Noname

15 posts

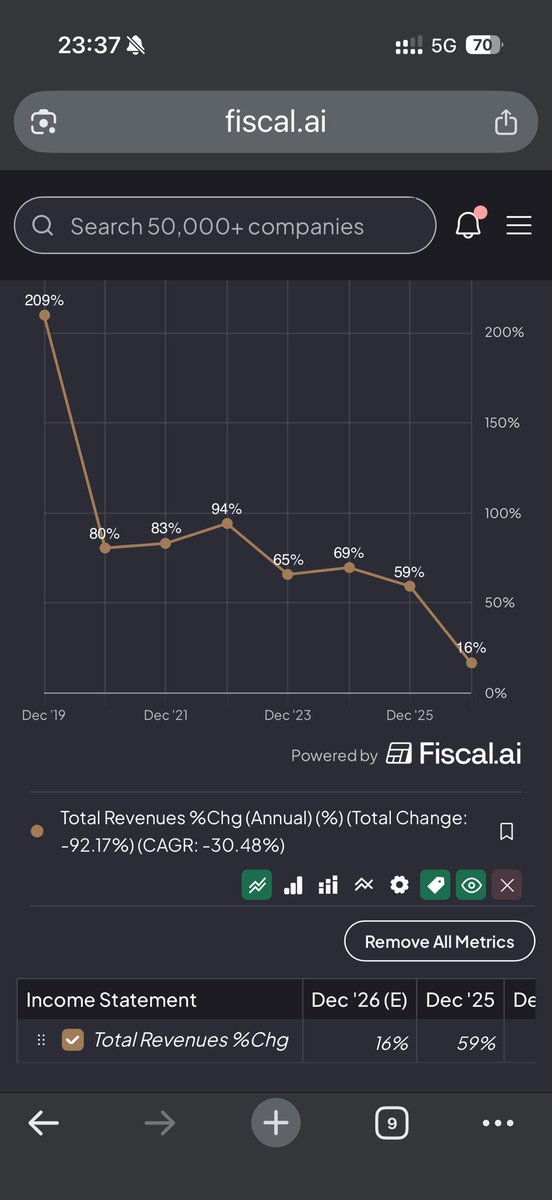

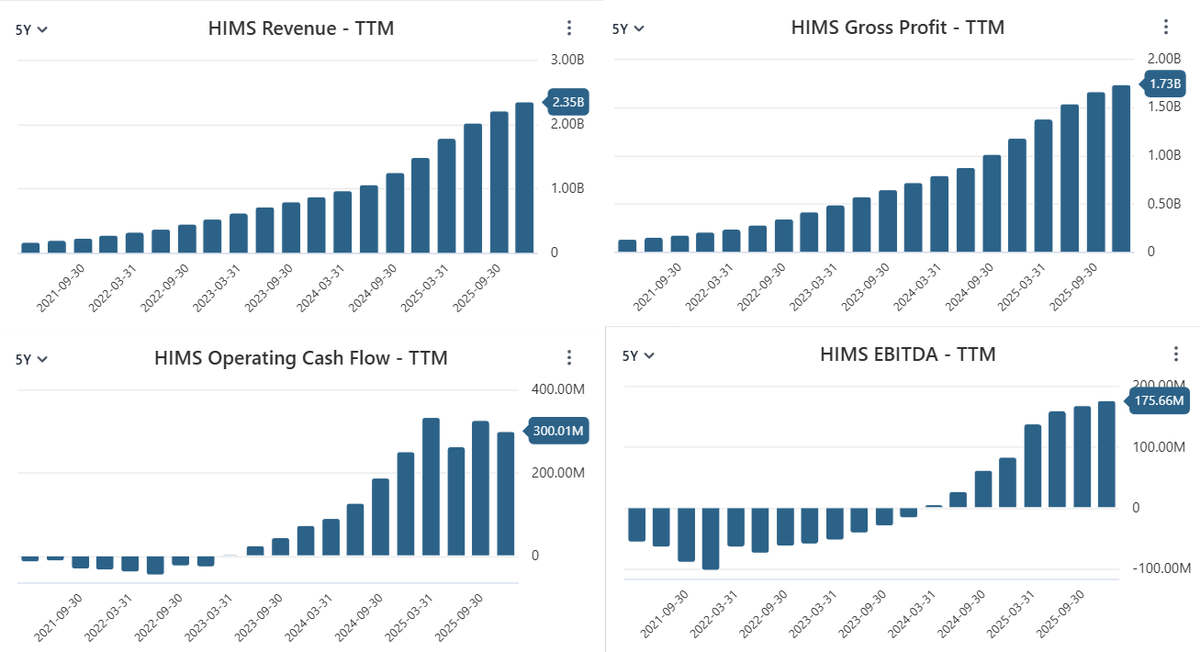

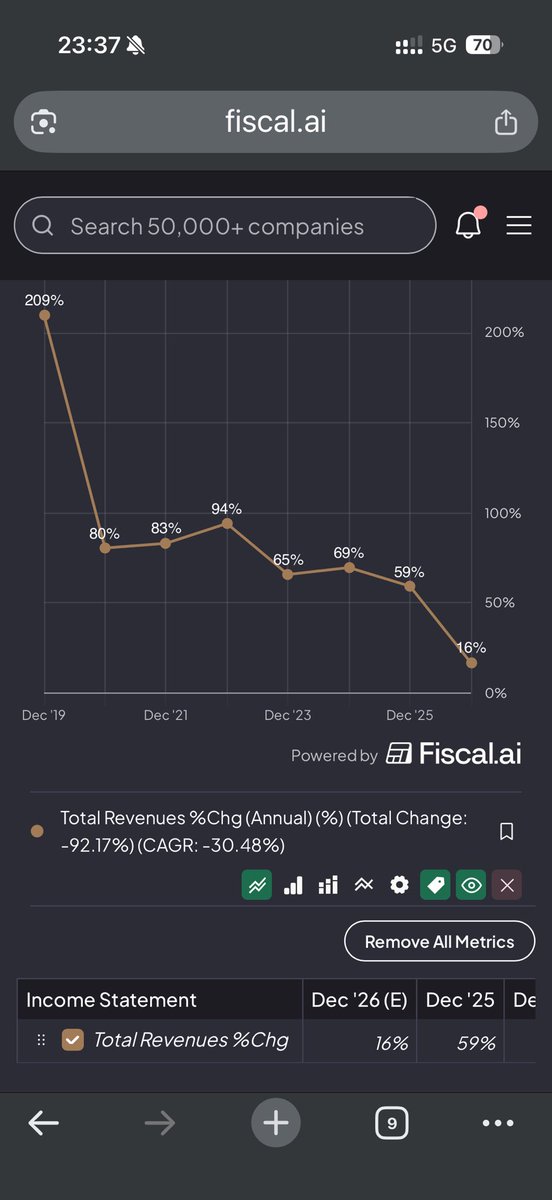

$HIMS 2021-2025 74% Average Growth🍆

2021:

Q1 2021 :$52M

Q2 2021: $61M

Q3 2021: $74M (or $73M in some rounded reports)

Q4 2021: $85M

Full Year 2021: ~$272M (up ~83% YoY)

2022:

Q1 2022: $101M

Q2 2022: $114M

Q3 2022: $145M

Q4 2022: $167M

Full Year 2022: ~$527M (up ~94% YoY)

2023:

Q1 2023: $191M

Q2 2023: $208M

Q3 2023: $227M

Q4 2023: $247M

Full Year 2023: ~$872M (up ~65% YoY)

2024:

Q1 2024: $278M

Q2 2024: $316M

Q3 2024: $402M

Q4 2024: $481M

Full Year 2024: ~$1,477M (up ~69% YoY)

2025:

Q1 2025: $586M

Q2 2025: $545M

Q3 2025: $599M

Q4 2025: $618M

Full Year 2025: ~$2,348M (up ~59% YoY)

So far average growth is 74%

Find me a growth stock that is trading at ~1x Forward P/S or this cheap.

