Tamas retweetledi

After too many hours of research/DD to count, these are my Top 5 AI Stocks in the Top 5 AI Sectors to Invest in:

1. Neoclouds: The GPU & Compute landlords. Whoever owns the compute owns what every AI company on the earth needs to grow & succeed.

$NBIS - Nebius. Spun out of Yandex, rebuilt as a pure-play AI cloud. Microsoft and Meta committed billions in contracted backlog. The fastest growing neocloud on the board. My favorite pick as a long-term investment.

$CRWV - CoreWeave. The American-founded neocloud. SemiAnalysis rated this Neocloud in a class of it's own, which can not be understated. Deals with Anthropic, OpenAI, Meta, Perplexity, Google, Microsoft... the list goes on forever.

$HUT - Hut 8. Started as a bitcoin miner, pivoted hard into AI hosting and power infrastructure. Owns the power, not just the GPUs. They're landing deals left and right, definitely an underappreciated sleeper pick.

$APLD - Applied Digital. Same playbook. Former crypto miner now building purpose-designed AI data center campuses with long-term hyperscaler leases.

$CIFR - data center host for Anthropic's directly, purchased Google TPU v7 Ironwoods (400K units, ~$10B), backed by a 10-year, $3B+ Fluidstack hosting deal where Google guarantees $1.4B of lease obligations for a 5.4% equity stake. One of the only neocloud-adjacent names with real exposure to Google's silicon instead of pure Nvidia GPU rental.

2. Optical / Photonics:

Because every GPU is useless if it can't talk to the GPU next to it.

$CRDO - Credo. The connectivity layer inside every AI cluster. Active electrical cables and DSPs that scale with every rack hyperscalers deploy.

$LITE - Lumentum. Legacy telecom optics company that's become a core 800G/1.6T transceiver supplier for the AI buildout.

$ALAB - Astera Labs. Connectivity chips that solve the bottleneck between GPUs, memory, and storage. Pure-play AI infrastructure with almost no legacy drag.

$COHR - Coherent. Lasers, optical components, and transceivers spanning the entire photonics stack from datacom to industrial.

$MRVL - Marvell. Custom silicon and photonic fabric for hyperscalers. The company quietly inside more AI racks than people realize.

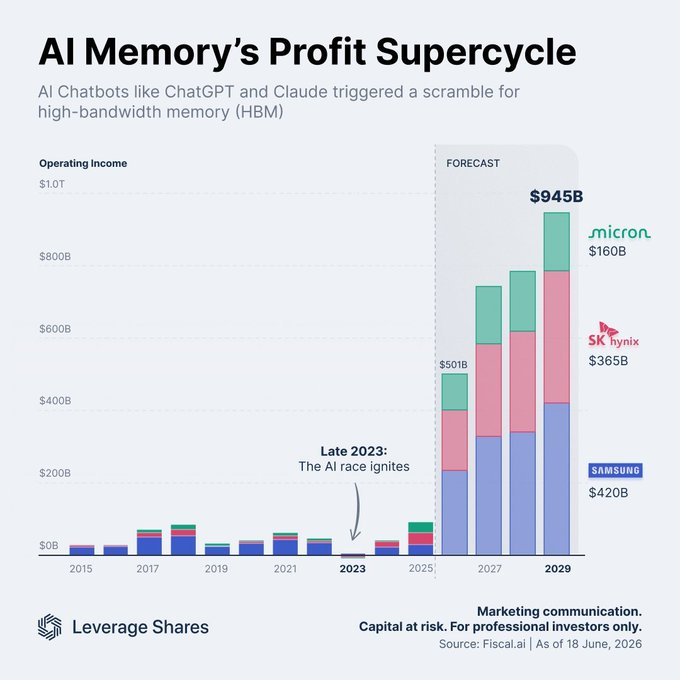

3. Memory:

The most cyclical, most violently mispriced sector in semis. HBM demand changed the entire setup.

$DRAM - DRAM ETF. One ticker, every important memory company on the planet, including South Korean companies like SK Hynix and Samsung Electronic, companies you CAN'T INVEST IN with most brokerages.

$SNDK - SanDisk. Spun off from Western Digital, now a pure-play NAND flash story riding the same supply tightness as everyone else in this sector.

$MU - Micron. One of three companies on Earth that makes HBM. The clearest direct line from AI buildout to memory revenue.

$WDC - Western Digital. Hard drive and enterprise storage demand riding the same data center capex wave as everything else on this list.

$STX - Seagate. The other half of the storage duopoly. Enterprise nearline drives are seeing the same supply crunch dynamics as memory.

4. Analog / Power Semis:

Unsexy. Necessary. Every data center, every EV, every robot needs power management silicon that doesn't get the AI premium yet:

$MXL - MaxLinear. Smaller-cap analog and mixed-signal play with infrastructure and data center exposure that's still flying under the radar.

$STM - STMicroelectronics. European chip giant spanning auto, industrial, and power semis. Way out of favor relative to its diversification.

$ON - ON Semiconductor. Power semis for EVs and industrial, now leaning harder into data center power delivery as a growth vector.

$VSH - Vishay. Passive components: resistors, capacitors, diodes. Boring until you realize literally everything electronic needs them.

$POWI - Power Integrations. High-voltage power conversion chips. Small cap, niche, and positioned for the power efficiency problem AI data centers haven't solved yet.

5. Physical AI / Robotics:

It's coming, soon, and the market is beginning to realize it.

$OUST - Ouster. Lidar for robotics, industrial, and autonomy. Consolidated the space after merging with Velodyne, now the survivor.

$VICR - Vicor. High-density power modules for robotics, AI servers, and defense. Power delivery at the component level, not the rack level.

$VPG - Vishay Precision Group. Precision sensors and strain gauges. The torque and force-sensing hardware that gives robots a sense of touch.

$AEVA - Aeva. 4D lidar with built-in velocity sensing. Smaller and earlier stage than the rest of this list, highest risk, highest ceiling.

$AMBA - Ambarella. Edge AI vision chips. Powers the cameras and perception systems inside cars, robots, and security infrastructure.

I believe a portfolio with these 25 names will severely outperform the market over the next few years. I have 7 figures throughout many of these names. These are all names I'm currently invested in, or plan on investing in in the near future.

None of this is financial advice.

English