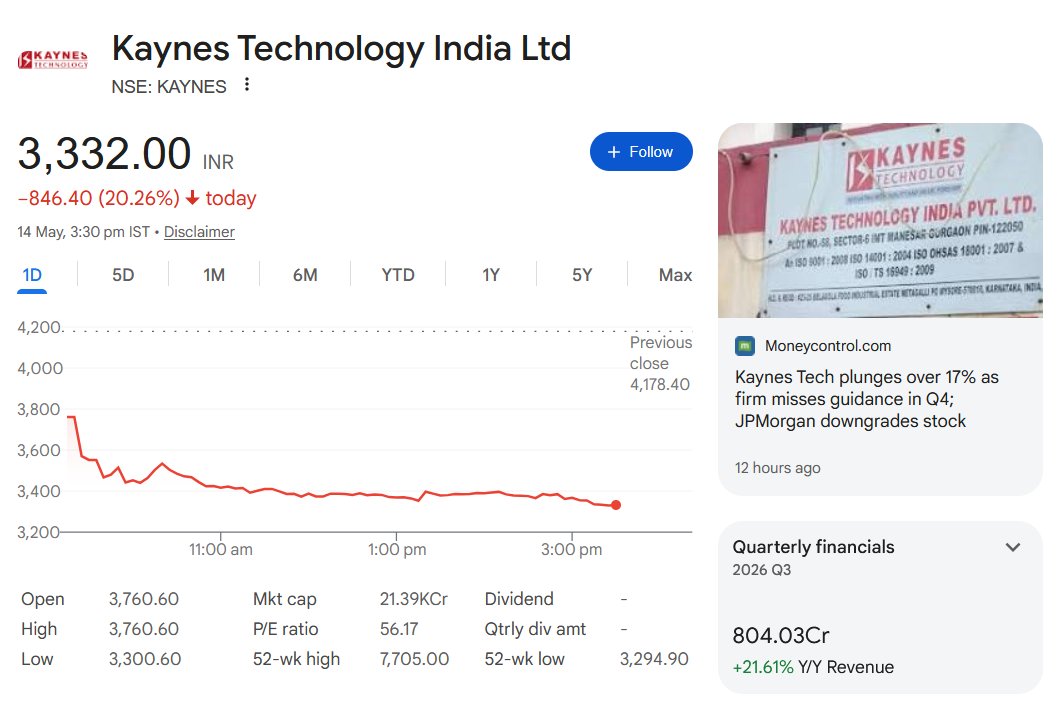

@niveyshak What are ur thoughts on Kaynes Technology right now?

English

ShriyaWealth

1.6K posts

@ShriyaWealth

📈 SEBI Registered MFD| 20 yrs banking | 🚀Simplifying stocks & mutual funds 📈 Wealth | SIP | Long-term investing ⚠️ Not financial advice | DMs open

Kaynes Technologies ✍️ Fresh downside, still price is in range on the fear side ✍️ Retails mostly got trapped here, looking for an exit or book loss ✍️Punching orders still not active, but with an SL this time ✍️ B/S errors are not clerical, markets seems to know something

IMPORTANT ! Govt hikes import duty on gold & silver to 15% from previous 6%. #GIFTNIFTY #NIFTY #BankNifty

The story of that ad. A bet that 700+ words of raw honesty would work. He said it was too long. Too dense. No visuals. Didn't cover the "So what?" "Intent accha hai, par koi farak nahi padega, log nahi padhenge." He wasn't wrong. But Rational Ghost turned out to be less wrong. What happened? Read the story: tinyurl.com/viraladblog