Mike@MikeLongTerm

BREAKING $HIMS Short Manipulation detected🚨 I was right, short sellers are not leaving. They will be here until they can't. They been manipulating price action for 18 trading days now, excluding today. The reason is simple, they see the risk of massive upside, and they want to tame the enthusiasm. They are lucky that sentiment on macro is mad bearish atm, yet $HIMS is holding very well even with massive short selling pressure. At the end of the day, they are trying to prevent that $5-$10B losses or unlimited loss potential. At some point, they will be forced to covered, and that is when you see crazy 30-50-100% gain in a day or 2 days. I have shares with no call option. Time is on my side Long Term. Short sellers should be ready to be clapped! Not Financial Advice.

English

@Iamhuman_ORBS @fundstrat @wintonARK @worldnetwork @tfh_technology @MrBeast @Beast @tbpn Put this beast to work. You giving money and this pussy barely mention you.

English

🧵

1/

Yesterday, I was on @CNBCClosingBell and said we would be “buying the market” here

- even if ‘the low’ is not in place

- mainly because we believe US economy can handle $100, even $120 oil

I know many are skeptical 🤨 but please keep reading 📖

BMNR Bullz@BMNRBullz

TOM LEE: WE’RE 90–95% THROUGH THE SELL OFF “I’d buy the market today.” That’s the call right now. It all comes down to positioning. 🔹 VIX: above 30 🔹 AII sentiment: bulls minus bears ~-20 🔹 Goldman: hedge fund selling = capitulation 🔹 Since 1900: markets bottom early in wars (~first 10%) Too many investors have already de-risked. When positioning gets this neutral, the market doesn’t need good news. Just less bad news to trigger a V-shaped recovery.

English

@Buldak_Crypto Why you think we can fly? I have a shit ton of $orbs but I see zero visibility and and a heavy bag being a $wld treasury treasury

English

What's your single most bullish company right now, the one you'd buy regardless of war, and why?

Let's collect some data from the crowd

English

And it’s in a clear downtrend. To reverse that, we need a better guidance. Maybe Novo and eucalyptus in the second half if that transaction is closed and they can incorporate that revenue but till then I see 10 before 30. Huge competence from many players. Not a dying company but surely market won’t pay premium for a decelerating grow rate

English

Can someone please get me pre-IPO shares of OpenAI?

Ram Ahluwalia CFA, Lumida@ramahluwalia

OPENAI: I WAS WRONG I finally came around on OpenAI. I reviewed @sama letter after they closed their recent financing round. OpenAI is a truly generational company. Sam Altman is a Great Leader that the next generation of founders should exemplify. Thank you, Sam, for all that you do each day and every day.

English

@DiaTSLAPLTR @lovedux You end up being a paid one. Read ur report on the f20. I’ll add a few points you must have forgotten

English

@lovedux To me, it doesn’t matter. I’m long on $RZLV and won’t touch my shares until 2030 and beyond.

English

Up 18% today! $RZLV!

