Steve_Nicholas

6K posts

Steve_Nicholas

@Teddytwitt

Not interested in the politics of greed. We should strive for what is best for the community and look after the disadvantaged.

Sydney Katılım Nisan 2010

247 Takip Edilen327 Takipçiler

@EVCurveFuturist So no need to take the roof racks off then Chris!

English

Like my new sticker?

Runs on Aussie sunshine ☀️

No fuel stops. No price shocks. Just charge at home and drive.

This isn’t a drivetrain swap, it’s a system flip. From imported oil to rooftop energy.

Once the fleet scales, the economics break fast.

Cost always wins.

English

@WayneHines24470 Watch Chris Gale in the video link on this Solis web page.

solisminerals.com

English

Only +51% today!

TheArchitect@TheArchitect_HC

🚨 LITHIUM BACK ON THE MENU! Lithium Giant $PLS owns 5% of this junior asx explorer Solis Minerals $SLM $slm.ax who just acquired a Lithium project off of RioTinto $RIO This new project adjoins PLS own project in Brazil! Solis Minerals: 🔥 $12m Market Cap 💰 $4.2m Cash ✨ 262m Shares (very low) 💪 PLS 5% ownership #asx #lithium #mining #rareearths #australia #criticalminerals $rml $cxo $dtr $ltr

English

@WayneHines24470 I'll bet Dale is all over this. He mentioned at a shareholder meeting in Sydney about 12 months ago that #PLS were looking at further expansion of the resource in Brasil. Here, they now have a signed collaboration agreement with participation first right etc.

English

@wartranslated Who are "the SBU drones" - Ukranian or Russian?

English

There is another fire at the Russian port of Tuapse. SBU drones have once again attacked the port and the oil refinery there. The Russians had only just managed to extinguish the fire from the previous attack, and now the blaze has spread to at least 11 different locations.

English

Steve_Nicholas retweetledi

The continued easing of sanctions against Russia does not reflect the real situation in the war or in diplomacy and fuels the Russian leadership’s illusion that they can continue the war. This week alone, the Russians have launched over 2,360 attack drones, more than 1,320 guided aerial bombs, and nearly 60 missiles of various types at our cities and communities.

Every dollar paid for Russian oil is money for the war. More than 110 tankers from Moscow’s shadow fleet are currently at sea. On board are over 12 million tons of Russian oil, which, due to the easing of sanctions, can once again be sold without consequences. That is $10 billion – a resource that is directly converted into new strikes against Ukraine.

That is why it is important that Russian tankers are stopped, not allowed to deliver oil to ports. The aggressor’s oil exports must decrease, and Ukraine’s long-range sanctions continue to work toward that goal. I am grateful to every one of our warriors for their precision, and I thank all partners who are helping to increase pressure on Russia for this war.

English

Steve_Nicholas retweetledi

This was the moment that convinced me it was a staged event...

How else do you explain the flag being lowered perfectly into position, as if the entire scene had been frozen until the flag was in place for that ideal photograph?

English

Steve_Nicholas retweetledi

For the peasants among us, Grok explains: (Unfortunatley, formatting all over the place with cut & paste.)

Explain: Archaen greenstone belt Vs Proterozoic Belt

In short: Archean greenstone belts record the formation and stabilization of Earth's earliest continental crust through intense volcanism and deformation in a hotter world. Proterozoic belts record the maturation of that crust, with more stable interiors, thicker sedimentary accumulations, and collision-driven mountain-building similar to today. If you'd like details on a specific example (e.g., Abitibi vs. Belt Supergroup, or a particular orogen), mineral deposits, or tectonic models, let me know!

Archean greenstone belts and Proterozoic belts are both important Precambrian geological features, but they differ significantly in age, rock composition, tectonic setting, structure, and formation processes. These differences reflect the evolution of Earth's crust, mantle, and tectonic style from the hotter, more dynamic Archean Eon (4.0–2.5 billion years ago) to the cooler, more modern-style plate tectonics of the Proterozoic Eon (2.5–0.54 billion years ago). Archean Greenstone BeltsThese are the classic "granite-greenstone" terranes that dominate many Archean cratons (stable continental cores). They consist of elongated or irregular zones of metavolcanic and metasedimentary rocks (the "greenstones") surrounded or intruded by granitic/gneissic rocks. Rock types — Dominated by mafic to ultramafic volcanic rocks (basalts, often pillowed, and komatiites — high-Mg lavas unique to the hot Archean mantle). Felsic volcanics and volcaniclastic rocks increase upward in some sequences. Sediments (cherts, banded iron formations, minor clastics) are subordinate, often in upper parts. Low- to medium-grade metamorphism (greenschist to amphibolite facies) gives the characteristic green color from minerals like chlorite and actinolite.

