Ronen Hayempour

1.5K posts

Ronen Hayempour

@RonenHayempour

Finance & Investing - Sharing My Opinions: NFA DYOR $NBIS $PGY $AMKR

Katılım Nisan 2022

73 Takip Edilen797 Takipçiler

@EndicottInvests Wanted to share Daniel’s post, brings light to this.

Daniel Koss@daniel_koss

Guys, how do I tell you this. $NBIS is probably NOT up 12% because of the acquisition they announced today. The most likely reason is the leak of Anthropic -> $44B ARR. Anthropic 1. Is a @ClickHouseDB customer (Nebius owns ~1/3). 2. Might become a Nebius customer. $CRWV is also up 7%. So today's price action is likely telling us market is learning that AI grows faster than expected. Some people realizing this means insane demand for Neoclouds. Anthropic is already a CoreWeave client. My read on the situation is that the market is pricing in the possibility of Nebius also soon signing a big Anthropic deal. Bottom line is however that even if Nebius does not get an Anthropic deal -> demand 🚀-> price/MW 🚀-> Neoclouds 🚀

English

Wow the market loves the acquisition more than I thought

$NBIS is really setting themselves up to become a hyperscaler and compete with the big dawgs

Still a long journey ahead but this is just another step in the right direction from the team

Earnings in 12 days.

English

$NBIS IS ACQUIRING EIGEN AI

• Combines Eigen AI's inference stack with Nebius's global capacity

• Jointly optimized endpoints achieved top rankings on Artificial Analysis across multiple models

• Eigen AI's founding team, including MIT HAN Lab researchers, will establish Nebius’s Bay Area engineering and research presence

Paid in a combination of cash and $NBIS Class A shares with aggregate value as of signing, based on Nebius’s 30-day weighted average stock price, of approximately $643 million, subject to adjustments.

Expected to close in the coming weeks.

BULLISH 🟢

English

$NBIS WILL RELEASE Q1 2026 EARNINGS ON MAY 13, 2026 BEFORE MARKET OPEN WITH THE CONFERENCE CALL THE SAME DAY AT 8:00AM ET

English

Data Centers are GREEEEEEEN

$NBIS up 9.5% 🟢

$CRWV up 8% 🟢

$CIFR up 2.5% 🟢

$IREN up 2.3% 🟢

$WULF up 2.2% 🟢

English

Exactly.

