Joe G.

2.3K posts

Joe G.

@SEC_digger

Mechanical Engineer. Data centers before they were hated. Creator of @BankviewUSA

Earth Katılım Haziran 2022

2.1K Takip Edilen4.1K Takipçiler

The most intellectually and personally insecure person on Twitter has once again blocked me after I embarrassed him in his replies.

x.com/avidseries/sta…

i/o@avidseries

IQ often predicts important life outcomes more robustly than other known variable. This isn't my opinion. It's the finding of 100s of studies published in peer-reviewed scientific journals. No major finding in psychological research can claim effect sizes as large as IQ. None are as endlessly replicable. Ignore the pseudoscientific projections of deep personal insecurity by people like Taleb, and stick to the science.

English

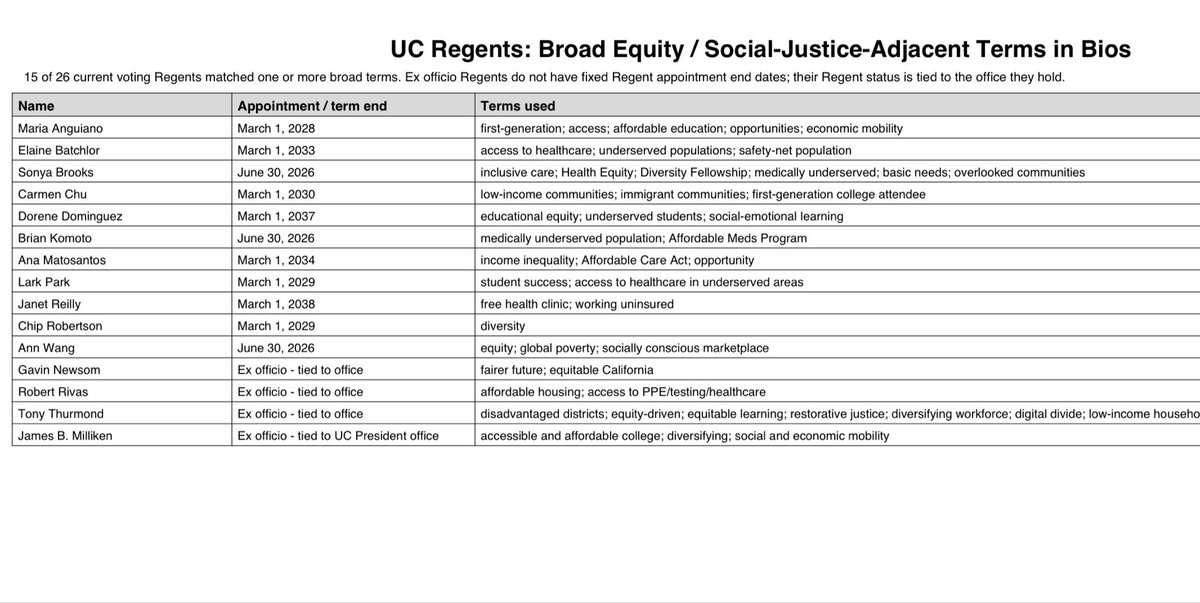

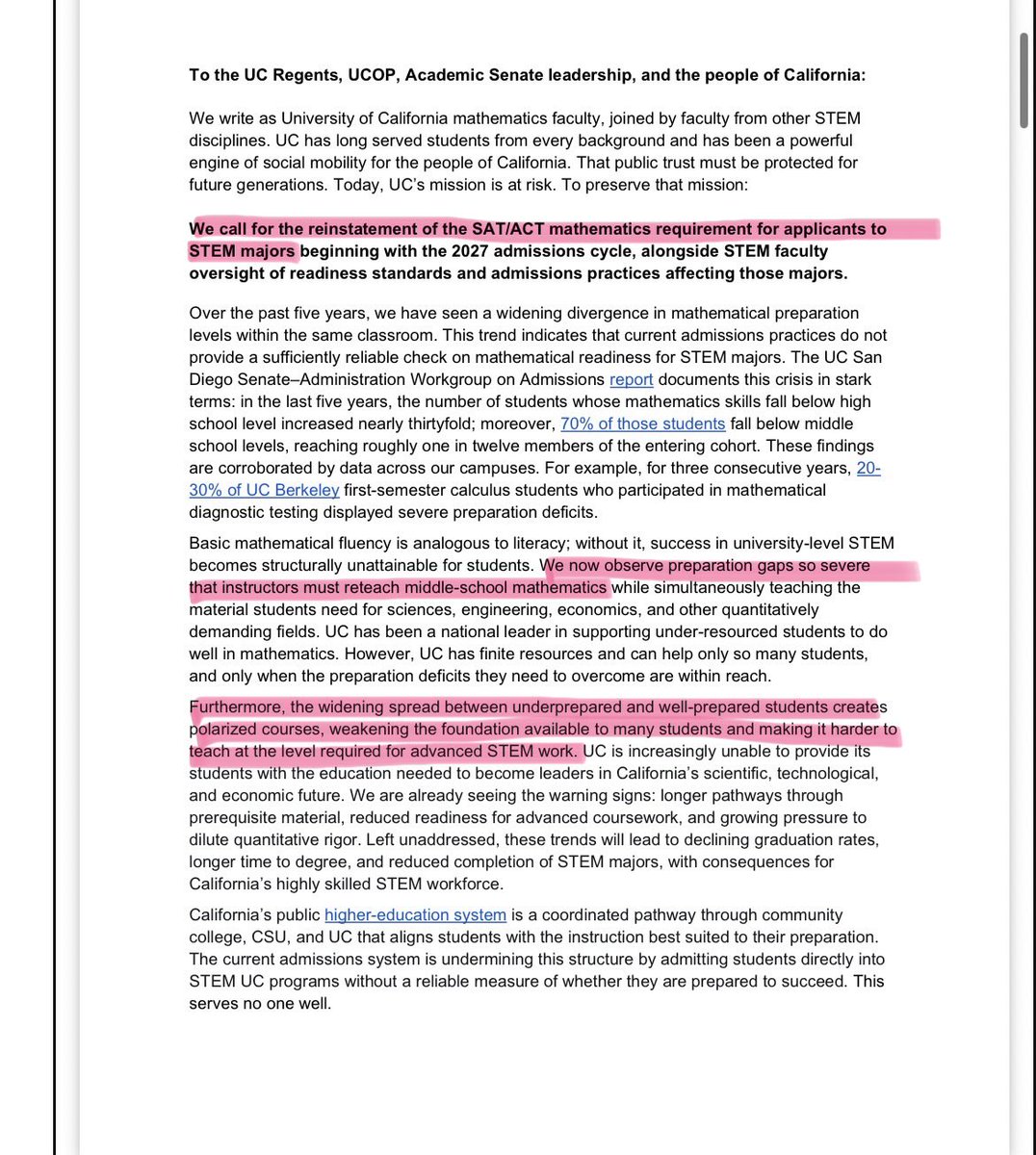

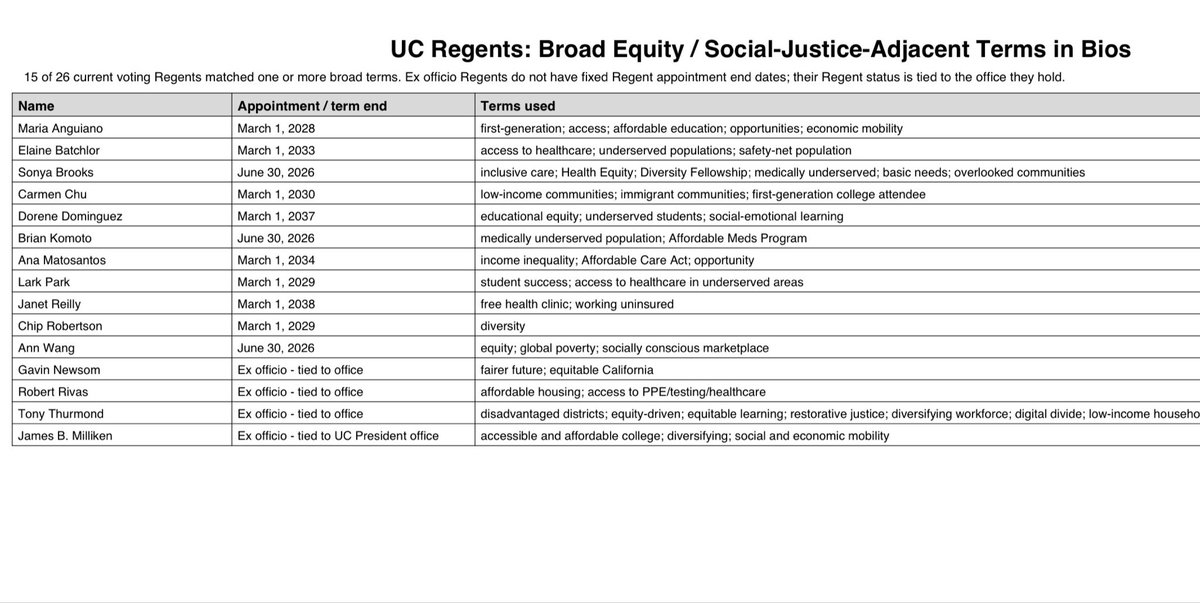

University of California STEM professors want standardized tests back due to severe math deficiencies among students:

“We now observe preparation gaps so severe that instructors must reteach middle school mathematics”

“The current admissions metric, based primarily on GPA & essays, can no longer reliably distinguish readiness for university-level STEM majors in an era of severe grade inflation & AI assisted application essays”

English

Where’s the next @nickshirleyy?

Would love to see some interviews w these people.

Joe G.@SEC_digger

