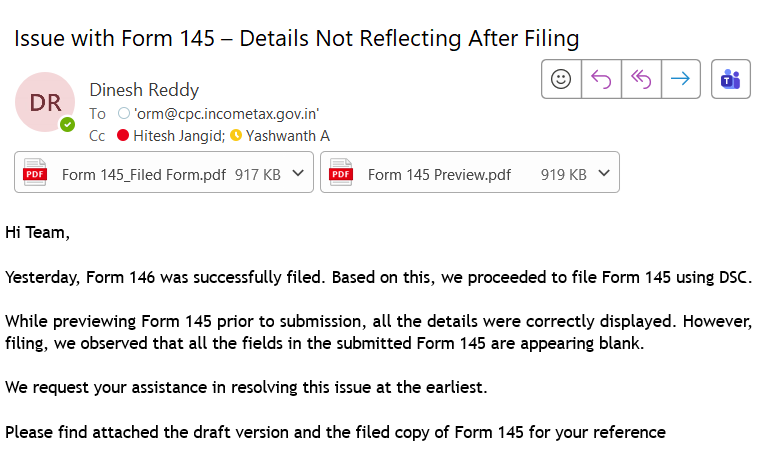

@IncomeTaxIndia On filing form 145 part C the details related to form 146 got disappeared and blank form got filed. In the preview downloaded the details were appearing correctly. Sent the email to orm@cpc.incometax.gov.in for this. Attached. Kindly resolve ASAP.

Except being member of ICAI,

You are neither a part of the ICAI Exam Department nor a council member,

So please stop behaving like that in every posts.

Chasing the refund for AY 2015-16 after opting for the Vivad Se Vishwas Scheme 2020.

The client has received Form V from the PCIT and thereafter determined a refund of ₹ 21 lakhs by AO. However when checking the refund details on the portal & verifying the bank account the actual credit received is only 34278.

Filed grievance + rectification request..

What should be done in this case? @IncomeTaxIndia

Dont tell me raise grievance or give me some mail id where i need to tell them the same thing again and again..

Refund mismatches after VSV still need consistent resolution hope the system improves..

@abhishekrajaram@IncomeTaxIndia The AO will take following documents

1. Request Letter mentioning the amount, date of payment, incorrect pan in which tax is paid and the correct pan to which the said challan persists.

2. Indemnity Bond

3. Bank Statement of relevant date as proof of payment of that Challan.

@abhishekrajaram@IncomeTaxIndia The assessee needs to approach his JAO in this case. The AO will first apply for identification of Challan No. which needs to be rectified as the assessee does not have the challan number and bsr code etc.