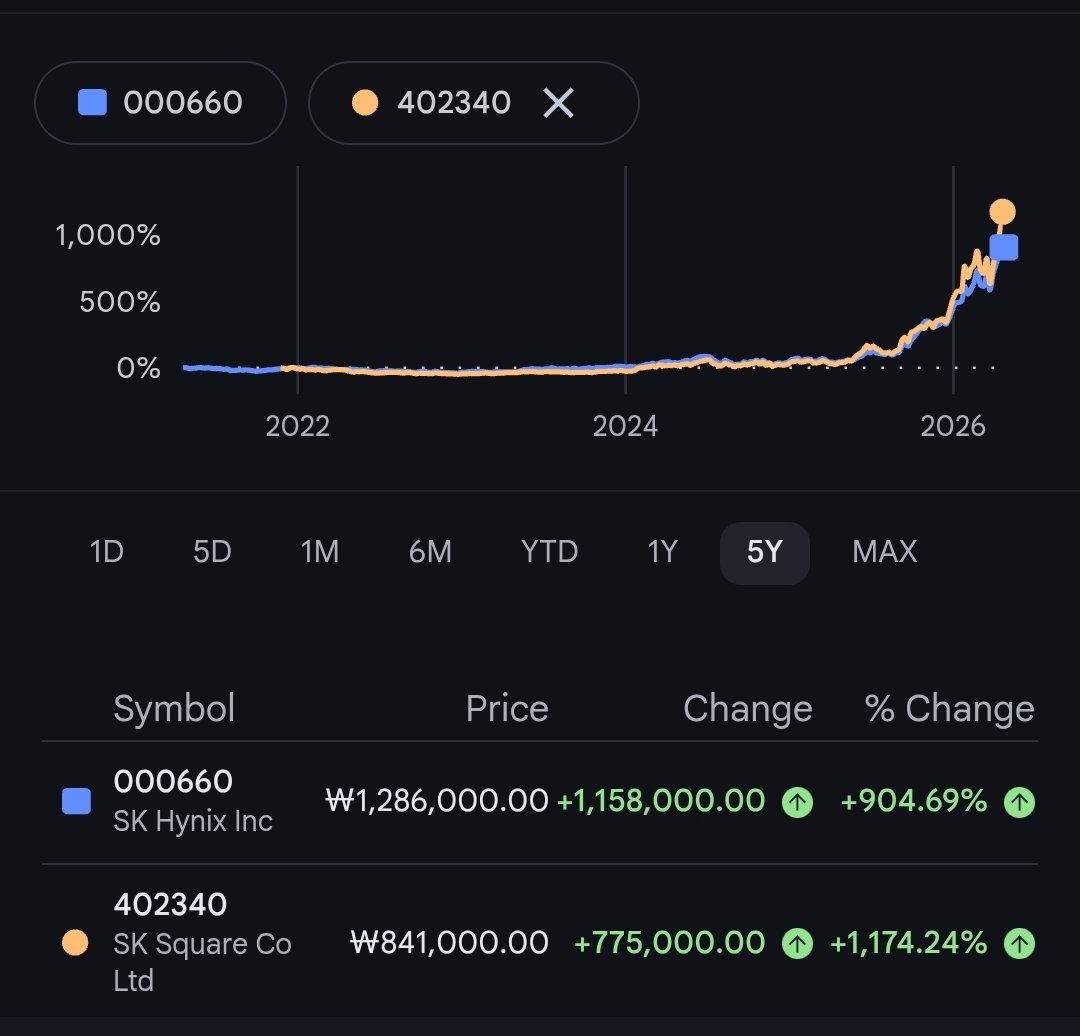

If you have an $IBKR account, take a look at SK Square($402340), it's a holding company that holds 20% of SK Hynix and is trading at 43% discount to NAV, you're basically getting SK Hynix for $350B

5Y Performance below 👇

Asymmetric Bets@UncleAlpha007

$000660 $402340 SK Square trades at 2x earnings and owns 20% of SK Hynix Available on Interactive Brokers now — much cheaper than $MU (SK Hynix has similar market cap to MU but 2x profit) … and they tell me I’m a “pump account”

English

FULL BREAKDOWN OF $AMKR Q1 2026 EARNINGS

This is a great read if you are interested in $AMKR, never heard of it, or are an investor. Let’s dive in! (Buckle up this is loooong)

First off, highlights:

• Record Q1 Revenue $1.68 billion, up 27% YoY

• Gross profit $239 million, operating income $100 million

• Net income $83 million, Diluted EPS $0.33

• EBITDA $285 million

• YoY growth across all end markets

Q2 2026 Guidance:

• Revenue of $1.75 billion - $1.85 billion

• Gross margin of 14.5% - 15.5%

• Net income of $105 million - $130 million, or $0.42 - $0.52 per diluted share

• FY2026 CapEx of ~$2.5 billion - $3.0 billion

Gross margin of 14.2%, down from 16.7% QoQ but up from Q1 2025 of 11.9%

Operating Income margin of 6.0%, down from Q4 2025 9.8% but up from Q1 2025 of 2.4%

Not worried. Q4 2025 they guided lower in expectation of this for Q1 2026. Also, the lowest end of the Q2 2026 guidance is 14.5%, an increase of .3% from this quarter (bearish outlook).

Total Debt / Total Cash ratio of 1.26x

Stock buyback of up to $300 million but also raising $1.15 billion through convertible senior notes due in 2031.

They are expanding greatly. The phase 1 construction of the Arizona facility is planned to be completed in 2027 and in Korea the new test building is on track for completion at the end of 2026.