This is exactly what the captured boards and sjw admins want. Feature not a bug. Stem departments need to grow some balls and take collective action to fail more students, even if it breaks policy. The board would be forced to choose between changing course or publicly firing entire stem depts.

English

@stoked_on_waves I got my ass handed to me in college and was almost one of those kids. Graduation meant more because I had to earn it.

English

@SEC_digger yeah, good for communications dept and similar if 70% of aspirant engineers et al flame out and need something else to study

English

This is exactly what the captured boards and sjw admins want. Feature not a bug.

Stem departments need to grow some balls and take collective action to fail more students, even if it breaks policy. The board would be forced to choose between changing course or publicly firing entire stem depts.

Neetu Arnold@neetu_arnold

University of California STEM professors want standardized tests back due to severe math deficiencies among students: “We now observe preparation gaps so severe that instructors must reteach middle school mathematics” “The current admissions metric, based primarily on GPA & essays, can no longer reliably distinguish readiness for university-level STEM majors in an era of severe grade inflation & AI assisted application essays”

English

@0dayCTF @TuckerCarlson Really great episode. Credit to you and @ShawnRyan762 for getting the word out.

English

@TuckerCarlson I appreciate the opportunity to speak about this on your show, and I hope a ton of parents open their eyes. Much love 🙏🚀

English