MarketMaverick@DiaTSLAPLTR

🧵1/2 $RZLV — I said I'd read the 20-F and listen to the earnings call. I did both. Here's my full concerns audit. For context: I've been publicly tracking $RZLV for months, posted detailed concerns, engaged directly with @realDanWagner, set specific goalposts before earnings, and now I'm scoring every open item against the actual SEC filing and yesterday's call. Let's go concern by concern. 1- GAAP REVENUE CREDIBILITY "Concern: Was the $40M+ guidance real?" ✅ RESOLVED. $46.8M GAAP revenue filed in the 20-F with the SEC. H2 delivered $40.5M vs H1's $6.3M. December alone: $19.4M. this is in the audited financials, not a press release metric. Beat guidance by 17%. On the call, Dan confirmed: "$19.4M December MRR is actually in our 20-F. This is an audited number." The biggest concern from my original analysis is now backed by an SEC filing. This one is closed. 2- AUDIT OPINION & GOING CONCERN "Concern: Clean audit or qualifications?" FLAGGED. The 20-F contains BOTH a going concern disclosure AND material weaknesses in internal controls. Here's what I found: Going Concern: The filing states "certain conditions and events raise substantial doubt about our ability to continue as a going concern." HOWEVER, management then states the $250M January raise plus existing cash "provides sufficient runway for at least the next twelve months" and believes this alleviates the doubt. Material Weaknesses: Management identified four specific weaknesses: • No formal consolidation system (now implementing ERP) • Insufficient review of subsidiary financial reporting • Inadequate segregation of duties in accounting • Weak controls over business combinations, asset management, tax, and close process Critically, management states: "Notwithstanding the identified material weaknesses, the combined consolidated financial statements fairly present, in all material respects, the Company's financial position." My take: Going concern language with $111M cash + $250M just raised is standard for high growth companies burning cash. The material weaknesses are more concerning . They're admitting their internal controls weren't adequate during a year of rapid acquisitions. They're remediating (ERP system, new finance teams from Crownpeak/Reward), but these won't be resolved until controls operate effectively for a "sufficient period." This is a yellow flag, not a red flag, but it means the numbers could be subject to future revision. 3-ORGANIC VS ACQUIRED REVENUE "Concern: How much growth is real vs bought?" ✅ ADDRESSED ON CALL. Dan provided the clearest breakdown yet: • GroupBy: $18M ARR contribution • Crownpeak: ~$70M ARR (acquired December 2025) • Combined acquisitions: ~$90M of the $232M ARR exit • Remaining ~$142M: organic and partnerships He explicitly said: "The $360M does not include new acquisitions." This is the first time we've gotten this level of granularity. Two thirds organic/partnership vs one third acquired is a much healthier mix than bears assumed. 4-RELATED PARTY TRANSACTIONS / DBLP SEA COW "Concern: $93.9M flowing to CEO's Seychelles entity" PARTIALLY ADDRESSED. The 20-F confirms: • DBLP Sea Cow Ltd is wholly legally owned by Daniel Wagner • The Bluedot Acquisition from DBLP is disclosed as a related party transaction (819,736 shares issued) • In 2025, the company settled $6M in debt to DBLP ($5M cash + 0.8M shares) • There's a rolling consultancy agreement with DBLP paying $20K $50K/month since 2016 • P&L shows ~$79.3M in total related-party costs across sales/marketing and G&A • Share based compensation to related parties: $5.325M in 2025 (down massively from $63M in 2024) The Reward acquisition specifically: Wagner was previously a director of Reward but resigned before the deal and held no shares. The 20-F states it "did not constitute a related party transaction." My take: The related party costs dropped dramatically YoY ($5.3M vs $63M), which is a major improvement. The DBLP consultancy agreement is still active but small. The Bluedot deal remains questionable in principle but immaterial in dollar terms relative to the current scale. This concern has significantly diminished but isn't fully closed the rolling DBLP consultancy needs to end as the company institutionalizes. 5- GOVERNANCE & HEADCOUNT "Concern: 61 employees, dual Chairman/CEO, golden share" ✅ ADDRESSED. On the call, Dan stated: "We now operate out of 32 offices globally with a world-class team of over 1,000 employees." The annual report names executives from Microsoft, Google, Visa, Accenture, Tata Digital, and Deutsche Telekom.

English

@DiaTSLAPLTR @realDanWagner so bro? are u going to post the review of the F20? help retail to avoid this

English

Yesterday I posted 6 things I needed to see from $RZLV earnings. The CEO, @realDanWagner replied "think I hit all your milestones." Let's check the tape:

THE HEADLINE NUMBERS

- GAAP Revenue: $46.8M (guided $40M+ — beat by 17%)

- H2 Revenue: $40.5M vs H1 $6.3M — 543% sequential growth

-December MRR: $19.4M = $232M annualized run rate

Gross Margin: 66% blended, 90%+ core software

- Net Loss: $101.4M (vs $173.5M in 2024 — improved 41.5%)

- EPS: -$0.38 (vs -$1.06 prior year — improved 64%)

- Cash: $111.1M (vs $9.7M a year ago)

- 2026 Guidance: RAISED to $360M revenue (from $350M)

- ARR Exit Target 2026: $500M+ reiterated

Now let me score this against my checklist:

1- Audited GAAP Revenue — DELIVERED ✅

I asked for the $40M+ guide to be confirmed. They delivered $46.8M with the 20-F filed with the SEC today. The H2 acceleration is real — $40.5M in H2 vs $6.3M in H1. December alone was $19.4M. That's not guidance anymore, that's audited GAAP revenue in an SEC filing.

