Today's bias

SPY is extended at $720 (+7.8% vs 200SMA, NTM PE 20.8x = "slightly rich") with the composite improving (+0.20σ, +0.51σ over 20d) on a tape-led rally — ride the regime turn, but don't add into the overbought watch and the 30Y at 4.99%.

What changed

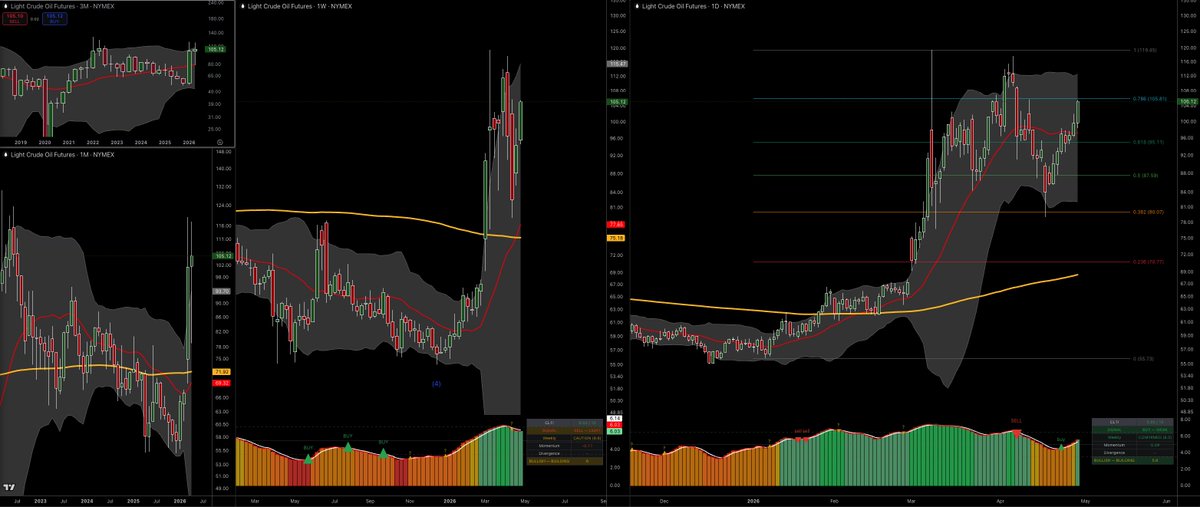

SPY pushed to $720 (3M chart shows new highs) — daily tape now flagged OVERBOUGHT–WATCH. Move is real but stretched; fresh longs have poor risk/reward here.

Long-end yields jumped: 30Y 4.99%, 10Y 4.46%, 2Y 3.97% — bear-steepening pressure returning. EFFR-vs-30Y spread now +1.35% (curve says fully accommodative). Term premium 0.65% and rising again.

Risk panel +0.55σ confirms no stress — VIX 17.7, VIX/VIX3M 0.87 (deep contango), HY OAS contributing +0.89σ. Credit is calm even as rates back up.

Sentiment -0.46σ stays the divergence — NAAIM exposure -1.13σ (managers underweight) while tape rips; this is fuel, not a top signal yet.

Macro panel -0.33σ, Liquidity -0.62σ unchanged — net liquidity still tightening (-4.2% YoY), bank reserves draining, M2/Gold ratio at 0.67/10. The structural drag the weekly flagged is still there.

Earnings Health 4.78 → "WEAKENING, BULL AT RISK" — NTM PE 20.8x against softening earnings is the core fragility under this rally.

Today's risk

30Y above 5.00% closes the rate-cut narrative and pressures the PE multiple directly; currently 4.99%, one bad print away.

SPY losing $716 (yesterday's pivot on the 1D chart) flips daily momentum and likely triggers the overbought-watch unwind toward 700 / 671 (50d).

DXY at 98.29 sitting on 200d — break lower would re-fuel risk; break higher (with yields up) is the squeeze that hurts everything.

Cross-check

Formal Composite (5.10 NEUTRAL) and Cycle (WEAK 5.5) disagree with the tape (+0.67σ Technical, +0.55σ Risk) — formal score leads on size (don't size up; structural backdrop is mediocre), tape leads on direction (stay with the trend until breadth or credit cracks). Translation: hold longs, don't add, tighten stops under $716.

English