Tech Spectator

752 posts

Tech Spectator

@SpectatorTech

Active investor and author covering broad technology sector. Posts are not financial advice.

Katılım Aralık 2020

513 Takip Edilen163 Takipçiler

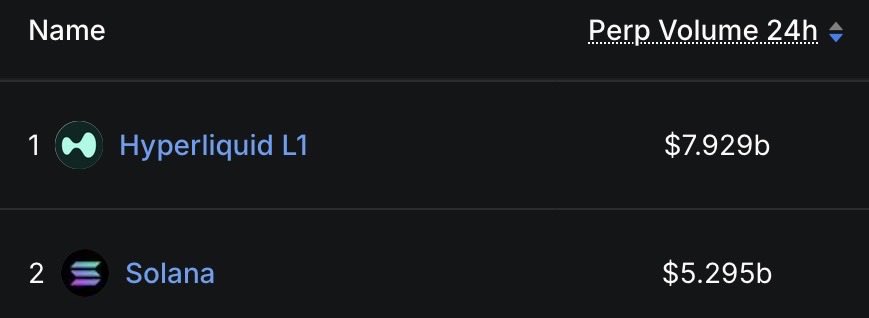

Solana perp volume climbed to $5.295B!!! It’s 67% of Hyperliquid’s volume. At this pace, Solana will claim the top spot for perp volume in a couple of days. Perp trading is the entire reason that Hyperliquid exists. Solana is winning everything! $SOL $HYPE #Hyperliquid #Solana

English

English

@WatcherGuru @SenWarren she never has an open mind and never learns. Democrats are doomed for being in a position against the people.

English

JUST IN: 🇺🇸 Senator Elizabeth Warren says the crypto Clarity Act will "blow up the economy."

"It pushes more of the economy into crypto!"

English

@IamRamenPanda 不仅选股有问题,还经常高买低卖,或者赚了点就马上出手哪怕是好公司(比如最近的AMD)没有长线投资的勇气,最傻的网红,专骗傻子的现金

中文

因为2021年买入比特币被虚拟货币圈捧成“神”的木头姐,Cathy Wood,她实际上是美股里最傻逼的“明星”基金经理

木头姐的基金Ark “创新基金”,不但彻底踏空了最“创新”的半导体大牛市,基金的股价仍然没有回到2020年那个大放水炒空气的高点

就她这样的臭鞋还配“创新”,还被一众币圈人众星捧月观点当圣旨看

中文

@CryptoCurb It's a speculative, high risk play. Be careful, in my assessment, Solana is eating HL's perp market and will surpass HL

English

LATEST: 📈 Tom Lee says Ethereum could hit $62,000 if it becomes the payment rails of the future, a scenario he believes will be the case.

English

@coinbureau The corruption in America’s political system is truly baffling, exemplified by Warren. How come she remain in the senate forever showing this stupidity. Every time she opens her mouth, it felt like her own acting drama rather than serving the people.

English

🚨NOW: WARREN LEADS MASSIVE AMENDMENT PUSH AGAINST CLARITY ACT

More than 100 amendments have been submitted ahead of the Senate Banking Committee’s markup vote on the CLARITY Act, per Politico.

Sen. Elizabeth Warren alone has reportedly filed over 40 amendments, signaling intensifying political resistance against the landmark U.S. crypto legislation.

English

🔥 兄弟们,汤姆·李更加“狂暴”了!他大胆预测以太坊要涨27倍!目标价62500 美元!他认为 ethereum:native第三次盘整很快就会结束!

他的核心观点是:以太坊 ethereum:native 的原生网络,可能会成为未来 AI 代理和代币化资产之间“转账、结算、支付”的底层通道。

简单点理解,未来 AI 不只是聊天,它会自己花钱、自己买服务、自己结算任务。而这些钱和资产如果都在链上,以太坊就可能成为它们之间最重要的支付和结算网络。

也就是说,AI 代理需要账户,代币化资产需要结算,而以太坊提供的,正是这两者之间的支付轨道。

如果未来 AI 是新劳动力,代币化资产是新资产形态,那么以太坊想做的,就是它们之间的金融底层高速公路。

大家怎么看,觉得他这个想法,V神能搞出来吗?

以太坊要涨30倍,你敢想吗?

