Quants hate candlestick patterns.

So I tested 5 popular "Buy the Dip" setups on SPY (2000-2026) to see if they work. The truth? 4 of them lose to the benchmark. But one weekly timeframe shift generated $551k net profit.

Full data + copy-paste RealTest code below 👇

It is tempting to add filters until a backtest has no losing years.

In reality, that just fits the code to yesterday's noise.

The systems that survive live trading are usually the simplest ones.

We look for a basic edge with a logical reason to exist.

Discretionary trading requires human emotion parsing charts in real-time.

Human emotion is a high-latency, low-fidelity processor.

It is a bottleneck.

Delete human from the execution loop.

Code rules in RealTest.

Automate the execution.

Your edge is statistical expectancy.

There is a specific kind of 'click' when you move from manual guessing to systematic testing.

It’s like finally seeing the matrix.

Once you start seeing the markets through the lens of a backtest, the old way of trading just doesn't make sense anymore.

The best part of the systematic world is that the data doesn't care about our opinions.

It’s a humbling process of constant refinement.

We’re all just trying to build systems that are a little more robust today than they were yesterday.

A whole trading rule can fit in one line a beginner can “read out loud”.

Buy = Close > Highest(Close, 200)

Own it when it climbs above everywhere it has been all year.

Writing the rule was never the hard part.

Trusting it enough to follow was.

Systematic trading can feel like a lonely grind, but there’s a real beauty in the process of building something robust together.

We’re all just trying to trade a little smarter than we did yesterday.

What’s one small win you’ve had with your setups this week?

Two people buy the same stock on the same morning.

1. One read about it in a group chat an hour ago.

2. One ran the rule on twenty years of data and already knows when he will sell.

They look identical today.

A hard year will show they were never the same trader.

The long-awaited article is finally here.

> Part 3 of the regime filter series.

> 12 "smart money" signals tested, plus the final leaderboard of all 45 filters from the whole series.

If you use any rule to decide when to be in the market, it's in here.

A trader watched his strategy take a loss he had seen coming and did nothing to stop it.

Tempting to override it, he thought, and let it ride anyway.

The loss was already in the plan, and the plan had been tested, so he stayed whole.