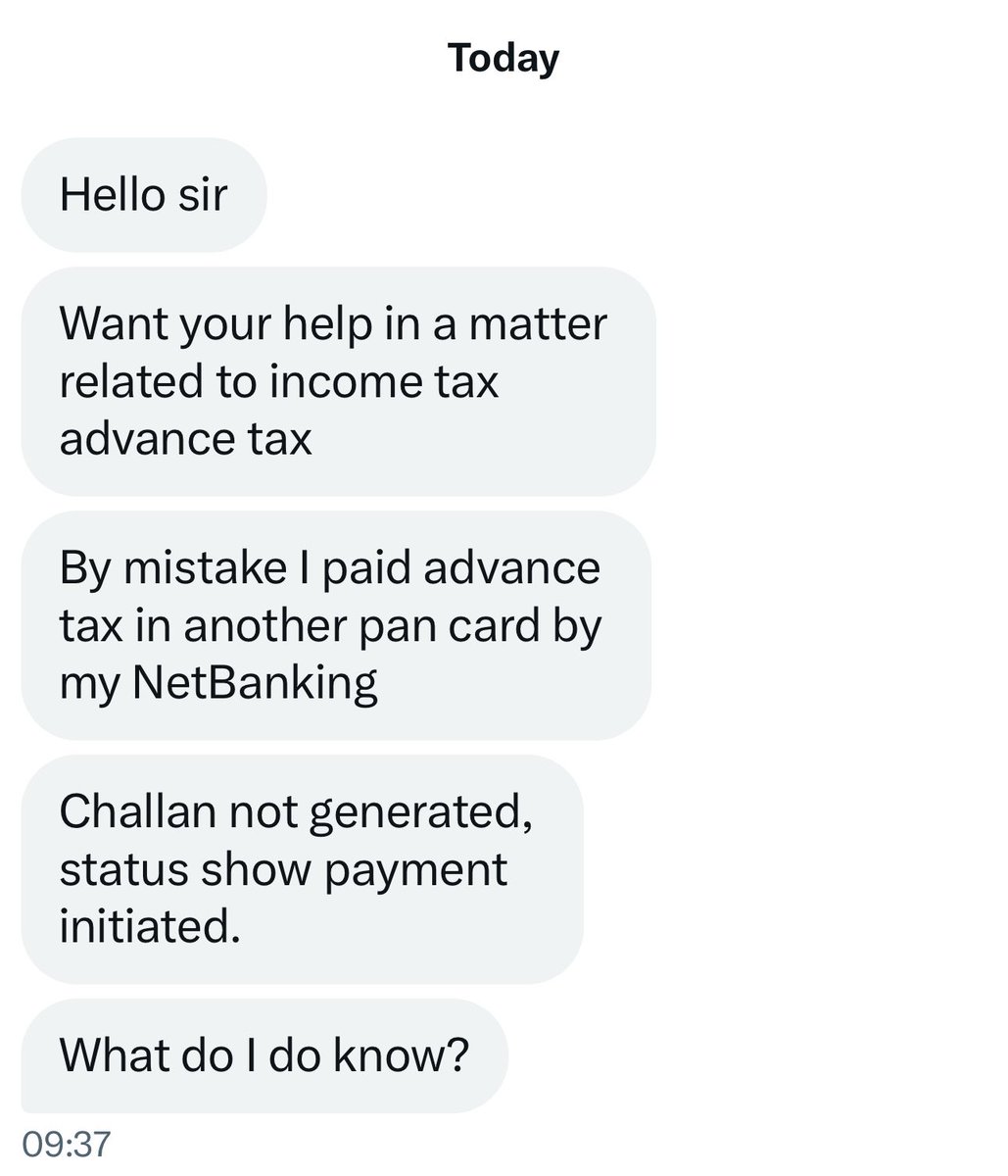

Friends,

I received this query from someone. Can you please help what could be the solution in this case. The amount is substantial and person can't make double payments.

Any suggestion would work.

@IncomeTaxIndia can you please suggest some solution to the person. And please don't reply with routine answer template that share your pan and other details. If you can suggest any solution then only please answer.

Thanks in advance to everyone

@shaifalyca If the individual is solely engaged in selling vegetables, then it is clear case of exemption from registration under Section 23(1)(a) of the CGST Act. Threshold Limits of 40 Lakhs or taxability of such sale of vegetable under GST is completely irrelevant in this case.

@umangjaiin@CAAditiBhardwaj Yes. In one of the Appellate Order as well, the JCIT (A) had recorded similar reasoning in the Appellate Order. Following this order, it appears that 87A rebate on STCG should be allowed for A.Y. 2025-26 (F.Y. 2024-25) as well.

@CAAditiBhardwaj Mam this exclusion come in Feb 2025 budget. So effectively this should implement in next year itr. For Fy 24-25 rebate should be allowed for ltcg & stcg. If I am wrong please correct me mam..🙏🙏

Rebate Debate

Last year, the rebate issue on STCG u/s 111A was hugely debated. The govt had to release a revised utility to allow this rebate.

This year however, effective AY 2025-26, Budget 2025 memorandum clearly states that rebate for STCG u/s 111A incomes won’t be allowed. It was always an intent to not allow it seems.

#incometax#ITRfiling

@Infosys_GSTN Sir, Please look into Grievance Number G-2023123111724570 on urgent basis. Table 8A figures of GSTR 9 OF FY 2022-23 are not updated correctly. Urgent resolution may please provided in view of the due date falling today and delay will lead to Late fee on daily basis.

@Infosys_GSTN Please look into Ticket Number: G-2023123011724274 on urgent basis. The GSTR 1 of november 2023 is not getting filled due to error "The system is checking for compliance of Form DRC01C." However, there is no Drc01C compliance pending in the matter.

No addition can be made on Unexplained Credit Amount in the Bank Account of Assessee: ITAT Delhi bench

Ajay Kumar Aggarwal vs The ACIT

CITATION: 2023 ITAT

Very interesting case

@Infosys_GSTN@Infosys_GSTN sir please look into the matter urgently as the figures of Taxes Paid in GSTR 9 under Table 9 are being shown only for 11 months i.e. from april 2021 to Feb 2022 and has not included for March 2022. Late fees is being levied unnecessarily with no fault of ours.