Sabitlenmiş Tweet

RichardJK

11K posts

RichardJK

@RichardJKPE

Dad to two, husband to one, engineer to many, nerd to all.

Atlanta, GA Katılım Temmuz 2023

337 Takip Edilen423 Takipçiler

If someone paid you $700,000 to not have a single drop of alcohol for a year, would you do it?

English

@LostHistory9 Stop bitching and start playing chess. Take an interest in medical shows so you two can be closer. Then put on Scrubs. Now, everyone wins.

GIF

English

My lady is watching Grey's Anatomy.

It is the most boring, cringe shit I've ever seen. Genuinely don't know how people enjoy this. I have retired to another room because I genuinely cannot stand being in the same room with that show on the TV.

Why do women like this crap?

English

@FBGreatMoments Moss over Allen Page? Rice over Montana? Wilson over Lynch? These are certainly choices.

Ok, Rice/Montana is really hard.

English

@JamesSurowiecki It's also easy to find that the HOF has honored several people from Pre NFL. Jim Thorpe for example.

English

@JamesSurowiecki Just a few hours ago you're criticizing someone for screwing up oil/gas prices. Fine, but here you are screwing up "Pro Football" vs NFL. Glass houses.

English

Teddy Roosevelt died before the NFL was created.

Dan Diamond@ddiamond

Trump officials are pushing Teddy Roosevelt for the Pro Football Hall of Fame. "I think we’re going to see Theodore Roosevelt inducted," @SecretaryBurgum said this week, referencing a recent meeting with NFL's Roger Goodell. h/t @HowardMortman washingtonpost.com/politics/2026/…

English

@themoviedadsc Ok, but we got a Spaceballs teaser, Street Fighter trailer, and a Jack Ryan trailer this week. Not a word on them?

