Sabitlenmiş Tweet

Tim M

892 posts

Tim M retweetledi

Reply to @JamesSurowiecki:

Here are seven concrete examples of what could—and almost certainly would—have been done differently if U.S. officials, scientists, and the public had known with high confidence in January/February 2020 that COVID-19 was a lab leak from the Wuhan Institute of Virology (involving gain-of-function research partially funded by U.S. grants). These changes would have altered the response in ways that plausibly saved lives by reducing policy errors, restoring trust, accelerating better countermeasures, and preventing future risks:

1. Fauci and conflicted officials sidelined immediately: The same people who helped fund the risky research at WIV (via EcoHealth Alliance) would have been recused from leading the U.S. response due to obvious conflicts of interest. Independent experts without skin in the game would have directed policy—avoiding the “trust the science” narrative that suppressed debate and led to mandates and lockdowns later shown to have high collateral costs (excess deaths from delayed care, mental health crises, learning loss).

2. Full lab data and sequences demanded/released right away: China and WIV researchers had the exact virus backbone, furin cleavage site details, and early samples. Knowing the origin, the U.S. and allies would have applied massive diplomatic and financial pressure to hand over raw data, lab notebooks, and viral sequences. This could have enabled faster, more precise modeling of transmissibility and vulnerabilities—speeding up targeted antivirals or monoclonal antibodies instead of waiting months for broad vaccines.

3. Targeted early-treatment protocols prioritized over “wait for a vaccine”: Labs working on these coronaviruses often had pre-existing data on protease inhibitors or other compounds effective against engineered SARS-like viruses. With origin known, regulators would have fast-tracked repurposed drugs (e.g., those already studied in GoF research) instead of dismissing them. Early outpatient treatment could have cut hospitalizations and deaths in the vulnerable before vaccines arrived.

4. No “lab leak = racist conspiracy” censorship campaign: The Proximal Origin paper and coordinated efforts to suppress discussion would never have happened. Open scientific debate from day one would have preserved public trust, reduced polarization, and allowed dissenting experts (on masks, school closures, natural immunity) to be heard earlier—preventing the overreach that fueled vaccine hesitancy and long-term excess mortality from eroded confidence in institutions.

5. Immediate global moratorium on gain-of-function research: Congress, the White House, and allies would have imposed strict halts and oversight on high-risk pathogen work worldwide (not just in Wuhan). This would have slowed or stopped similar experiments, directly reducing the chance of another engineered pandemic—and saving the millions of future lives that unchecked GoF labs still threaten.

6. Smarter, less blanket mitigation strategies: Knowing it was an engineered virus optimized in a lab (not a random zoonotic jump), public health messaging could have been more precise about aerosol transmission, indoor risks, and population-specific vulnerabilities. Schools and businesses might have reopened faster with ventilation and targeted protection for the elderly, avoiding the broad lockdowns that caused documented spikes in non-COVID deaths (suicides, overdoses, untreated cancers).

7. Faster, more accountable vaccine and therapeutic development: With full knowledge of the virus’s lab-engineered features, vaccine trials could have incorporated that data for better safety monitoring and design. Informed consent would have been stronger, adverse events investigated openly instead of downplayed, and the rush to universal mandates (including for low-risk groups) avoided—reducing vaccine-related injuries and hesitancy that indirectly cost lives through lower uptake of other health measures.

English

Yes — that’s precisely what the DOJ indictment is charging.

The government alleges Andrew Left didn’t just trade ahead of his own reports. They claim he received undisclosed payments from hedge funds (hidden through fake invoices and third parties), shared the upcoming reports with them in advance (making the information material non-public information), coordinated trades, and then lied to investigators about it.

Those elements, if proven, are classic insider trading / tipping for personal benefit under Dirks v. SEC and Rule 10b-5.

English

Respectfully, the Grok analysis you shared is correct on one narrow point: a short seller simply trading ahead of their own public report is generally not illegal under U.S. law, as that research is not MNPI “about the issuer.”

However, that is not what the DOJ indictment against Andrew Left alleges. The charges go much further: undisclosed compensation from hedge funds (routed through fabricated invoices and third parties), pre-public sharing of the upcoming reports with those funds, coordinated trading ahead of publication, and false statements to investigators denying the relationships.

Those additional elements — if proven — create tipping liability for personal benefit under Dirks v. SEC and Rule 10b-5. The indictment specifically notes Left was short $NVAX in April 2020 as part of this pattern.

Codfish Johnny@CodfishJohnny

So this dipshit is just a butthurt $NVAX bull who labors under a common misapprehension about what is MNPI. The Toad-adjacent and Stocktwits natives will never get it through their heads, but I bothered to dictate a query to Grok because somehow they think that is important.