What percentage of suicides are inspired by satanic death cults online? Ryan Montgomery tracks crime on the internet and says it’s more common than we know.

0:00 Ryan Shows How Easy It Is to Find a Stranger’s Information

9:19 The Scary Reality of Facial Recognition

23:12 How Threatening Is It if Someone Has Your SSN?

25:47 How Roblox Is a Playground for Predators

33:07 The Satanic Cult Blackmailing Children Into Self-Harm

43:02 Ryan Shows Tucker One of the Groups Doing This

52:29 The Lack of Effort From Roblox to Stop Predators

56:44 Ryan Montgomery’s Story and Why He Does This

1:10:02 Project Veritas’s Failed Involvement

1:12:11 Who These Groups Are and Why They Do It

1:16:26 Is There Any Effort From the FBI to Stop This?

1:21:44 Ryan’s Hacking Gadgets

1:47:47 The Surrender of Human Autonomy to the Machine

English

@MrAndyNgo @AndyKimNJ @elaadeliahu Lived and went to school in Newark in the 00s. Was always a shit hole city, but they were building at the time so it felt hopeful. Went back last year and it felt worse than I remember. Super depressing.

English

Newark, N.J. (May 25) — Democrat NJ Senator @AndyKimNJ gets his face and eyes washed at the anti-government far-left riot outside the Delaney Hall Detention Center. The militants tried to stop @elaadeliahu from recording.

English

@SMB_Attorney He was basically saying the economy is still cyclical and no one can predict the future.

English

I’m a lawyer. I’m the first to suggest caution and point out the risks.

But listen guys, if you’re sitting waiting for a recession, scoffing at others and thinking you’re the smarter than them, you’re a loser.

