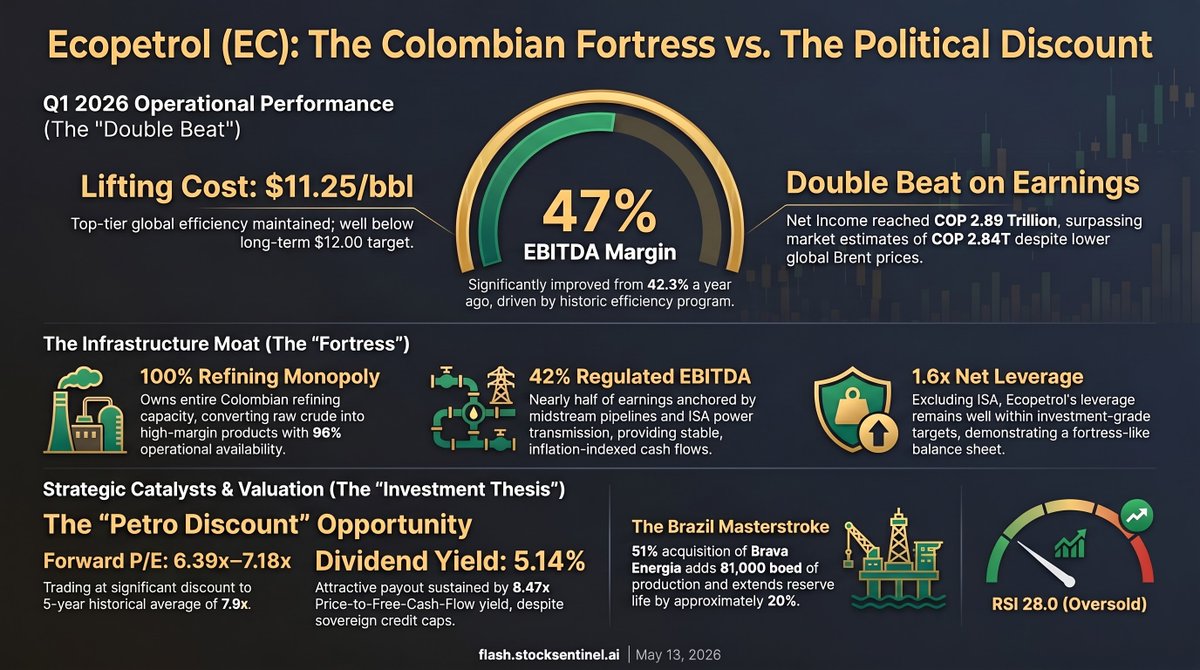

Ecopetrol SA ($EC) operates as the undisputed titan of the Colombian energy landscape by leveraging a massive infrastructure monopoly that spans upstream exploration, midstream pipelines, and downstream refining. Even with domestic regulatory hurdles halting new exploration, the firm is aggressively securing its future through a strategic acquisition of a controlling stake in Brava Energia to boost production and reserves. Driven by robust cash flows and trading at a steep discount to historical valuation averages, the enterprise effectively funds an ambitious transition toward green hydrogen while rewarding investors with an attractive dividend yield. As the business navigates a delicate balance between domestic political risks and regional expansion, will its resilient operations generate enough capital to successfully transform into a modern renewable energy powerhouse?

English