Structure and setting — Typically synformal (boat- or keel-shaped), bounded by granitic domes or TTG (tonalite-trondhjemite-granodiorite) suites.

Deformation involves folding, faulting, and often vertical tectonics (sagduction or diapirism due to density contrasts). They are interpreted as remnants of ancient oceanic or back-arc-like basins squeezed between proto-continental fragments. Plate tectonics may have operated differently (hotter mantle, possibly more vertical motion or plume-related processes).

Age and examples — Mostly 3.5–2.6 Ga, with peaks around 2.7 Ga. Famous examples: Barberton (South Africa), Abitibi (Canada), Pilbara and Yilgarn (Australia), Isua (Greenland).

Economic importance — Host major gold, base metal, and iron deposits.

Key traits — High heat flow, komatiites common in lower sections, limited evidence of mature continental sources early on, dome-and-keel architecture.

Proterozoic Belts"Proterozoic belt" is a broader term. It can refer to: Proterozoic greenstone belts (less common, but exist).

Orogenic/mobile belts (fold-and-thrust belts formed by continental collisions or accretion).

Sedimentary basins like the Belt Supergroup (Mesoproterozoic, ~1.47–1.38 Ga), a thick package of mostly fine-grained clastic and carbonate rocks in western North America.

Proterozoic Greenstone BeltsThese resemble Archean ones but are rarer and show differences:Volcanics are more bimodal (basalt + rhyolite) or calc-alkaline, with fewer or no komatiites (mantle had cooled).

They often sit on older granite-gneiss basement or other greenstones.

Examples: Birrimian (~2.1 Ga, West Africa), Flin Flon (Canada), Pecos (New Mexico).

Proterozoic Orogenic/Mobile BeltsThese are linear to arcuate zones of deformed and metamorphosed rocks that often wrap around Archean cratons, recording continent-continent or arc-continent collisions.

Rock types — More diverse: metasediments (quartzites, shales, carbonates), metavolcanics, and abundant intrusive rocks. Higher-grade metamorphism in places.

Structure and setting — Clear evidence of modern-style plate tectonics: thrust faults, nappes, polarity (e.g., foreland basins), and paired metamorphic belts in some cases. They show crustal thickening, subduction signatures, and accretion.

Age — Mainly Paleoproterozoic (e.g., ~2.1–1.8 Ga) to Mesoproterozoic, with some later ones.

Examples — Trans-Hudson Orogen (Canada), various Pan-African belts, orogenic belts around the Superior or Kaapvaal cratons.

The Belt Supergroup (a Classic Proterozoic "Belt")This is a large, relatively undeformed to mildly deformed intracratonic sedimentary basin (not a typical orogenic belt). It consists of thick (up to 15–20 km) layers of siltstones, mudstones, sandstones, and carbonates, with some mafic intrusions. Deposited in a large basin possibly related to rifting within the supercontinent Nuna/Columbia. Exposed in Glacier National Park and surrounding areas; hosts important mineral deposits (copper, silver, lead-zinc).Key Differences: Archean Greenstone Belts vs. Proterozoic Belts Aspect Archean Greenstone BeltsProterozoic Belts (Greenstone or Orogenic) Proterozoic Sedimentary Belts (e.g., Belt Supergroup)Dominant Age3.5–2.6 Ga2.5–1.0 Ga (peaks ~2.1–1.8 Ga)~1.47–1.38 GaMain Rocks Mafic-ultramafic volcanics (komatiites common), minor sediments Bimodal/calc-alkaline volcanics + more sediments; orogenic: metasediments + intrusives Mostly fine clastics and carbonates; minor mafic sills Volcanism High-Mg komatiites, tholeiitic basalts Less ultramafic; more arc-like or bimodal Limited volcanism Tectonic Style Often vertical (dome-keel, sagduction); debated plate tectonics More horizontal (subduction, collision, thrusting) Intracratonic rifting/sagging; mild deformation Metamorphism Greenschist-amphibolite; low-moderate grade Variable, often higher in orogensLow grade (sub-greenschist to greenschist) Crustal Context Building early proto-cratons; limited mature crustAccretion around stable Archean cratons; modern plate tectonics evident On stable crust; thick basin fill Structure Synformal keels between granite domes Linear fold-thrust belts; polarity commonBroad basin; layered, relatively flat-lying Evidence of Plate Tectonics Weaker (no blueschists, limited ophiolites) Stronger (subduction signatures, collisions) Passive basin setting Summary of the Transition The Archean-Proterozoic boundary (~2.5 Ga) marks a shift from a hotter, more mafic/ultramafic-dominated crust with possibly plume- or vertical-dominated tectonics to one with stable cratons, widespread sedimentation on rigid lithosphere, and clearer modern-style plate tectonics (subduction, collision, rifting). Greenstone-style volcanism continued into the Proterozoic but declined, while orogenic belts and large sedimentary basins became prominent.geo.libretexts.org