Make a plan, then let it fucking rip. We’ll be dead soon anyways.

Andrew Lokenauth@FluentInFinance

“A crash is coming.” Andrew Ross Sorkin says a massive crash is inevitable. He’s one of the most credible financial journalists in the world.

English

Good primer on the defense market.

Any disagreements w Peter @PalmerLuckey?

youtu.be/VElWGgso2FY?si…

YouTube

English

Thanks. My wife deserves the credit. She did most of the heavy lifting for about 1-2 hours a day. No daycare. Our daughter is probably average-ish IQ, so we credit her performance to the approach.

When I hear curriculum designers talk about social justice or push a debunked approach like three-queing, it’s a massive red flag to me. If your mission is to make racial groups perform equally, you can bring under-performers up to speed, but you can also slow down over-performers. I don’t want these idiots anywhere near my kid.

English

@SEC_digger @NielsHoven Amazing, kudos to you and your wife! How much time do you spend reading to her? Is she going to daycare?

English

@NielsHoven is right.

If we want American kids to be literate, find out what the teachers’ unions are claiming and do the opposite.

We started our girl on phonics at 2yo as she was learning to talk. If kids can learn to speak two languages at that age, why not one language + reading? She’s 3-1/2 now.

John Stossel@JohnStossel

Teaching reading "became this holy war!" says reading app designer @NielsHoven. One reason is that George W. Bush pushed phonics. Teachers said "if George Bush is telling us what to do, we aren't going to do it." Seriously.

English

Since David blocked me but has implied that concerns about accredited investor verification are just “fear-mongering,” it is worth stating: there are real securities law consequences to knowingly admitting non-accredited investors into a private fund where the exemption requires accredited investors.

Among other things:

• It can undermine the issuer’s exemption reliance entirely — potentially transforming the offering into an unregistered public offering under the Securities Act.

• If the federal exemption fails, state blue sky violations often follow as well.

• Rescission rights may extend to all investors in the offering — not merely the improperly admitted investor.

• It likely creates disclosure/compliance issues under Rule 502 of Regulation D, particularly if non-accredited investors were admitted without satisfying the applicable information requirements.

• It raises obvious diligence and governance concerns for institutional allocators and sophisticated counterparties reviewing the manager’s compliance infrastructure.

These are not theoretical issues. They are core aspects of private offering compliance.

Max Schatzow@AdviserCounsel

If you mess up an investor qualification issue that could frustrate your reliance on an exemption under the ‘33 Act, ‘40 Act, or Advisers Act, don’t tweet about it. This is legal advice.

English

It’s a sticky issue. At the Federal level, the U.S. Constitution establishes a system of religious pluralism. The First Amendment ensures the "free exercise" of religion while simultaneously prohibiting the government from creating an "establishment" of religion. This creates a framework where all faiths are protected, but none are officially elevated by the state (establishment clause, no religious test clause).

At the state level early America featured state-sponsored churches (such as in Massachusetts until 1833 and Utah in territorial period and de facto well into 20th century). Many states outlawed certain religions formally (e.g. Catholicism).

The Founding Fathers generally viewed foreign religious states, theocracies, and nations with established state churches with deep skepticism, viewing them as cautionary tales of corruption, tyranny, and endless civil warfare. Israel is a semi-confessional state and it probably would have raised the eyebrows of the founding fathers as children of the Enlightenment, yes. However, when dealing with foreign governments, they interacted with them based on national interest, commerce, and international law, rather than trying to change their religious governance models. The clearest example of this separation between domestic principles and foreign diplomacy is the 1797 Treaty of Tripoli, initiated by George Washington, signed by John Adams, and ratified unanimously by the Senate. Article 11 famously demonstrates that while the U.S. rejected the idea of a religious state for itself, it expected to maintain peaceful, equal diplomatic relations with foreign nations that were explicitly religious states.

English

I can't stay silent anymore. I can't hint around the edges. The antisemitism has to end.

I was raised Christian. I also carry some Ashkenazi blood. So this is personal on more than one level.

I'll own my worst take of the last decade: I said @bariweiss's book "How to Fight Antisemitism" was unnecessary. I was wrong. Embarrassingly wrong. The receipts are everywhere now.

Dave Smith and Darryl Cooper are grifters. They found a market opportunity in Jew-hatred and they are cashing in on it. That's the whole game.

