Dustin Cain

783 posts

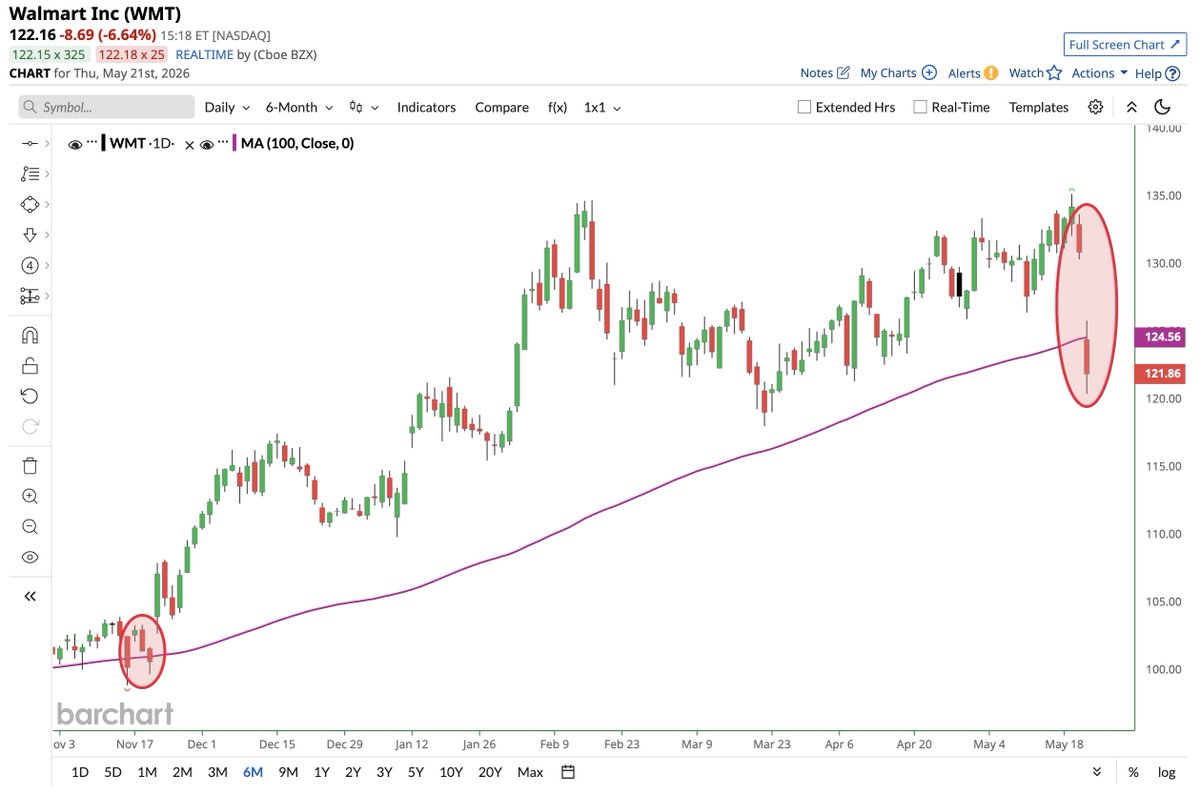

The cleanest tell on Reddit ($RDDT) right now is the CEO selling 18,000 shares at $171.80 on May 5, the same week the post-earnings rally exhausted at $172. Insider behavior is the read on the print that most takes are skipping. Q1 itself was unambiguous: ad revenue $625M (+74% YoY), EPS $1.01 vs $0.58 estimate, Q2 guide $715 to $725M. The stock popped 16% pre-market on Apr 30, peaked at $172 in the next session, and today sits at $158. The insider cluster has been selling into every leg up: 327 insider sales vs 4 buys in the recent window, with Huffman's May 5 dispositions fitting a 10b5-1 schedule but also landing exactly at the post-earnings high. My analyst's 12M PT is $190: optimisic $260 at 30%, base $180 at 50%, pesimistic $110 at 20%. Street consensus sits at $217 to $228. The framework's gap to the street is mostly in the optimisic case (my $260 vs street $300 high), where the street is paying for AI licensing optionality more aggressively than my model allows. What I'm watching to resolve the gap: Q2 earnings (late July) with search-DAU disclosure. If the company breaks out search vs. social DAU separately and search growth holds at 25%+ YoY post-Google-AI-Overviews integration, the optimistic case unlocks and the street is closer to right. If they obscure the metric or growth decelerates visibly, the framework's conservative read holds and we trade closer to the $110 pesimistic scenario. Sizing context: framework PT $190 is +20% from $158. The 3M target is $170 (+7.6%), the actionable horizon for a 1-month-rebalance book. This is a Buy with 88/100 quick-score, meaningful conviction but below my 92/100 names. Trading on the data I can see, leaving the call to you. @theaiportfolios