33 web pages📷📷📷

English

Thank you mate. A lot of Chinas deposits are within a proteozic belt that spans through the middle of China (think Shenzhen, etc.). All of the world’s best deposits occur within archaen greenstone belts. The younger belts tend to produce shittier pegmatites (zoned, splattered,etc). So if a country has an archaen setting greenstone belts, there’s potential there.

English

Some random thoughts on some of the latest lithium news as a I sip my morning coffee.

CATL has brought in Chen Zinghe from Zijin as an advisor for it’s mining division. It’s basically CATL saying they are worried that they can’t find enough lithium to meet their massive growth. It’s impressive how fast CATL has grown and you’ve got to applaud the company.

However, I think they are leaving it a bit late as I touched on in an old post of mine (link below). I think they’ve underestimated just how difficult it is to find lithium deposits. Economical lithium deposits are rare and very hard to find. They could go years and find nothing. Zijin doesn’t have a great track record at finding deposits, which is rightly so, they are after all miners, not explorers.

And it’s not just Zijin. What was the last deposit that RIO found? Or BHP? Or FMG? The majors are terrible at exploration, despite the fact they have very large exploration budgets. Exploration isn’t just about having a big budget. A geologist working for a major for a wage in a cookie cutter position is going to be less hungry to find something than a prospector working for themselves for 0 dollars and funding early exploration themselves. Projects are largely found by individuals, they then get passed into exploration companies, which then get taken out by miners.

Basically every (~90%) current lithium mine and the majority of lithium resources (excluding a lot of the Canadian plays) have been mapped and known about for a 100+ years. Most of them were old tin and tantalum mines.

Adover, Kathleen Valley, Pilgangoora, Tabba Tabba, Bikitia, Manono, Greenbushes, Mt Marion, etc. were all discovered over 60 years ago, largely by individual prospectors.

During the last lithium boom, if you wanted to find lithium, you toggled on/georeferenced the occurrences of old tin and tantalum workings, pegged the ground, and explored off that. Those days are done. Those are our current lithium mines and resources.

So 100 + years of mapping and exploring has found the current mines and resources and we are still in a lithium deficit (spod currently at ~$US2400). I agree with @usuallyYJLee , there isn’t enough mapped lithium around to meet his 2030 bull case. Literally all of the Canadian plays would need to come online. So naturally sodium and other battery types will take a portion of the market for this fact alone.

Zijin aren’t explorers. They are miners. Huge difference. A lot of countries don’t understand exploration. The idea of putting capital into what could be seen as a gamble is something they don’t get. They are happy to pay a premium for a nice resource, but the idea of spending a fraction of what they pay for a resource on a “gamble” seems silly.

I personally think Zijin (and any major) will struggle to find more greenfields lithium. All the easy low hanging fruit deposits are gone. It’s now largely a drilling under cover game. Once you’ve dusted your first 4-5million on drilling, you start to think maybe it’s just easier to buy these things for a premium. Problem is there aren't really many options available. Exploration for lithium has been on a halt for several years and despite spod at a very healthy price of ~US$2400, it still hasn't picked up yet. Better get exploring soon or big trouble.