GIF

English

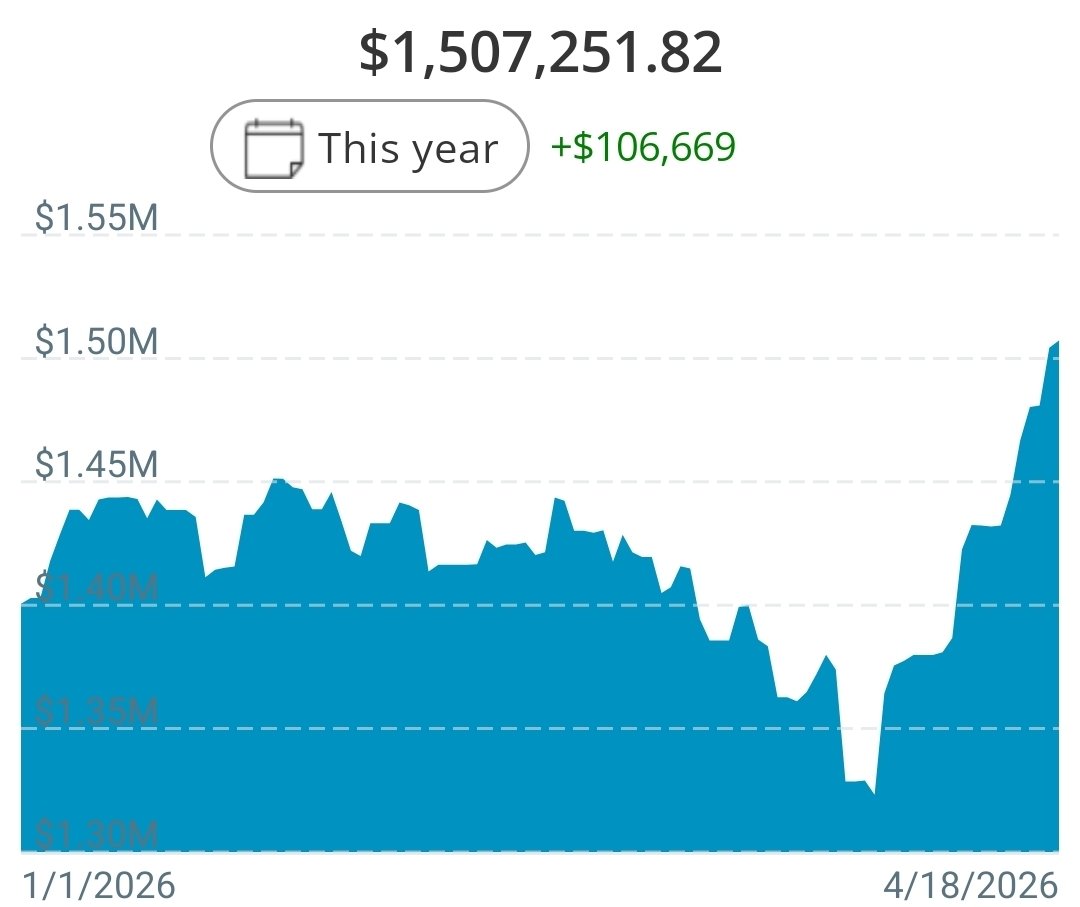

How we've made almost $200K in the stock market since the March 30th low?

Doing nothing and being patient.

Never sold any of our portfolio that we've spent 12 years building.

Just kept buying in our 401ks and taxable brokerage and just... waited.

Bark@barkmeta

Most of making money is just being patient and doing boring things consistently. Nobody wants to hear that because it doesn’t go viral. But it’s the truth.

English

@mellowrk_lion I feel triggered.

I was actually in this one too. Made a few coins. Green is green, but I got stopped out and missed the run to 30s. Same thing with another recent one. Reviewing these trades. Missing gains annoys me.

English

@mellowrk_lion Not doubting. Just impressed at the timing.

I was trimming most of my positions today when the decimal place moved on the big number in my account.

Unfortunately some government jackass called at 3:57 and made me miss close. I wanted to get some covered calls.

English

@dom_lucre @flapprdotnet

First Sweeney and now Fox? Sasquatch might be onto something.

English

🔥🚨STOLEN: Hollywood actress Megan Fox just appeared in a new Dr. Sasquatch commercial wearing a tight leather outfit. They really believe men are this easy.

English

@mellowrk_lion Good afternoon sensei. I've gotta be getting punked. Did you really sell this at the high point? Also guessing you've already sold puts.

GIF

English

@EastPointMadeMe I'm sure the parents in those counties would just love to go to APS, and watch their property taxes double.

(This is why we just moved to Cobb)

English

Terrible idea. Its like 10+ cities in each county.

Charlotte 💙 💫🚉💫@barely_th3re

if Atlanta locked the fuck in, we would consolidate Fulton, DeKalb, Clayton, Cobb, and Gwinnett under the City of Atlanta

English

SHMD - Sold 2/3 of my position at 6.80 taking a 20% win. Holding the rest.

RichardJK@RichardJKPE

SHMD - Got this back under 6 with a 1/4 size position.

English

Let's call this done.

Never imagined this blastoff on VTI, but to summarize:

1. 1.55 premium on the 325P

2. 3.60 premium on 325C

3. No gain/loss underlying.

1.5% win in 2 months. The divvy is 1% in 12 months.

Monday, we sell puts and go again.

RichardJK@RichardJKPE

VTI - Sold 325C April, 3.60 My actual idea didn't work out, but this is fine. Adding some cash and playing defense on the shares that got assigned at 325.

English

@themoviedadsc On Monday (hopefully), I'm going to sell a VTI put once I've got the cash available. I'll post a synopsis of the full idea.

English

@gen_axis_gen People get Edgar wrong. Tools dominate the first half so Edgar rules! Well, they stop being good later, but there's three things to make up for this: good spears, dragon boots, and dragon horn.

English

@from1to3000000 Absurd timing on this. I took a few 10C leaps yesterday to add to my commons position.

GIF

English

I added again small to $RKT here $15.66 on a large looks like over 10 million block trade clearing out a seller? My cost basis still in the $13s but I want to go for the jugular so keep pushing my line in.

Donkey building warchest@from1to3000000

I added to $RKT here on this move over $15.25 but only slightly as I do not want to hurt my cost bass. But, I needed more shares!

English

@FBGreatMoments Heinicke got off easy. Drinking light beer should be a fireable offense.

English

Still cant believe the NFL actually fined Taylor Heinicke for drinking a Busch Light after a win 🤦

English

@MomAngtrades This is honestly why I always say we need more voter suppression. These idiots all think the economy is about money rather than the availability of goods and services. Pay people not to produce anything, and the economy collapses.

English

Universal income is socialism. I’m laughing so hard at the people saying “hey, I will able to do hobbies and whatever I want” you do realize that’s the same things people who want socialism think will happen and it’s not even close to reality. Whether it’s Mamdani’s or Elon’s plan, the outcome is the same. Why don’t people get this?

English