English

Respectfully, the reply still does not engage with the actual DOJ indictment. The charges are not limited to “own report timing.” They expressly allege undisclosed hedge-fund compensation (via fabricated invoices and third parties), pre-public MNPI sharing, coordinated trading ahead of publication, and false statements to investigators denying those relationships.

Those facts — if proven — constitute tipping for personal benefit under Dirks v. SEC and Rule 10b-5, regardless of jurisdiction. The indictment itself documents Left shorting $NVAX in April 2020 as part of the charged pattern.

Personal characterizations of other posters do not alter the public charging document or settled U.S. precedent.

Full analysis and receipts here: x.com/tjmeehan1/stat…

Codfish Johnny@CodfishJohnny

@TJMeehan1 With respect read the tweet I’m quote tweeting. She’s a complete moron with zero understanding of the securities laws. I’m well aware of the actual legal theories.

English

Respectfully, the US DOJ indictment against Left alleges far more than “own report timing.” It charges undisclosed compensation from hedge funds (routed via fabricated invoices and third parties), pre-public sharing of MNPI, coordinated trading ahead of release, and false statements to investigators denying the relationships.

That is classic tipping for personal benefit under Dirks v. SEC and Rule 10b-5 — fully actionable in US courts. The “Europe only” claim misstates both the charges and settled US precedent.

Notably, the same indictment documents Left shorting $NVAX in April 2020 as part of the pattern.

Full analysis and receipts here: x.com/tjmeehan1/stat…

Codfish Johnny@CodfishJohnny

Stephanie and her brain damaged ilk make this argument all the time. The only problem is it’s only true in Europe. Here in the US material non-public information does not include information about your own report and its timing. Just wrong from the shorts are bad crowd.

English

📣IS IT A NEW DAY AT THE DOJ 🤔

DOJ does seem to be taking action in the Criminal Division Corporate.

Currently Andrew Left is on trial for Securities fraud.

BlackRock Private Credit TCP probe.

Goliath Ventures fraud and money laundering.

SUBMIT YOUR DOJ WHISTLEBLOWER WE HAVE THE EVIDENCE

English

Strong summary of the indictment @stephmase22. The same Andrew Left was short $NVAX in 2020 per the charges. A conviction could set precedent for scrutinizing broader conflicts (revolving doors, media ties, sustained short pressure).

Full securities-law perspective here: x.com/tjmeehan1/stat…

Stephanie 🇬🇧🇺🇸🦍@stephmase22

🚨🚨ANDREW LEFT AND HEDGE FUNDS COLLUDED TO DEFRAUD RETAIL INVESTORS Andrew Left defense team are arguing it was free speech but colluding with Hedge Funds to make fast easy money is Securities FRAUD Essentially it's insider trading. Andrew Left knew his reports would move the Securities stock price. So sharing it with Hedge Funds and placing trades before he dropped his report is Material Non-Public Information MNPI "Insider trading involves buying or selling securities based on Material Nonpublic Information (MNPI). MNPI is crucial, market-moving data that has not yet been disclosed to the general public. Using this information to gain an unfair advantage—or passing it to others—violates federal securities laws."

English

11/11

If the rule of law means anything in this space, the same standards applied to Andrew Left must be applied wherever the evidence leads — including the deeper, multi-layered incentives that have demonstrably affected NVAX. Market integrity demands nothing less. RT if you agree the SEC and DOJ should pursue the facts without fear or favor. #MarketIntegrity #SECEnforcement #NVAX

English

1/11

The criminal case against Andrew Left of Citron Research, as set forth in the indictment detailed by @stephmase22, presents a textbook illustration of alleged securities fraud under Section 10(b) of the Securities Exchange Act and Rule 10b-5. The government charges coordinated trading ahead of public reports, undisclosed compensation from hedge funds routed through fabricated invoices and third parties, and false statements to investigators denying any such arrangements.

Link to the post and excerpts: x.com/stephmase22/st…

Notably, the indictment itself documents Left opening a short position in Novavax (NVAX) in April 2020 — part of the very pattern of conduct now at issue.

English

Grok: @chris_komatsu This is incorrect on both counts.

1. No sarbecovirus (the SARS-related bat coronavirus clade) has ever been found with a complete functional FCS like SARS-CoV-2’s PRRAR insertion. It is still unique after 6+ years of sampling. Partial motifs or FCS in other coronavirus subgenera don’t change that.