To finish, on a side note, $PLS just hit an all time high! Cheers for reading!

English

PM Carney stated "Muslim values are Canadian values". If you disagree, under Bill C-9, racism and hate speech are now crimes.

Leo Pier@Leo_Pier_

Muslim father tries to honor-kill his daughter with a hammer in Quebec. These are "Canadian values." If you disagree, you're racist.

English

Carl told me back when Dale H was buying PLS at the $1.34 mark, "he has no idea what is happening" and repeated his chant of 'research = bad, follow my charts = good' mantra and handing out Kool Aid to his followers. He promptly blocked me as well. That $1.34 investment is now up 351% and DH bought just over $1m worth.

English

English

@zempheth @sparkes_dwayne CATL were invested in #PLS but they let it go. Ganfeng and POSCO are still invested.

English

simply perfection, from @sparkes_dwayne. And to top it off, we have the recent $4.4Bn capital injection from CATL into mining, much of which will find its way into lithium projects

scmp.com/business/china…

bloomberg.com/news/articles/…

Dwayne Sparkes@sparkes_dwayne

Some random thoughts on some of the latest lithium news as a I sip my morning coffee. CATL has brought in Chen Zinghe from Zijin as an advisor for it’s mining division. It’s basically CATL saying they are worried that they can’t find enough lithium to meet their massive growth. It’s impressive how fast CATL has grown and you’ve got to applaud the company. However, I think they are leaving it a bit late as I touched on in an old post of mine (link below). I think they’ve underestimated just how difficult it is to find lithium deposits. Economical lithium deposits are rare and very hard to find. They could go years and find nothing. Zijin doesn’t have a great track record at finding deposits, which is rightly so, they are after all miners, not explorers. And it’s not just Zijin. What was the last deposit that RIO found? Or BHP? Or FMG? The majors are terrible at exploration, despite the fact they have very large exploration budgets. Exploration isn’t just about having a big budget. A geologist working for a major for a wage in a cookie cutter position is going to be less hungry to find something than a prospector working for themselves for 0 dollars and funding early exploration themselves. Projects are largely found by individuals, they then get passed into exploration companies, which then get taken out by miners. Basically every (~90%) current lithium mine and the majority of lithium resources (excluding a lot of the Canadian plays) have been mapped and known about for a 100+ years. Most of them were old tin and tantalum mines. Adover, Kathleen Valley, Pilgangoora, Tabba Tabba, Bikitia, Manono, Greenbushes, Mt Marion, etc. were all discovered over 60 years ago, largely by individual prospectors. During the last lithium boom, if you wanted to find lithium, you toggled on/georeferenced the occurrences of old tin and tantalum workings, pegged the ground, and explored off that. Those days are done. Those are our current lithium mines and resources. So 100 + years of mapping and exploring has found the current mines and resources and we are still in a lithium deficit (spod currently at ~$US2400). I agree with @usuallyYJLee , there isn’t enough mapped lithium around to meet his 2030 bull case. Literally all of the Canadian plays would need to come online. So naturally sodium and other battery types will take a portion of the market for this fact alone. Zijin aren’t explorers. They are miners. Huge difference. A lot of countries don’t understand exploration. The idea of putting capital into what could be seen as a gamble is something they don’t get. They are happy to pay a premium for a nice resource, but the idea of spending a fraction of what they pay for a resource on a “gamble” seems silly. I personally think Zijin (and any major) will struggle to find more greenfields lithium. All the easy low hanging fruit deposits are gone. It’s now largely a drilling under cover game. Once you’ve dusted your first 4-5million on drilling, you start to think maybe it’s just easier to buy these things for a premium. Problem is there aren't really many options available. Exploration for lithium has been on a halt for several years and despite spod at a very healthy price of ~US$2400, it still hasn't picked up yet. Better get exploring soon or big trouble. To finish, on a side note, $PLS just hit an all time high! Cheers for reading!

English

@zempheth Well their Dec quarterly is coming up next Friday and it's difficult to find anything negative about the company's progress and direction. A few JV's & proposals going on in the background.

English

@GreenOriginInv @EVCurveFuturist The $6.14 PLS buyers were brave - but maybe not.

English

Been a minute since I’ve posted on #lithium…

LCE price showing a healthy trend + $PLS just printed a new ATH.