中文

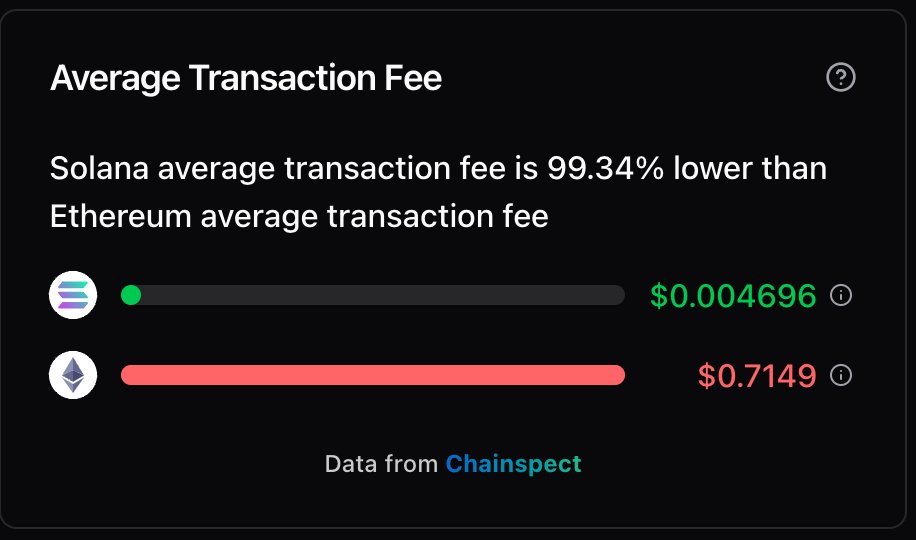

@SolanaSensei @solana @chainspect_app @toly @jito_sol @anza_xyz @SolanaFndn @luminaries I think you meant to say 100x lower not 100% lower

English

Almost 100% lower in transaction fees, the comparison is just diabolical

It's been over 5 years on Solana and I still don't understand why anyone should use anything other than Solana.

English

@MikeLongTerm @AMD They are backward-looking talking heads while the market is busy rerating for $20 earnings/share. I remember when AMD was around $20 the same people laughed when someone brought up price target of $70. God knows how many newbies will be victims by listening to these talking heads

English

BREAKING $AMD| CNBC is implying AMD the biggest bubble

They also said AMD is trash at $30-$50 at $100.

"Do we even need @AMD "

AMD will become the top 10 largest companies whether they like it or not.

It is ok. AMD is not for everyone!

Not Financial Advice! DYOR!