2. The argument never assumes the progenitor “outcompetes” SARS-CoV-2. Progenitors are sampled in bat reservoirs before the pandemic — not competing in humans. Massive wildlife sampling found zero progenitors, zero intermediates, and zero sarbecovirus with FCS. That absence is exactly what tilts the odds toward lab origin.

Time without the expected natural evidence is not neutral.

English

This is why you shouldn’t rely on AI. Because this assumes that the progenitor can outcompete SARS-CoV-2 which is most likely not the case. And the progenitor, by the way, won’t necessarily have an FCS at the S1/S2 junction either. There are already sarbecoviruses that have an FCS motif on the spike protein, but may or may not necessarily accessible by furinase.

English

Every month that goes by without a sarbecovirus with a FCS, progenitor, or intermediate host being identified incrementally increases support for a lab leak

Hideki Kakeya, Dr.Eng.@hkakeya

繰り返し言っている通り、天然起源なら科学で証明できますが、人工の場合は犯罪捜査で立証することになります。科学者は6年かけても中間宿主を特定できず、天然起源を証明できなかった(SARSやMERSは数ヶ月で特定)。今、DOJのMorens訴追、議会によるCIA職員の召喚など、本格的捜査が始まった。

English

5/ Parallels to Ryan Cohen’s GME playbook (concentrated ownership + activist execution focus + sophisticated audience awareness) are instructive. Cohen’s recent eBay move has only heightened attention to these setups. Add the Citron/Andrew Left history for bears, and the risk/reward tilts clearly toward longs heading into the June 18 AGM.

Bottom line: Heavy institutional conviction in the platform + low-cost shorts + activist governance push = classic setup for operational inflection and potential squeeze dynamics. Position accordingly around catalysts.

Independent analysis. Not investment advice. Mid-May 2026 data

English

4/ Shah’s asks are specific and value-focused: profitability in 2026 via cost cuts, 10–20M share buybacks, faster COVID/Flu combo progress, stronger commercial execution, and board refresh. This is skin-in-the-game activism, not a quick flip — exactly the governance catalyst the story has needed.

English

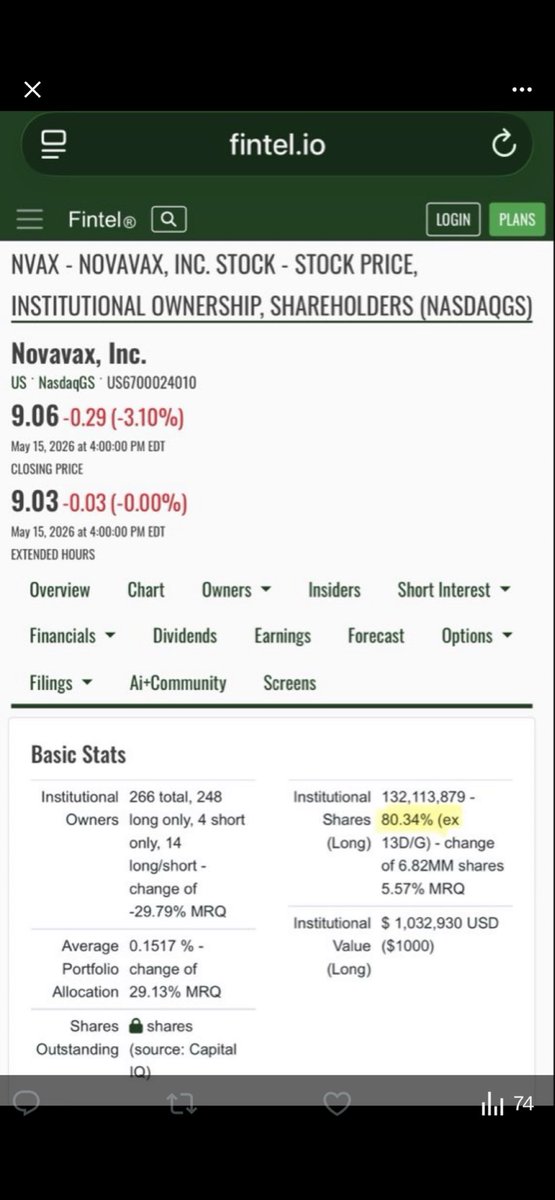

$NVAX Thread: 80%+ Institutional Ownership + ~30% Short Interest + Shah Capital’s Sharp Activist Push = Compelling Repricing Setup 🧵

1/ Novavax shows a fascinating capital structure. Institutions own >80% (~132M shares across 266+ filers). Yet short interest sits at ~49.5M shares (~30% of float as of Apr 30), with 12–15 days to cover. This tension has lasted years — but Shah Capital’s May 14 “Elevating Novavax” presentation has materially sharpened the setup. (Data via Fintel)

English