2- Audit Opinion — PENDING ⚠️

The 20-F is being filed today. I need to read the auditor's report in the full filing for any qualifications, going-concern language, or material weakness disclosures. The press release doesn't address this. I'll update once I've reviewed.

3- Cash Position Post-Reward — STRONG ✅

This was a major concern. They ended 2025 with $111.1M cash (up from $9.7M). But note: this is BEFORE the $230M Reward acquisition which closed Feb 2026. They also raised $250M in January. So the math: ~$111M + $250M raised - $230M Reward = roughly $131M entering post-Reward. Management explicitly stated "zero requirement for additional operational equity." That's a direct answer to my dilution concern.

4- ARR-to-GAAP Conversion — PARTIALLY ADDRESSED ⚠️

The gap has narrowed but remains. $232M ARR vs $46.8M GAAP still shows the majority of contracted revenue hasn't been recognized under ASC 606. However, the trajectory is clear: $19.4M December MRR means they were already recognizing revenue at a $232M annual pace by year-end. The definitions page confirms the $232M contracted revenue figure is based on annualizing December's actual revenue. That's more credible than prior ARR claims.

5-Related-Party Disclosures — IN THE 20-F ⚠️

The income statement shows related-party transactions embedded in both sales/marketing ($1.8M + $1.0M) and G&A ($8.1M + $68.4M). That's $79.3M in total related-party costs disclosed on the face of the P&L. I need to read Note 14 in the full 20-F for the breakdown. This remains the area requiring the most scrutiny.

6- Organic vs Acquired — NOT BROKEN OUT ❌

The CEO letter explicitly calls this a "Roll-Up strategy" and names GroupBy, Crownpeak, and Reward as the drivers. The annual report doesn't provide an organic vs. acquired revenue split. This is still a gap.

BALANCE SHEET DEEP DIVE

What caught my eye:

• Total assets: $611.7M (vs $21.2M prior year) — acquisitions transformed the entity

• Goodwill: $168.4M (didn't exist last year) — all from acquisitions

• Intangibles: $239.2M (vs $6.8M) — acquired IP and customer relationships

• Deferred revenue: $46.5M (vs $1.2M) — this is bullish, it's cash collected but not yet recognized as revenue

• Short-term debt: $102.1M (new) — includes Crownpeak acquisition debt of $151.9M taken on

• Accounts receivable: $39.2M (vs $0.7M) — real clients owe real money

• Total liabilities: $364.9M vs equity of $246.8M

WHAT'S ACTUALLY NEW AND BULLISH

• $46.5M deferred revenue is the single most underappreciated line item. That's cash from clients sitting on the balance sheet waiting to be recognized. It's a forward revenue indicator.

• Operating loss improved 37% despite massive scaling — operating leverage is emerging

• Net loss: only $34.2M was actual cash burn; the rest was non-cash items (impairments, share-based comp, extinguishment losses)

• Raised 2026 guidance to $360M (from $350M) — they're getting more confident, not less

• Earnings call held today at 8:30am ET — they did exactly what I asked for

WHAT STILL CONCERNS ME

• $63.3M impairment loss — on what? Need the 20-F footnotes

• $30M loss on debt extinguishment — expensive refinancing

• $102M short-term debt — needs servicing or refinancing in 2026

• Related-party transactions totaling ~$79M still embedded in operating costs

• No organic/acquired revenue breakdown provided

• Cash burn from operations was $63.1M — they need the December run-rate to sustain this without more capital

MY UPDATED SCORECARD:

✅ GAAP revenue beat — $46.8M vs $40M guide

✅ Cash position solid entering 2026

✅ H2 acceleration validated the hockey stick

✅ No equity dilution pledge for operations

✅ Earnings call held with Q&A

✅ 2026 guidance raised

⚠️ Audit opinion — awaiting full 20-F review

⚠️ Related-party details — need footnotes

❌ Organic vs acquired split — still missing

BOTTOM LINE: The narrative just got significantly harder to dismiss. $46.8M in audited GAAP revenue with a $19.4M December run-rate and $46.5M in deferred revenue is not a story anymore — it's a business generating real, recognizable cash flows. At a ~$1.1B market cap with $360M 2026 guidance, you're looking at roughly 3x forward revenue IF they execute.