October 7th was not a genocide.

Calling it one is an insult to the Rwandans, the Armenians, the Cambodians, the Bosnians, the Yazidis, and the Uyghurs. Words mean things. Use them correctly.

The history is not complicated. Bill Clinton put a two-state solution on a silver platter. Arafat said no. The Hamas charter calls for the death of every Jew on earth.

That is not a negotiating position. That is eliminationism.

To my Western Muslim brothers and sisters, including some of the best business partners I've ever had: I know this isn't you. I'm not talking to you. I'm talking about the people who hide behind faith to push something you'd never endorse.

Sharia law is not coming to the greatest country on earth. Not on my watch.

I stand with Israel.

עם ישראל חי

Bill@Bill1719573

@paulswaney3 Paul, Boomers made a lot of mistakes but their 3 biggest are: 1) Not supporting David Duke when they had a chance 2) Believing the lies on the electronic jew about diversity 3) Believing the anti-"Nazi", holocaust lie. These mistakes have been profoundly bad for our nation.

English

America’s history is one of anti-religious or caste tribalism. Freedom (and even extra protections) to practice, but no special treatment for any one group.

This philosophy is completely incompatible w a religions state, Jewish or Muslim. The entire idea is anti-American and the opposite of what our founders fought for.

English

Data centers

Joe Lonsdale@JTLonsdale

Just personally with @8VC, here is a sample of what we are doing using these: * research against various diseases including solid tumor cancer that’s already leading to new cures in promising trials; * healthcare AI that’s already cutting billions in costs and accelerating, we can and will take out trillions in costs but it’ll be a worthy battle against the cartels; * accelerating aerospace design and iteration for the top engineers by 100X and making flight over 12X more affordable while also safer and quieter, already launching prototypes and a lot more coming soon; * bringing back manufacturing to the US with AI enabled companies that are hiring thousands of people to build ships, and many other areas; * making shipping costs far lower with major advances in logistics, and helping each top broker at various companies be far more effective and earn more, just making this area cost less for all; * helping us partner to buy new small businesses and pay more for them to previous owners in ways we wouldn’t have bandwidth to do before, thanks to AI agent research and diligence augmenting our team in this area, with a goal of creating tens of thousands of new small business owners. And helping them each thrive and do more, AI is key for small business operators. That’s off the top of my head. I hate big tech idiot politics and chicanery too. You’re right their foundations are terrible. I’ve also called them out hard. It pisses me off, too. What do you want me to do? These above are all great things and I’m doing my best. Should I stop all of this / should we honestly turn off the data centers powering my work, or make them not available to scale it?

Italiano

@utekkare @JTLonsdale Start by not calling it “electricity equipment”

English

@JTLonsdale Joe can we help with electricity equipment ? Non China. 3-6 month delivery and install. UL in process.

Pranay Srinivasan@utekkare

I'm wondering who builds data centers out there and is stuck waiting for UL certified pad mounted power transformers... I think we can help them.