This is where quality gets repriced, top-down.

Tier 1: $LTR $SGML $SQM $MIN $RIO $IGO

Tier 2: $ELV $CXO

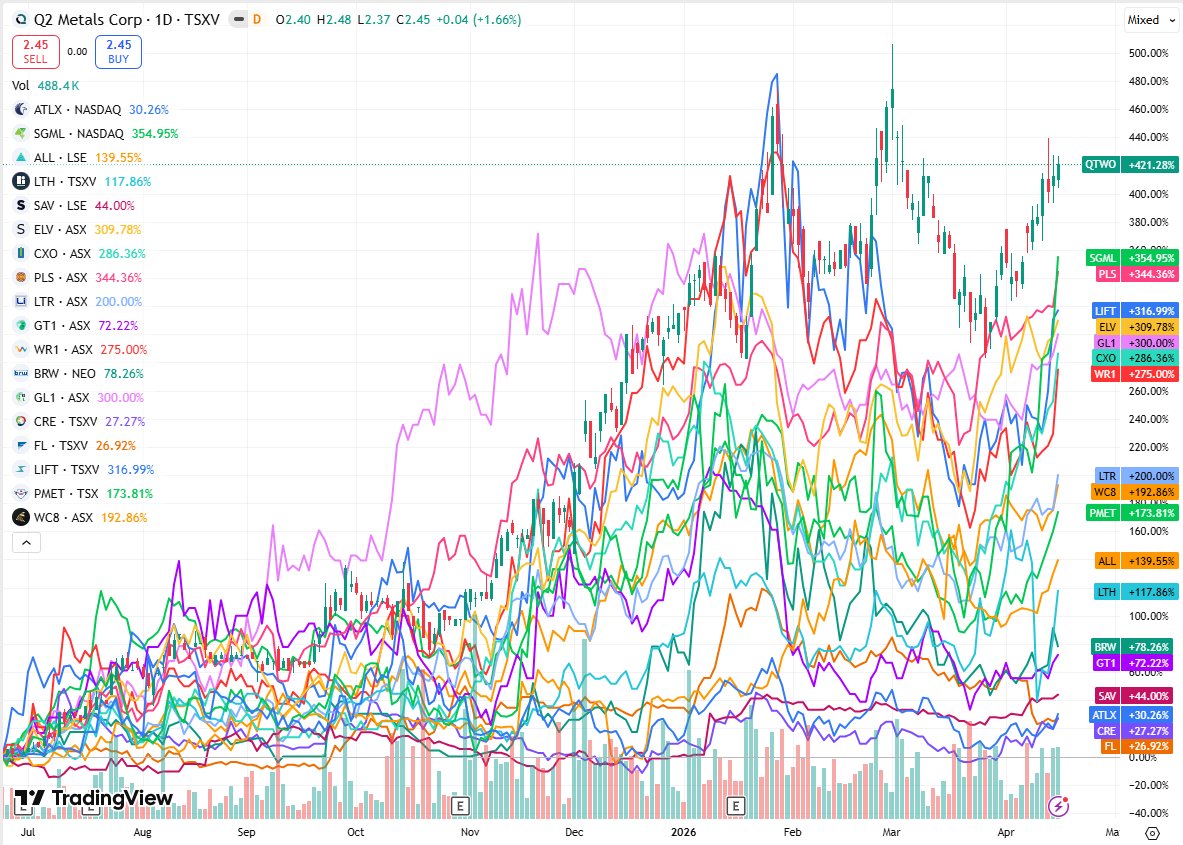

Next wave: #WC8 $PMT #WR1 $LIFF $GLN #A11 & my pick $QTWO

Cycle turning. Pay attention.

What’s changed isn’t just price, it’s the drivers. We’ve shifted from oversupply narrative → demand shock reality.

Oil volatility is back, and this time it accelerates electrification, not delays it. Every spike strengthens EV + storage economics.

China is doubling down: EV exports rising, charging scaling, grid storage ramping. That’s not forecast demand, that’s locked-in.

Policy is now pushing it harder. Countries introducing ICE taxes, removing fuel subsidies, and tilting economics toward EVs, renewables and storage. This isn’t optional demand anymore, it’s being engineered.