The bear case isn't dead — the related-party transactions, debt load, and acquisition dependency remain real risks. But the goalposts I set yesterday? Most of them were met or exceeded.

I'm reading the full 20-F tonight. If the audit is clean and the footnotes don't reveal surprises, this stock has a credibility problem — but it's the market's credibility problem, not the company's.

Still long. More convicted than this morning.

$RZLV @realDanWagner @RezolveAi

MarketMaverick@DiaTSLAPLTR

$RZLV reports H2 and full year 2025 earnings Monday before the bell. This is the one that matters. After months of guidance, press releases, and promises — we finally get audited numbers. Here's what I'm watching: 1. Audited GAAP Revenue Management guided $40M+ for full year 2025. H1 was $6.3M. That means H2 needs to show ~$34M — a massive acceleration. December alone was guided at $17M+. Did it actually land? Show me the bridge. 2. Audit Opinion Clean and unqualified, or are there qualifications? This single line matters more than any number on the P&L. A going-concern flag or material weakness disclosure would be devastating. 3. Cash Position Post Reward They raised $250M in January at $4.00/share, then spent $230M on Reward weeks later. What's left? Working capital deficit was $71.1M as of June 2025. I need to see a credible liquidity runway. 4. ARR to GAAP Conversion The $209M ARR exit claim has been the bull case and the bear case simultaneously. Monday we find out how much of it converted to recognized revenue under ASC 606. The gap between ARR and GAAP is the credibility gap. 5. Related-Party Disclosures I'll be reading the footnotes carefully. The $93.9M in share based payments to DBLP Sea Cow and the Bluedot transaction details need full transparency in the annual filing. 6. Segment Breakdown With GroupBy, Crownpeak, and now Reward in the mix — how much revenue is organic vs. acquired? Even a high-level split would go a long way. What would make me more bullish: ✅ $40M+ GAAP confirmed with clean audit ✅ Clear cash runway through 2026 ✅ Evidence of organic growth beyond acquisitions ✅ A real earnings call with open Q&A — not just a press release What would concern me: 🚩 GAAP revenue materially below $40M 🚩 Audit qualifications or restatements 🚩 Cash burn rate suggesting near term dilution 🚩 No earnings call scheduled I've been covering this stock for months, engaged directly with the CEO @realDanWagner , and laid out my concerns publicly. Monday is where narrative meets reality. Long and watching. $RZLV @RezolveAi

English

@realDanWagner Crook release the audit and stop stealing from retail. Once ur auditor comes out we go to 1

English

How is Rezolve AI changing the way the world shops?

Our latest Annual Report is live, detailing our growth, our tech breakthroughs and our vision for an AI-first future in commerce.

Download the full report: investor.rezolve.com/static-files/6…

#love #RezolveAI #FutureOfRetail #AI #FinTech

English

@fundstrat @CNBCClosingBell @ScottWapnerCNBC @FundstratDirect @FundstratCap @BitMNR Tom pump $orbs. You are ruining your reputation with $bmnr and this. Deploy the cash into some other private company and make it run

English

Tune into @CNBCClosingBell at 3:35pm ET with ‘the Judge’ @ScottWapnerCNBC

- lots to discuss as the war moves into its 5th week

@FundstratDirect @FundstratCap

@BitMNR $BMNR

Fundstrat Direct@FundstratDirect

Don't miss @fundstrat's Tom Lee live on @CNBCClosingBell with @ScottWapnerCNBC at 3:35pm ET🔔

English

In case you missed it, this is what I am referring to 👇🏻

First Squawk@FirstSquawk

IRAN'S PRESIDENT PEZESHKIAN: WE'RE READY TO END WAR, BUT WANT GUARANTEES.

English

It is quite unbelievable we got to a point where global financial markets can swing wildly by trillions in value based on a misleading headline purposely crafted by one of the popular newsfeed accounts on X for the sole goal of engagement farming

English