English

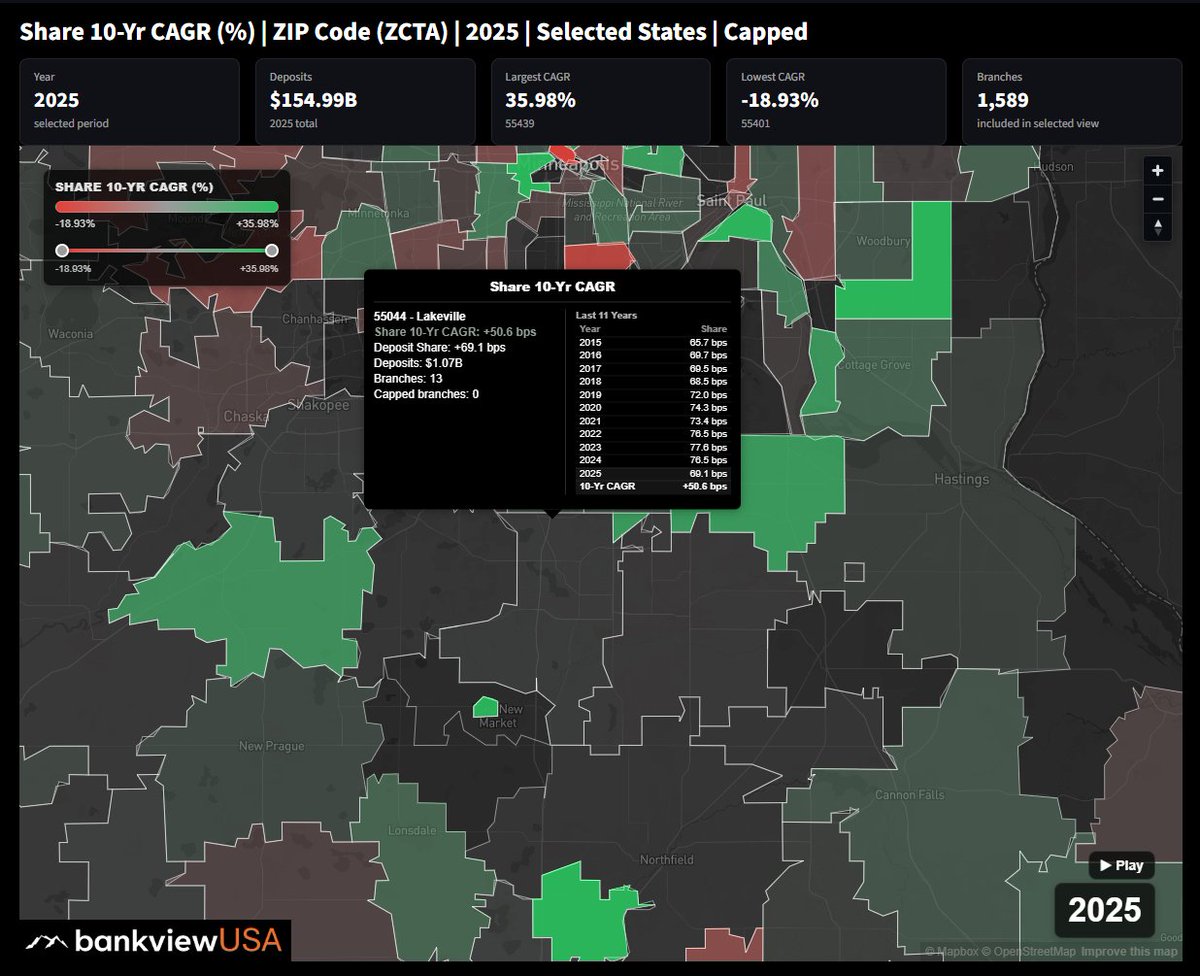

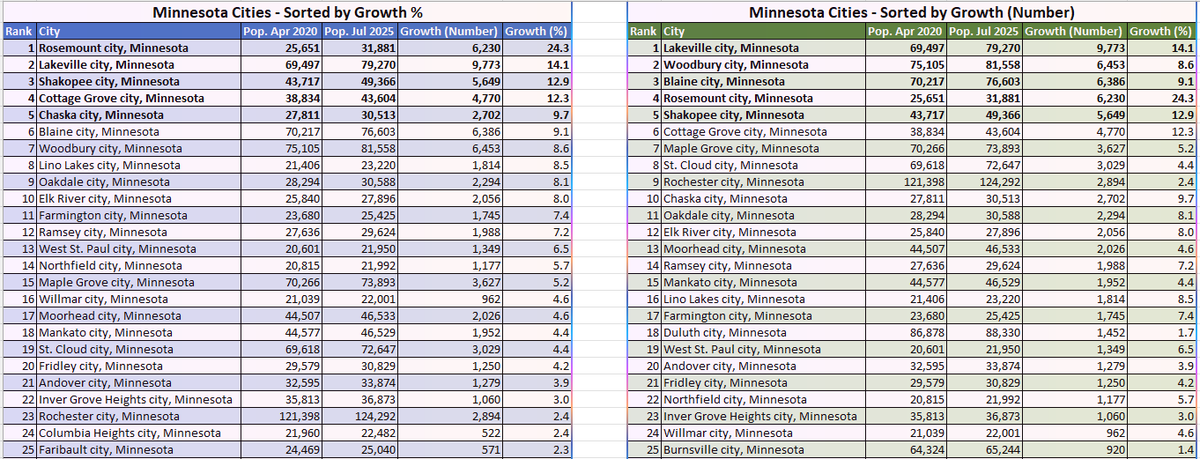

Here's the data by Minnesota. A lot of growth in South Metro.

