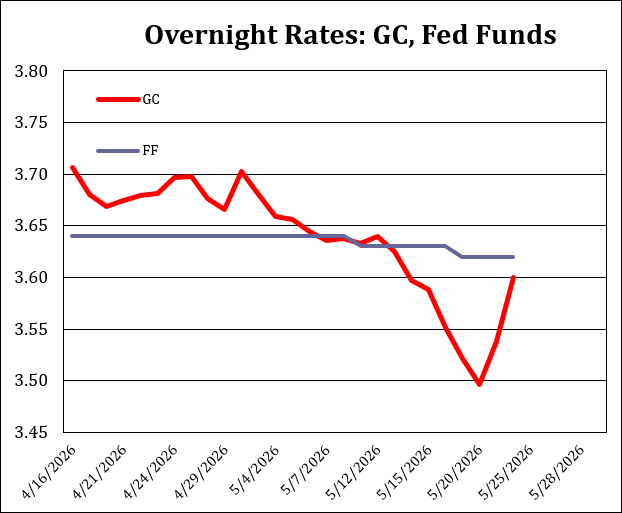

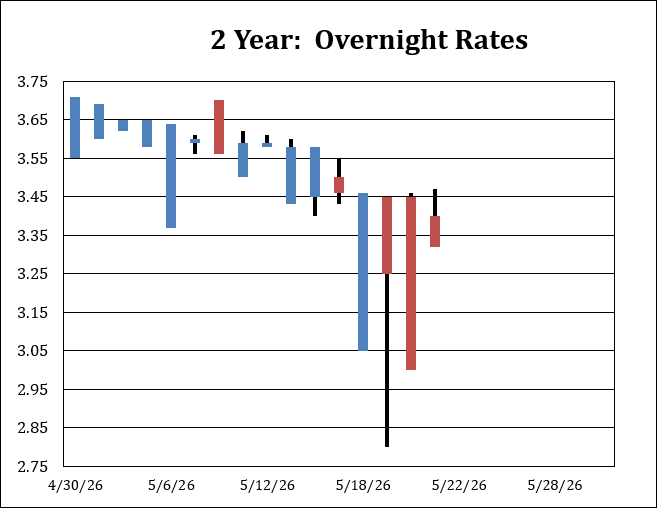

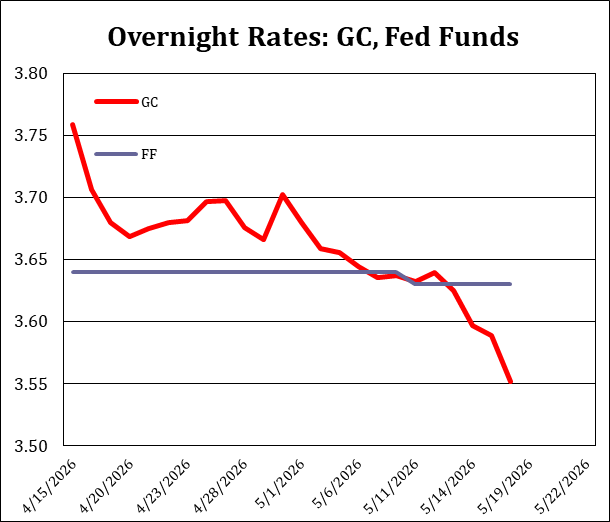

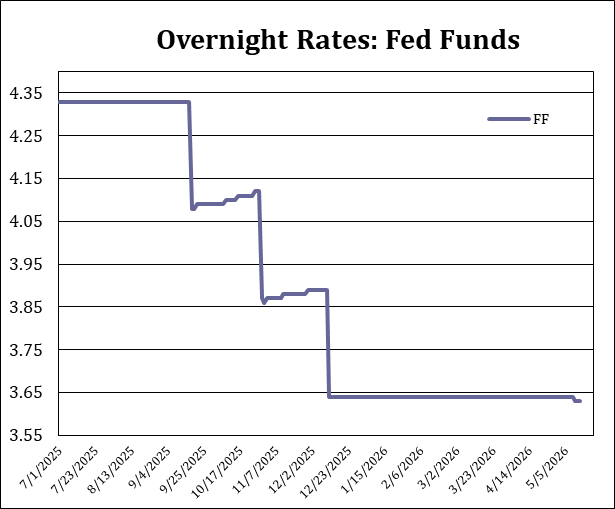

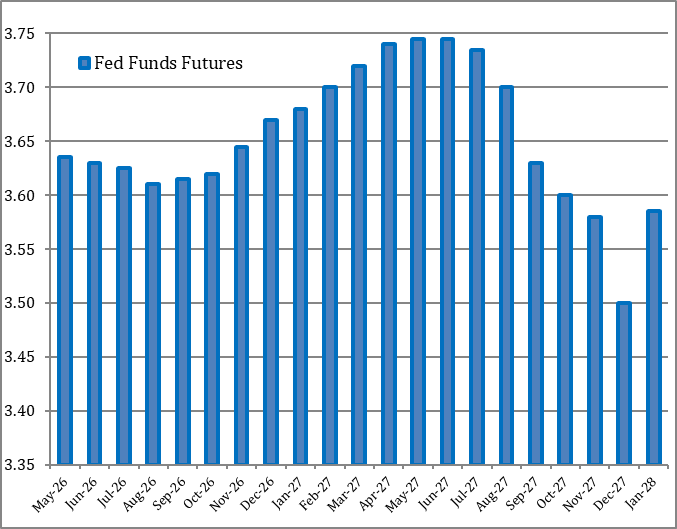

The market removed all of the chances of easing, except for a small remnant in June. The market prices a 3% chance of an ease on June 17, a 12% chance of a tightening by July 29, a 35% chance of a tightening by September 16, and a 45% chance by October 28

English