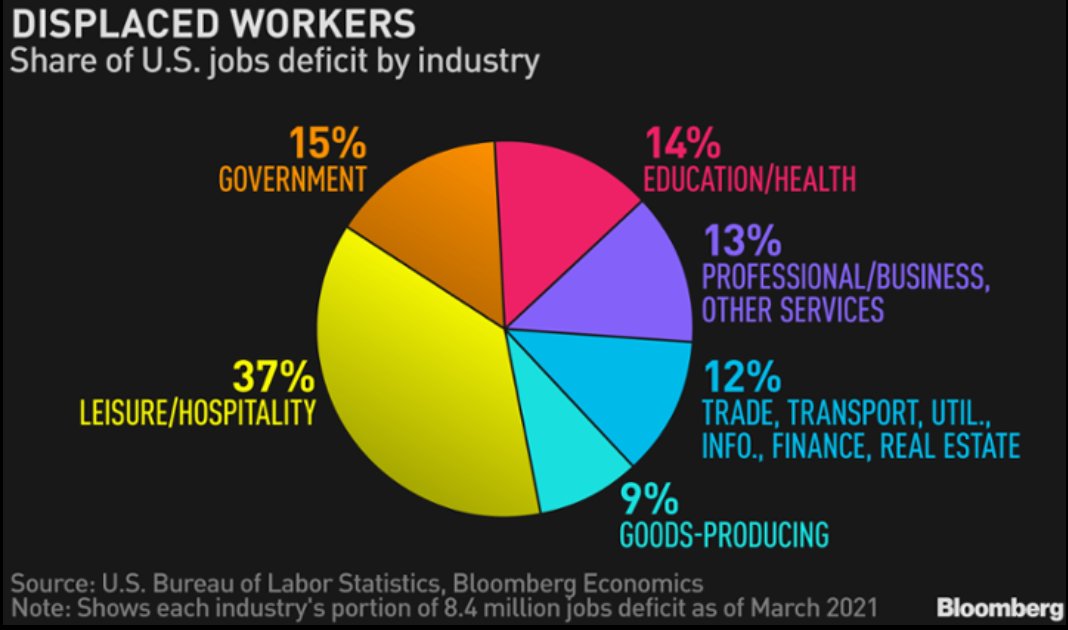

Today's payrolls figure is expected to be a blowout, but there's a lot of ground to make up. "The 'jobs deficit' relative to pre-pandemic levels remains roughly as wide as it was coming out of the recession of 2007-09:" @Riccanomix

“The divergent ‘K’ track will be broadly evident in the January jobs report, as sectors such as leisure, hospitality and restaurants/bars are due to witness ongoing, significant job losses”: Bloomberg Economics’ @Riccanomixbloomberg.com/news/articles/…

“Economic slack in general and labor slack in particular will stifle any sustained pickup in price pressures. This will yield the Fed an extremely long runway before officials will need to legitimately contemplate reducing accommodation”: @Riccanomix & @WingerEliza

Latest Macro Matters podcast talking the Economy - inflation, wages, growth with @Riccanomix... of course Angelo joins me for Fun Fed Facts were we talk TIPS and the Fed's influence on them... hope you'll have a listen. soundcloud.com/bloombergintel…

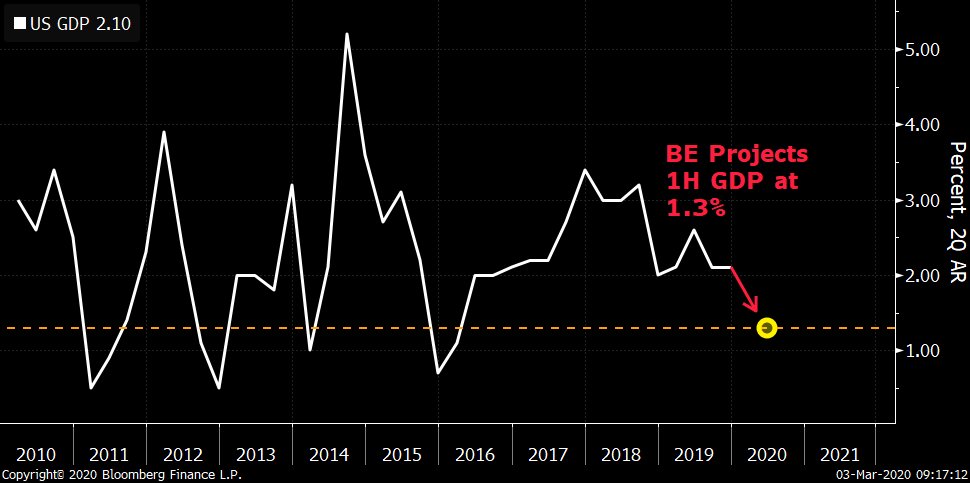

If US GDP growth slows to 1.3% in 1H, as we now project, this would be troubling, to be sure, but we've seen weaker soft patches earlier in this cycle...and managed to muddle through. Labor market is far stronger now than the prior episodes from 2011 to 2015.

While difficult to find an apt supply-shock parallel to Covid-19 (Sars, Fukushima, etc.), one need not look far for a parallel to the financial market shock--the equity correction of 4Q '18. As a result, Bloomberg Economics is downgrading 1H growth to 1.3% from 1.9%.

Watch for downside risk to motor vehicle sales today. Auto sales are among the more weather-sensitive economic indicators, and are likely to be impacted by extreme severe cold and snow at the start of January. Bloomberg Economics projects sales rate @ 17.0 million vs. 17.8m prior