Growth data you can read. Solid results imo. 👇

Communications:

- Q1 revenue up 42% YoY

- Strong demand across premium tier smartphones

Computing

- Q1 revenue up 19% YoY

- Record AI datacenter revenue

- Softness in PCs and laptops

Automotive and Industrial

- Q1 revenue up 28% YoY

- Record Advanced packaging revenue

- Mainstream demand improving

Consumer

- Q1 revenue up 4% YoY

- Broad-based improvement in demand across customers

EARNINGS CALL: MY FAVORITE PART 🥳

Gross Margin Expansion Outlook:

- Back to the gross margins, they expect them to improve into the mid to high teens in Q2, driven by stronger pricing, higher factory utilization, and a better product mix from growth in advanced packaging and data center compute demand.

Pricing Strategy and Customer Acceptance:

- For Japan specifically they began raising prices in Q1 and are now working with nearly all customers to gradually increase pricing throughout the year, with customers generally willing to accept higher prices to help offset rising material costs.

- This will help increase gross margins.

CPU Ramp and Near-Term Timing:

- There will be a ramp for commuting, specifically for the CPU device, which will start from Q1. The meaningful revenue from this will start to show in Q3, so I’m interested in what Q2 will bring.

- Overall sounds good, not particularly worried about one shaky quarter due to the cyclical nature of the industry.

Customer Concentration Improving:

- The revenue from the top 10 customers is now 68%, down from 72% in Q4 2025 and 71% in Q1 2026. This is good to see, with revenue increasing and dependence on the heavy hitters lessening, hopefully it continues gradually.

Cost of Sales Trends:

- The cost of sales have essentially stayed flat YoY with a 1.1% increase to 53.5%. However, it's down from 56.5% last Q.

- For Q2, I’d like to see that down again with the increase in gross margin.

Arizona Margin Impact (Short-Term):

- They are signaling that the Arizona facility will create a temporary 1 to 2 percentage point drag on operating margins in 2027 due to upfront costs like depreciation and ramp expenses, though the exact timing is still uncertain and depends on equipment delivery and customer qualification.

- Something to monitor but I’m not worried; it’s bound to happen and the benefits for the facility are immense long-term.

Cost Transition (OpEx to COGS):

- These costs will initially hit operating expenses, then shift into COGS sold once production begins, similar to prior ramps like Vietnam (which just broke break even!).

Arizona Revenue Ramp Timeline:

- Revenue from Arizona is expected to start modestly in 2028, scale meaningfully in 2029, and fully ramp by 2030, which should offset the early margin pressure over time.

- This plays out perfectly with my ~2030 thesis.

Arizona scale:

- The Arizona facility is expected to reach about a $1 billion revenue run rate over time, roughly 10% or more of $AMKR current revenue base, though revenue per square foot may be higher than typical capacity since it focuses on advanced packaging.

EMIB + COAS-L:

- They continue to work with Intel on EMIB-related outsourcing.

- For COAS-L they do have one CPU product that they are working on. This will be more relevant in 2027 since they are early in the development cycle and it’s going to take time.

- Due to the constraints in general in the supply chain and in the packaging space, customers are very motivated to try to move as quickly as they can to develop these new technologies and new supply chain options.

- This is beneficial and bullish for $AMKR so great to hear.

AI advanced packaging growth (3x YoY):

- AI-related advanced packaging revenue is still expected to triple year over year, with potential for more than that, but growth could be limited by external constraints like silicon and memory supply as well as how quickly they can ramp up new equipment.

End-market growth outlook:

- Compute remains the strongest segment at around 20% growth, driven by AI/data center demand despite weaker PCs; automotive and industrial are growing solidly due to ADAS and in-car computing; communications is now trending stronger than expected, improving from prior single-digit expectations to potentially low double-digit growth.

- However, the typical second-half seasonal boost may be less pronounced because the first half is already unusually strong.