Mike@MikeLongTerm

$AMD is easily a $1,200 stock IMO| CPUs TAM 🧵 Not Financial Advice! DYOR! In this thread, I want to discuss the actual TAM for CPUs data center for just 2026, where many are giving different ranges, where I don't agree with. I will explain in detail why I disagree with these research firms and financial analysts using Math. And this thread should not be treated as Financial Advice. I'm just explaining my research and thought process so we can have a discussion. In 2024/2025, I gave out $620 PT for FY2026 was too conservative for AMD potential. At the time, It was early and many were just laughing, that PT was unrealistic and the AI world is run on GPUs only. Today, most of these folks are laughing with me. That is ok, I dont offer financial advice, and I do not need everyone to agree with me. I respect other opinions. If you enjoy this kind of thread, slap the like/repost/bookmark. If you want to support my work further and gain more in-depth analysis, consider subscribe! In early 2026, hyperscalers, enterprises, and OEMs are scrambling as Intel and AMD server CPUs are largely sold out for the year, with prices jumping 10–20% and lead times stretching from weeks to months (or longer for certain SKUs). What was once a GPU dominated story has flipped: the shift to explosive Agentic AI with its multi-step reasoning loops, tool calling, multi-agent orchestration, real-time data movement, and reinforcement learning, is dramatically tightening CPU:GPU ratios from the old training-era 1:4–8 all the way to 1:1 to 5:1 or even CPU-heavy configurations. CEOs across NVIDIA, AMD, Intel, Google, Meta, Microsoft, and public companies have been sounding the alarm on CNBC, Bloomberg, and earnings calls. CPUs are “cool again,” and in many agentic deployments they are becoming the new bottleneck alongside (or even ahead of) GPUs and custom ASICs. In 2025, roughly 12-15m AI GPUs + AI ASICs GPUs shipped, and is expect to be 15-20m units by 2026, where it suggesting Training demand is not going away. The actual TAM is structural, multiplicative demand that has already forced AMD to double its long-term server CPU TAM forecast to >$120 billion by 2030 (>35% CAGR), with Dr. Lisa Su noting Q2 2026 server CPU sales expected to surge 70%+ year-over-year and demand “far exceeding expectations.” At the same time, AMD’s secured 30–40% share of TSMC’s initial 2nm capacity (behind only Apple’s >50%) positions it to ramp Zen 6-based EPYC Venice exactly when this agentic wave hits hardest but even that aggressive five-fab 2nm expansion (with plans scaling toward 11 total advanced facilities) cannot instantly close the gap in the near-term. Supply constraints on wafers, advanced packaging, and power are compounding the squeeze, just as hyperscalers forward-buy and lock in long-term deals. 1. The actual potential TAM Various sources and institutions are giving $50-$160-$200B CPUs TAM toward 2030, and i disagree, where supply is severely behind vs Demand by at least 2-3 years or even longer by some estimates. The actual TAM will probably be 15-20m for FY2026. The typical average selling price from low to high end is $5,000 to $15,000, but due to rising memory, and different inflationary pressures on Semi, it would be more logical to think between $7,000-17,000. A. CPU:GPU Ratio at 1:1 A basic calucation at mid range =12,000 x 15-20m CPUs= $180-$240B TAM B. CPU:GPU Ratio at 5:1 = $12,000 x 75m-100m CPUs= $900B-$1.2T TAM Of course TSMC cannot even supply 20% of this massive inflection TAM in 2026. But do we think of Demand for TAM or Supply for TAM? Hence we are seeing massive 2nm Ramp from TSMC for $AMD. IMO, conservatively, I would take down 15-20% on 1:1 or $135-$192B TAM for just 2026. Im not even talking about 2030. We are just months into this, it is impossible to estimate Cagr atm, but this is 1-5 agents running tasks, I wrote a thread on 24/7 autonomous agents thread, where companies could use 50-250 agents to run tasks for them 24/7. It would require a different structural CPU:GPU to bring down the cost of token as well as handling the Orchestration bottleneck. GPUs would be useless and sit idle waiting for CPU due to highly CPU-intensive nature. The cost per Million tokens must come down more rapidly for this 50-250 autonomous agents to work, otherwise the token cost would be too enormous. Helios Rack is estimated to bring inference cost down to $0.0003-$0.0005/M tokens with 18 EPYC Venices along with 72 MI455x and other chips+ Components. A heavier or CPUs dense rack would bring down inference cost further. EPYC Verano(2027 gen 7 AI-optimized) is expected to drive inference costs meaningfully lower than the Venice baseline likely to the $0.00002–$0.00025 per million tokens range (or even sub-$0.00015 in highly optimized agentic/batch workloads). Verano have higher core counts than Venice, LPDDR5X SOCAMM2 memory support, more AI optimized and Next-Gen rack density & efficiency. 2. $AMD secured at least 30-40% of TSMC 2nm capacity and Memory from Samsung through 2028-2030. 