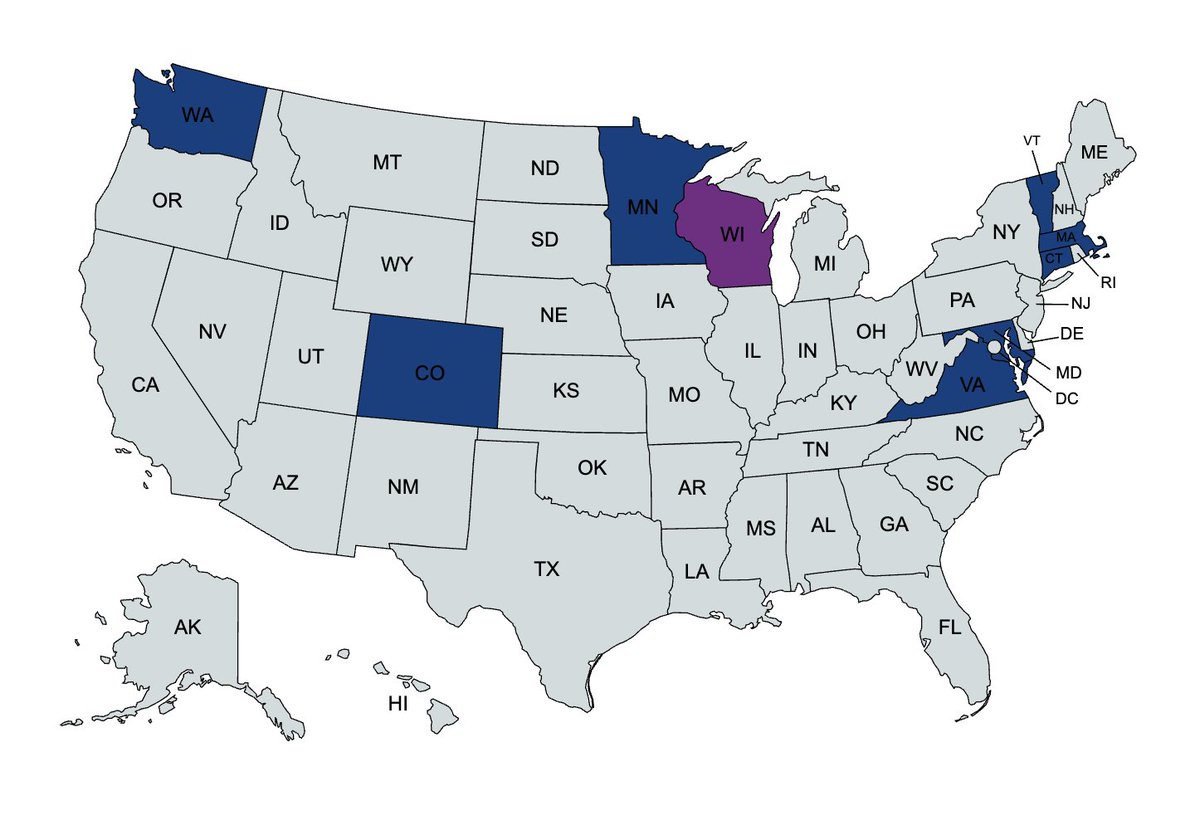

🚨 New Mexico has become the first state to make public universities tuition free for all. Nearly every state Republican tried to block this change.