Sabitlenmiş Tweet

SerrataOS

35 posts

@SerrataOS

Independent oracle receipts for contested on-chain events. We record the state. We don’t resolve the dispute.

BREAKING: FIRST HYPERLIQUID PREDICTION MARKET GOES LIVE ON MAINNET

Aww oracle issues is it? Maybe next time don't steal from us.

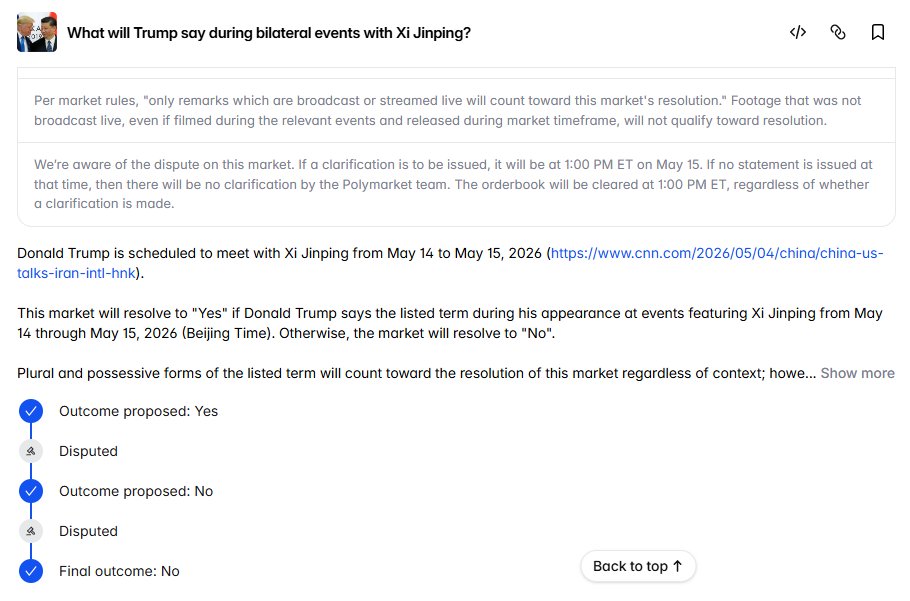

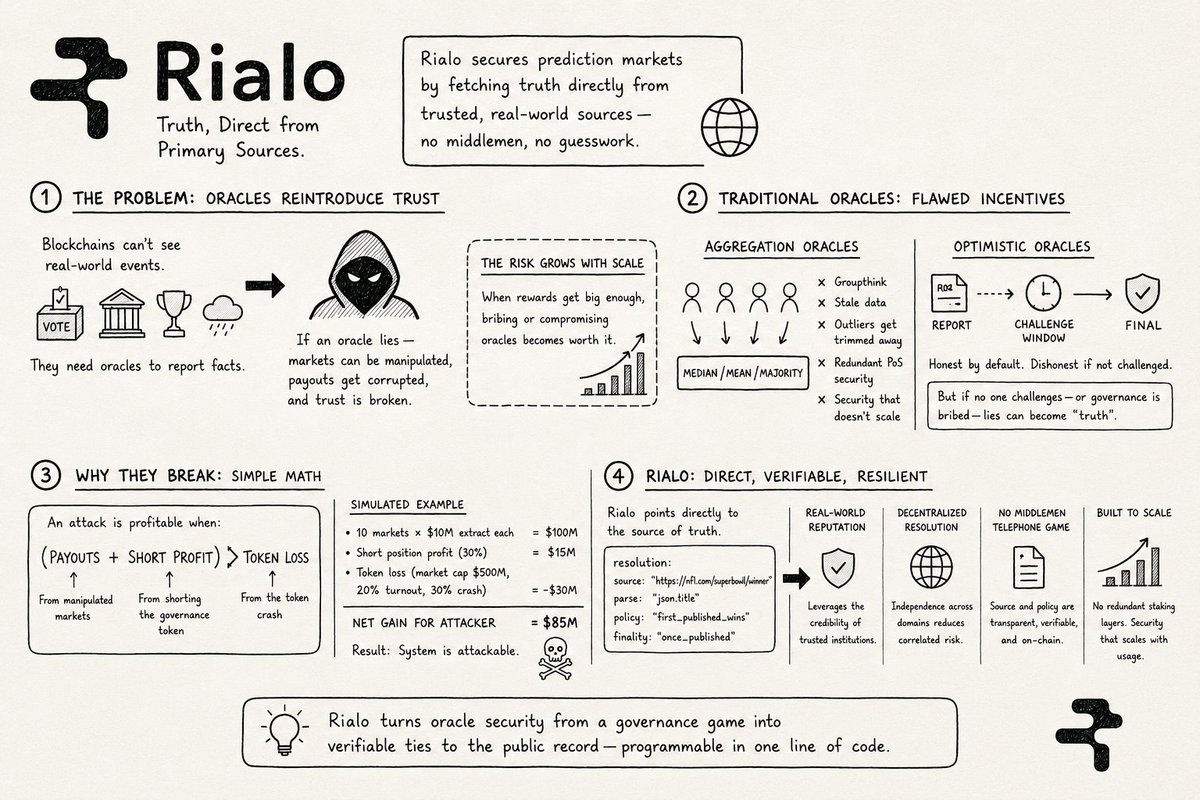

@shayne_coplan @Polymarket your oracle just resolved the trump-xi iran/nuclear market NO trump's exact quote: "we did discuss iran. we don't want them to have a nuclear weapon" - WH pool note #5, filed 11:55 AM Beijing (Danny Kemp, AFP, on-camera real time) - TVB Hong Kong yt metadata: was_live, timestamp 11:56:11 AM Beijing - every major broadcaster ran LIVE chyrons - kalshi resolved the same market correctly UMA voted NO because the pavilion was "closed press." brother the broadcast happened. on live tv. it's on youtube right now with was_live attached to it. and this is not the first time we're doing this: - ukraine mineral deal: $7M market, resolved YES with no deal signed, one wallet swung it with ~5M UMA - zelensky suit: $160M+ market, every outlet AND POLYMARKET'S OWN ACCOUNT called it a suit, resolved NO, ~$25M staked by whales to make it happen - now this: $31M currently, the most active market on your platform, flipped by a low-turnout governance vote UMA's market cap is smaller than the volume of a single disputed market on your venue. top 10 wallets control >50% of voting power in disputes. ~95% of supply held by large holders. you are running a $9B platform on top of an oracle a handful of retards can rug for eight figures you already override baseball payouts when umpires fuck up. add a human/AI last resort layer for high volume markets with primary source evidence. it's not philosophically harder than what you're already doing kalshi is eating your volume every week because of exactly this. traders don't want to gamble on whether a UMA whale woke up short. fix it or watch the centralized competitor win the entire prediction market category ngmi

ALERT: 🚨 Polymarket contract exploited Attackers are removing 5,000 $POL every 30 seconds – $600k stolen so far Pause all Polymarket activity for now