% Growth

1. Rosemount

2. Lakeville

3. Shakopee

4. Cottage Grove

5. Chaska

# Growth

1. Lakeville

2. Woodbury

3. Blaine

4. Rosemount

5. Shakopee

Luke Hellier@lukehellier

Latest census data. Lakeville 2nd fastest growing city in Minnesota 8th in the Midwest 150th nationally 14% increase in population from 2020 to 2025. Total population 79,270. www2.census.gov/programs-surve…

English

Companies used to keep their own local DCs in their offices before everything moved to the cloud. (The elimination of capex was part of the pitch.) The power infrastructure in a centralized DC is way more robust than what you'd find in an office, and there's typically backup gens and a power substation next to the property of a hyperscaler. You also need the same HVAC capacity to get rid of the heat, so a wider geometry works better.

English

@upInYerCommentz another question: why aren't they putting more data centers in old office buildings (instead of annoying boomers in suburbs)?

English

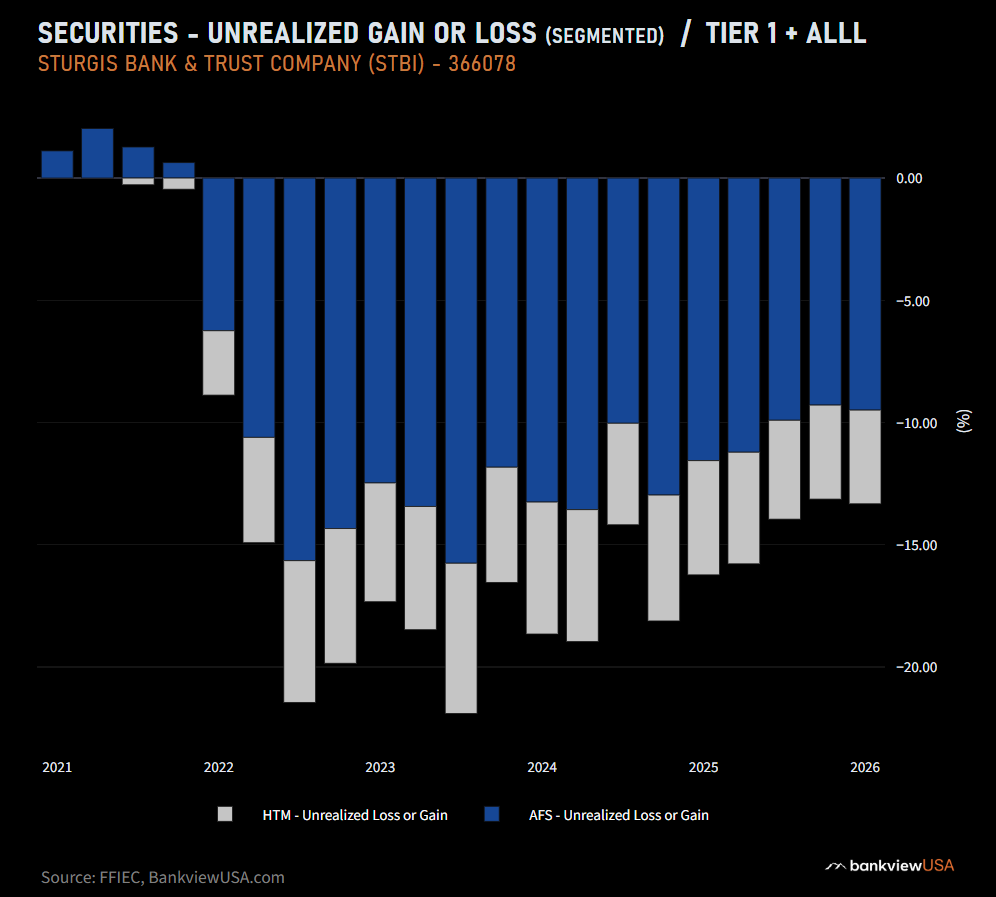

Know what you're buying first. BankviewUSA.com

$STBI

Dirt Cheap Banks@dirtcheapbanks

A new article on this beautiful Sunday afternoon for you all to enjoy. A very cheap bank that looks like the perfect M&A target.

English