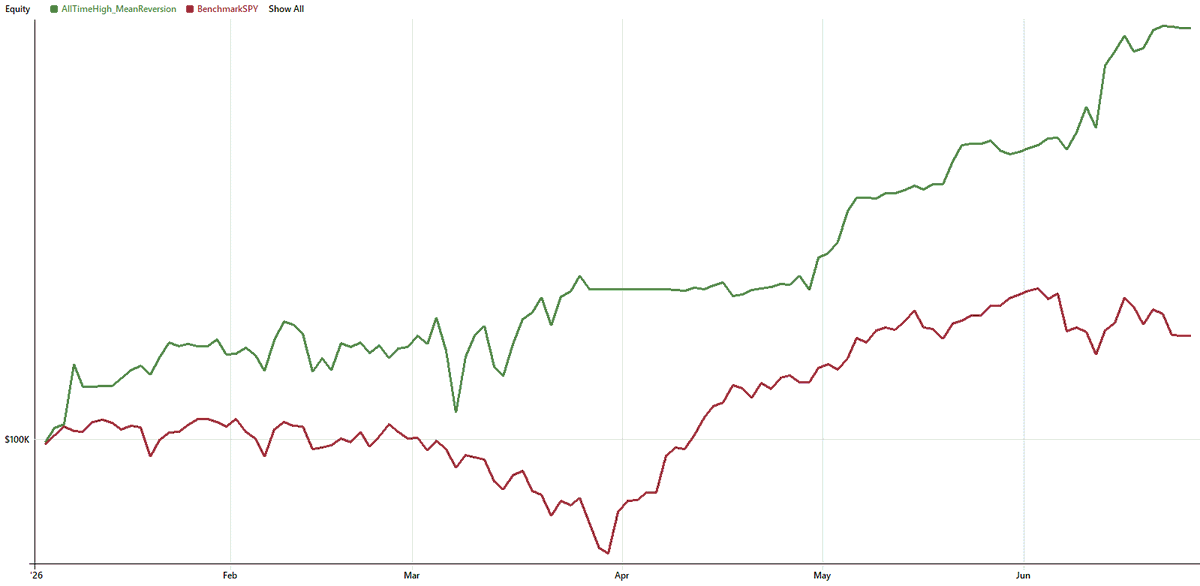

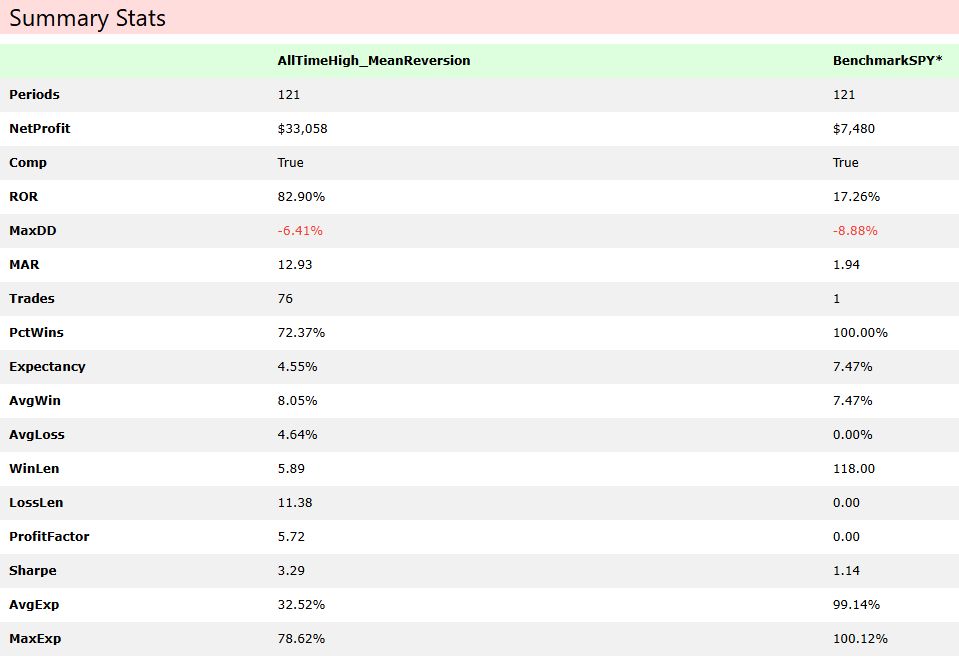

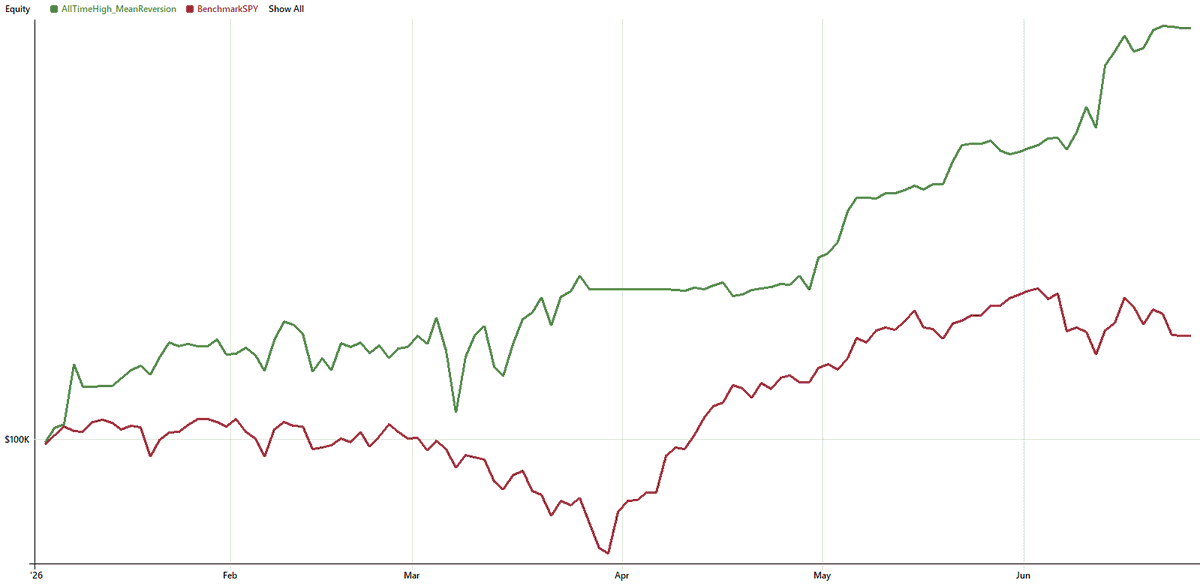

While SPY did +17% with an 8.88% drawdown...

My AllTimeHigh Mean Reversion strategy did +82.90% with only -6.41% max drawdown (ytd).

Sharpe Ratio = 3.29

Full strategy👇