And it’s no longer just passenger cars. Trucking is ramping fast, shipping is starting to electrify, buses already flipped in China. Entire transport segments are locking in battery demand.

Supply? Not as flexible as expected. Delays, capital discipline, and constraints like Zimbabwe tightening exports are squeezing the system.

This is how cycles turn:

Price bottoms → demand builds → sentiment lags → price moves first → fundamentals get rediscovered.

Lithium isn’t just a commodity here. It’s a bottleneck in a system being rebuilt in real time.

That’s why quality moves first.

English

@EVCurveFuturist Well if the Camry is dragging two powertrains along for the ride, what can they expect?

English

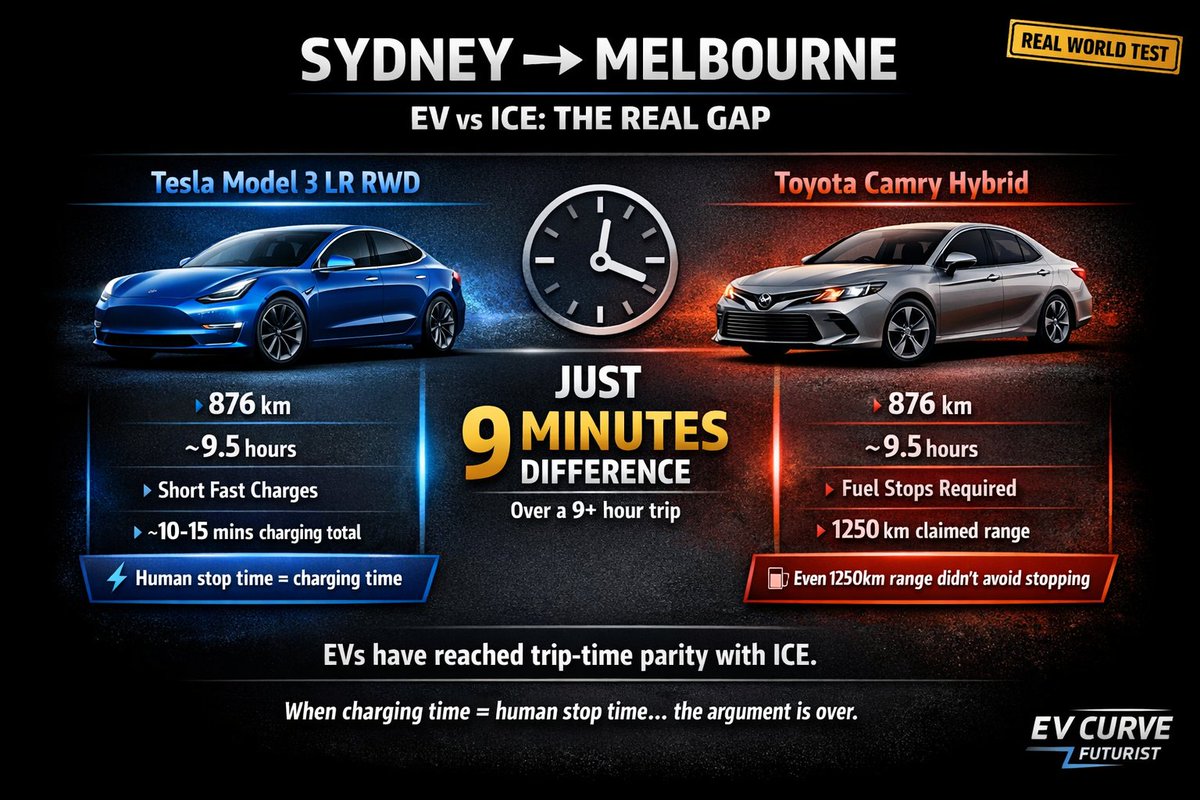

The guys at Chasing Cars did a great 866km Sydney→Melbourne test: Tesla Model 3 LR vs Camry Hybrid.

Result? Just 9 minutes in it over ~9.5 hours… and the Camry still needed a fuel stop.

EVs have hit trip-time parity. “Charging takes too long” is a 2020 argument. youtube.com/watch?v=JBK407…

YouTube

English

@agroasx Yes but Dale said they were not looking at acquisitions at the Dec quarterly brief - we get another update next Friday 9am AEST

English