2 2nm fabs are entering ramping phase toward 60-65k wafers per months and 5 dedicated 2nm fabs entering mass production/ramp in 2026. Will link sub threads below if you are interest for full detail. Apple is reported to secure 50%+ 2nm capacity for Iphone 18 and Mac chips and AMD secured at least 30-40% capacity while $NVDA $AVGO $ARM $AMZN $GOOGL and others are on 3nm. This broader aggressive ramp from TSMC to target up to 11 fabs is to address $AMD massive growth ahead. Where $ARM is facing massive CPUs supply constraints as they have to compete with other Mega Cap players on 3nm allocation. And $INTC is also facing supply constraints for data center CPUs and PC per management with lead times extrended to longer than 12 weeks. Dr. Su is aiming for higher than 50%+ Market share, and I believe it is achievable in 2026 or 2027 as AMD has the strongest CPUs offerings. Dr. Su did not want to take advantage of the shortage and she said during the Q1 earning call, AMD is prioritizing Units shipped while guiding margin to be inching 60%. If Jensen were in charge, I'm sure margin would be 70-75% in this kind of severe CPUs shortage condition. But that is not how Dr. Su operates for more than a decade. She wants most market share. So we will see it in revenue growth, but as TSMC ramps faster and faster, AMD Operating and FCF margin will massively improve vs prior decade. A significantly higher margin profile than before. 3. How I came up with $1,200 withint 12-18 months? At $1,200/ share, that would be around $2 Trillion MC. I expect FY2027 revenue to be $124-$144B where data center revenue dominates overall revenue. AI GPUs: I will stick to the lowest end so show u that I'm conservative at $18B for each GW vs $NVDA Rubin is $30B+ (most likely Helios Rack in the $20B+ due to memory price rising). We know deals with @OpenAI and @Meta are around 12GW and additional multi-customers at multi-GW scale were hinted and will be revealed as we get to July 22-23 2026 Advancing AI event. For now I will conservatively add a bit more to this model. (3-6GW Helios Rack Range) EPYC Venice is reported to be in $15,000-$20,000. However large customers will likely to enjoy $10-$12k discount. I expect AMD to be able to ramp 7m EPYC Venice for entire 2026 and 3-4m of EPYC Verano(higher price than Venice). If we take an average selling price of $10,000 to be on the conservative side. Take down another 30% to be even more conservative on projection. I like to be conservative. That would be ~ 7m EPYC CPUs(Venice + Verano) for FY2027 or 583,000 units per month or 15,000 additional 2nm wafers per month which is completely reasonable for current TSMC Ramp, and I may be too conservative here. EPYC Verano and MI500 series will also be on 2nm. AI GPUs: 3GW x $18B= $54B EPYC CPUs: $10k x 7m CPUs= $70B = Data center revenue alone is $124B Other segments= probably in the $20-$25B FY 2027. FY2027 revenue = $124-$149B At 7m EPYC CPUs for entire 2027, that would be more than 50% market share when we comp it to availability from supply side, not from total Demand. It is possible that TSMC could significantly ramp even more capacity in 2027, so we will see. Metric Q1 2026 FY2027 Gross Margin 55-56% 60-62% Operating Margin 25-26% 32-35% Net Income Margin ~22% 26-30% FCF Margin 25% 28-30% At $124-$149B Revenue FY 2027 Net Income would be $32-$44B EPS would be $20-$27 (GAAP) Non-GAAP would be $25-$31 At $1,200 a share or $2T valuation that would be: 13.4-16x Price to Sales (P/S) 38-48 P/E At this kind of growth of AI SuperCycle, I think it is very reasonable valuation. If we use today at $406/share or $661B MC: 2027 P/S = 4.4x-5.3x 2027 P/E = 13x-16x Is AMD today expensive or cheap to you? Above is already a very conservative where I trimmed 20-30% of doable units. Meaning, there could be upside if TSMC is able to ramp meaningfully like they are planning. Conclusion: A $1,200 per share valuation IMO for AMD in FY2027 is not expensive at all; it is, in fact, conservative when viewed against the structural explosion in agentic AI demand we have mapped out. With server CPU TAM potentially scaling into the $100–$200B+ range in just CPU:GPU 1:1 Ratio for just 2026. AMD positioned to capture 50%+ share thanks to its 2nm TSMC allocation advantage and full-stack leadership, the company could realistically deliver $124–149B in total revenue and $25–$31+ non-GAAP EPS. At those levels, $1,200 implies a 2027 P/E = 13x-16x. Entirely reasonable for a company that will have become the clear Inference Queen (and in many workloads the preferred) AI infrastructure provider, with operating margins expanding above 30% and tens of billions in high-margin rack-scale AI revenue. Dr. Lisa Su was right presciently so about the Agentic AI inflection all the way back to her early 2022–2023 commentary on the coming shift from pure training to inference and orchestration-heavy workloads. While the broader market only fully woke up to this in 2026 when she doubled AMD’s long-term server CPU TAM forecast to >$120B by 2030 (with >35% CAGR), Dr. Su and her team have consistently positioned the company at the center of the CPU renaissance. The explosive demand we are seeing today, sold-out lines, rising ASPs, and hyperscalers forward-buying entire gigawatts of Helios-class systems is exactly the outcome she forecasted years ago. Not Financial Advice! DYOR!