PC demand quality:

- PC demand itself isn’t especially strong, but they are being supported by a shift toward higher-end devices and some customer supply chain reallocations.

CapEx timing (2026):

- Capital spending will be heavily back-half weighted, with about 30% in the first half and 70% in the second half, partly due to timing delays in payments and equipment deliveries.

Memory impact:

- High memory prices are creating some supply constraints, pushing out an estimated $50 million to $100 million of revenue per quarter, but demand overall remains strong.

Arizona margins + funding:

- The Arizona facility is expected to generate margins meaningfully above $AMKR corporate average once scaled, though details will come later.

- The $7 billion investment will be supported by government incentives (including CHIPS funding and tax credits worth about $2.8B), customer contributions, and Amkor’s own liquidity and potential debt.

Export controls + macro risks:

- The main risks being monitored are rising input costs driven by commodities and geopolitics (like oil and metals), along with ongoing US-China trade restrictions around AI, though $AMKR says these are now more normalized and manageable rather than a major disruption.

Overall takeaway:

- $AMKR is seeing strong demand, especially in AI and advanced packaging, with utilization rising and capacity expanding globally, while near-term constraints come from supply chain limits and heavy investment spending ahead of major growth from Arizona later on.

- I’m very bullish and continue to hold with my $30 entry. I am hoping to see a decent dip to (worst I see is $50) so I can scoop up a bunch of more shares!

That’s it! Hope you enjoyed. I would love to hear your thoughts in the comments or if you have anything else to add. Would love a like and follow, thank you.

English

@cmsinvests I’m holding cash and I feel great!

$MSFT still down more than 25% from ATH, and I see other opportunities opening up. Also you can sell CSPs with cash.

🫡🫡

English

people who are still holding cash right now

Watcher.Guru@WatcherGuru

JUST IN: S&P 500 reaches new all-time high of 7,200

English

$AAPL Q2 2026 EARNINGS SUMMARY

Financials 📈

• Total Revenue: $111.2B (⬆️ 17% YoY)

• Diluted EPS: $2.01 (⬆️ 22% YoY)

• Operating Cash Flow: Over $28 billion (New March record)

• Stock Buyback: Additional $100 billion authorized

• Dividend: Increased to $0.27/share

Highlights 📱

• iPhone: Achieved a March quarter record, driven by "extraordinary demand" for the iPhone 17 lineup

• Services: Reached a new all-time revenue high

• New Launches: The M4-powered iPad Air, the MacBook Neo, & the iPhone 17e

Tim Cook, CEO - "Today Apple is proud to report our best March quarter ever... with double-digit growth across every geographic segment."

Kevan Parekh, CFO - "Continued strong customer demand... helped us achieve a new all-time high for our installed base of active devices."

English

$AAPL Q2 FY26 EARNINGS:

EPS: $2.01 vs. $1.95 🟢

Revenue: $111.18 vs. $109.66 billion 🟢

iPhone revenue: $56.99 billion vs $57.21 billion est 🔴

Mac revenue: $8.4 billion vs. $8.02 billion 🟢

iPad revenue: $6.91 billion vs. $6.66 billion 🟢

Wearables, Home and Accessories revenue: $7.9 billion vs. $7.7 billion est 🟢

Services revenue: $30.98 billion vs. $30.39 billion est 🟢

Gross margin: 49.3% vs. 48.4% 🟢

English

@bullsofwealth Nice! Would love to connect, dropped you a follow.

English

I talk finance and spread good vibes.

I’ve had some great momentum over the past week going from 150 to 377 followers.

I’m on a 5.5H flight to Mexico City so let’s try to get to 500?

I’ll be replying and engaging with everyone for the next couple hours.

Can we do it?

English

@BULLtrapBear Unfortunately not 🤦♂️

Still doing research on it, since I’m looking for one stock to put a big chunk into. I do lots of dd

Early worm gets the bird 😆

English

$MSFT IS DOWN 5% 🔴

Might have to scoop up some shares at $400

English