce off the $1,547 capitulation low now stands near 15%, the best run since spring, and the structure is quietly improving: the 20-day EMA near $1,708 has flipped from resistance to support, and ETH is stringing together higher lows for the first time since April. The accumulation story keeps building. Tom Lee’s BitMine added another $74 million in ETH this week and is rapidly approaching its stated goal of owning 5% of the entire supply. A former Bank of America strategist publicly called a “tactical bottom” in Ethereum. And the narrative piece that has been missing all year is forming: analysts are now framing staking ETFs as the institutional story ETH never had, a yield-bearing wrapper that no other major crypto asset can offer. The map from here is unchanged: close above $1,800, then the 50-day EMA near $1,865, then the $2,000 fight. The Glamsterdam upgrade remains the fundamental catalyst on deck.

Fifteen percent off the lows, higher lows forming, BitMine buying toward 5% of supply, and Wall Street strategists calling the bottom out loud. ETH is one clean close above $1,800 from confirming the turn. It has knocked on that door three times this week. The fourth knock usually opens it.

English