English

@FurtureRichKid It’s a huge gap-up. Technically it’s not possible. Also this gap-up was supported by fundamental change in business outlook. Very unlikely to revisit $300, what happened? You missed it?

English

@DavidANicholas Memory chips are commodity, memory price has cycles, simple as this

English

Micron is trading at roughly 9x forward earnings while $AMD trades near 60x.

Micron generates about five times more profit, yet trades at roughly one-fifth the multiple.

I believe Wall Street has this wrong, and $MU reaching $1,000 within two years is not out of the question.

English

@treasureh8nter Good luck with trader’s mindset. It’s very difficult to time it. It’s better to ride than time the market.

English

Personally I do think that $AMD will pullback to the $300’s after earnings even if has a stellar earnings which it most definitely will be!!!

Anything under $300 is an opportunity to load up even more cheap $AMD shares and build an even bigger position!!!

We will be in the $400 to $450 range by year end! ☝️

Cole@StockOptionCole

$AMD Earnings on Tuesday Either the fire is put out and pulls back to 330 for a round trip then bought up fast on the road to 400+ 2026🎯 430, 470 If this drops post earnings this would be a case of BUY THE FUCKING DIP IMO The Semiconductor rally is nowhere near done and cycle will last multiple years Memory constraint directly benefits AMD. Especially if NVDA is stumbling right now → AMD gets a large expansion + stronger inflow. Noticing Whale 600C flow too

English

@hr63859681 @dingzhonggood 斩杀线是中文语境带有中共宣传口政治立场的标签用语,在美国根本没有这个说法,站不住脚,我就不评论了

中文

来美国两年了,说实话还是不太适应。刚来美国的人,总喜欢把美国和中国对比。我也不例外。

说实话,我感觉美国这个国家特别讲究实用。就拿基础设施来说吧,公平地说,确实美国的基础设施比中国落后不是一个等级。说美国的基础设施比中国落后几十年不为过。

美国的马路几乎都是水泥的,而且修修补补,车开起来颠簸得就像坐船一样。红绿灯,没有倒计时,很多直接就挂在电线上,摇摇晃晃,还是歪的。电线杆几乎都是木头的,很多都快倒了。

地铁看起来就像中国以前的旧火车。

还有购物,总感觉美国的物品种类特别少,打开亚马逊,无论搜什么,就那几样东西。以至于我家孩子买个书包和水杯,都跟同学撞脸。不像淘宝,上面琳琅满目,无论什么东西,都是种类繁多。美国几乎没有直播带货,外卖又贵,又不方便。

城市方面,美国只有市中心,才有现代化摩天大楼的都市派头,其他地方就像农村。住宅区和商业区分离,不像中国下楼就可以买各种东西。

交通工具方面,美国几乎只有公交和汽车两样。虽然也极少数人骑电动车和自行车,但少又不方便,因为美国很多地方都没有自行车道,以至于自行车和电动车根本无法骑。

美国有很多人都开二手汽车,很多也都是十几年的车,还有很多车破破烂烂,连玻璃都是用塑料纸糊起来的。

说实话,我在中国几乎很少看到有人开二手车,更没有看到被撞得破破烂烂的车在路上跑。

还有看病,美国看病相当麻烦,几乎所有医生都需要预约,而且专科医生还需要转诊才能看。住院更是需要转诊。

另外很多诊所居然周末不开门,所以周末就只能多花钱挂urgent care。

不像中国一年三百六十五天,一天二十四小时看病都极其方便。

所以从内心讲,来美国两年多,我仍然没有完全适应美国。尤其是在美国感到就像离群索居了一样,到处看不到人。再加上这么多跟中国对比,都觉得中国很好,所以虽然美国很好,但也总是怀念中国。

但是转念又一想,中共在这些方面实现弯道超车,确实胜过欧美国家很多,中共这些其实都是为我们建的呀。

这是我的朋友讲的,我觉得非常有道理。

中共把中国建得这么好,就是为我们建的呀。这是为我们作嫁衣裳。

中共马上就要倒台,到时候我们回中国,这么好的中国,不是为我们建的吗?

一想到这一点,就觉得非常开心。

虽然黎明前的黑暗很痛苦,但是曙光已经来临,大家是不是跟我一样开心啊?

中文

@Wakoohead @dingzhonggood 流浪汉占美国总人口能有多少比例?这里说的藏富于民当然是统计意义上的绝大部分人口:就是如果你肯干、守法,不管工作贵贱,普通人都可以有体面的生活和福利,这个在中国根本不能保证的。再说流浪汉的成因主要也不是因为穷困,很多人是毒瘾和精神问题

中文