Sabitlenmiş Tweet

Rocky Chartz

1.5K posts

Rocky Chartz

@TheCryptoRocky

📍NYC | Full-time Trader & Investor | Former Economist | Navigating markets through macro events, policy shifts & long-term opportunities

Decentralized Katılım Haziran 2021

253 Takip Edilen133 Takipçiler

It's wild to me more people don't talk about this Dutch company. $ASML will be a $3000 stock by 2027.

100% return in 1 year, not bad?

English

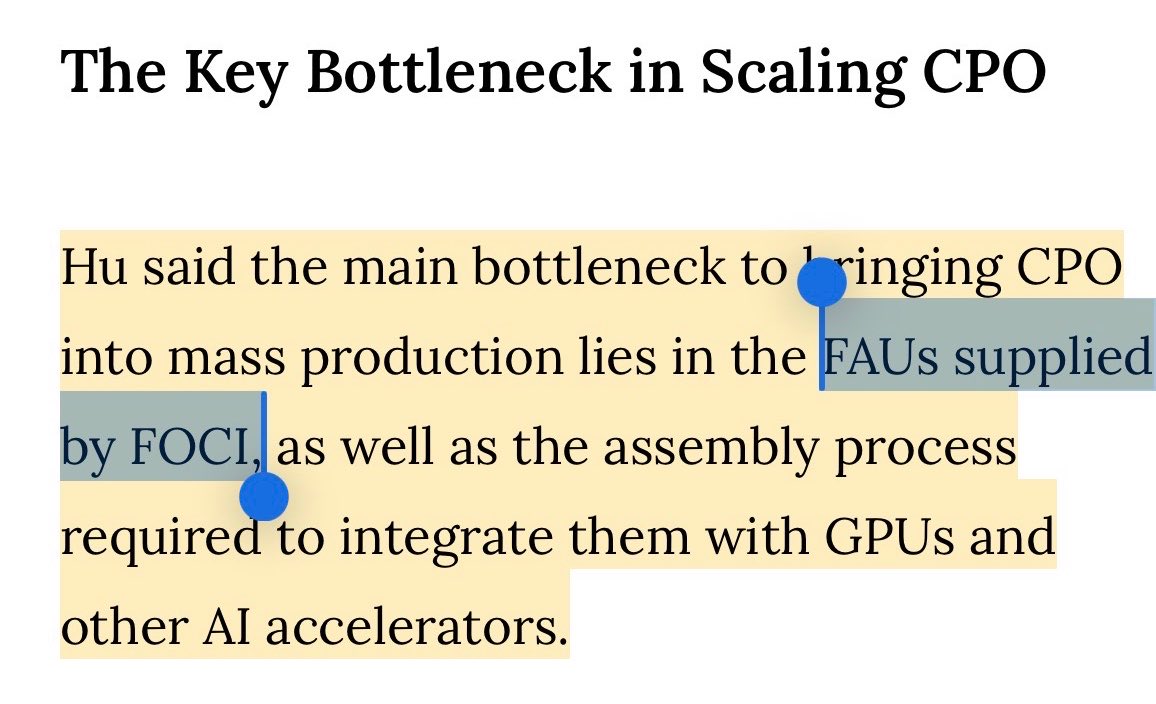

Honestly I’m expecting FOCI (3363) to blow away projections over next two years.

It’s a pretty high conviction position for me medium term at this level.

Since they’re expected to be the leading supplier to $NVDA and $TSM and get frequently cited as a bottleneck for that $91B+ 2028 CPO TAM (GS).

Insane how it’s $3B MC as a critical CPO bottleneck required for scale, while LightWave Logic literally has around the same valuation at $2.7B in development stage.

Soyunce@soyunce_

@aleabitoreddit This is actually very interesting, their forecast EPS for 2028 is 47 TWD, which give them a PE OF 18, this is insane! Good find!

English

@aleabitoreddit No other news on alrib partnership with Google?

English

@Bluntz_Capital As a trader yes, as an investor I’m not touching Tesla. Forward pe of 200x is outrageous for a company that size.

English

“Leading” Glass Substrate players that were name dropped if you’re curious:

• $LPK — TGV Equipment

• $GLW — Glass Materials

• $ASGLY (5201 T)— Glass Materials

• $NIDGY (5214 T) — Glass Materials

• $LRCX — Etching Systems

• $DSCSY (6146 T)— Dicing Equipment

• $SMHSF — Bonding Systems

• $ONTO — Inspection Tools

• $KLAC — Inspection Tools

Fun to see the stuff I’ve called out early in the year like LPK at ~$150m MC get mentioned as a critical player by Trendforce and others.

English

@aleabitoreddit @Matej91030183 $ASML has a monopoly on the machines used to build chips used for AI?

English

For me, probably until start of H2 2027.

I don't like long term holding equipment sellers like $ASML, $AIXA, even $TOWA etc.. Monopolies are usually exceptions since they retain valuations + keep going higher.

But they mainly benefit from the start-middle of cycles, then fall off until the next cycle begins. But now's usually a good time before the GCS ramp.

English

$LPK up 80% in the last two weeks. Not too shabby at ~$687M MC?

It's probably one of the cleaner ways to play the next Glass Substrate supercycle.

50-100 machines per customer at scale, with "start of 2027 as mass production" across likely $INTC, $GLW, SKC, and others (since they captured ~80% of the major players).

Maybe ~€2M average per machine.

€400M–€1B+ across just 5 players in 2027 (could be more)? Since they basically supply to everyone as a chokepoint. Off ~67.6% blended gross margins.

Seems promising for volume ramp wait time.

Serenity@aleabitoreddit

People nonstop ask me about $LPKK / $LPK for my opinion Yes, I mentioned they're like a chokepoint for glass core substrates for LIDE (laser induced deep etching) way back when. Biggest known partner is $ONTO (LIDE with Onto metrology for glass core mass production). Then as for market share: "more than 80% of customers among major global players have selected LPKF equipment" for process validation. So that probably includes: - Samsung Electronics/Electro-Mechanics - $INTC (Receives a Major Order from a Leading Chip Manufacturer... installed a first LIDE system at the beginning of 2020... now ordered further LIDE systems to start volume production) - SKC (Absolics) - $GLW, AGC, Schott. - Nippon electric glass. Of course this is evaluation, so that 80% could be lower in actual ramp. As for some personal FWD P/E calculations: - 2027: ~11-12.5x and ~7.8x for 2028, which looks very compelling. - Total Cash: ~€10.0M, debt was around ~€3.0M. debt to equity: ~3.8% So very clean-asset light balance sheet, no dilution overhang like $SHMD. ~$362m MC, conclusion: great upside long imo, hard to see institutions not buying this name down the road. Even if the 80% of players managed to design another way, even a fraction would probably be very material to the MC. It was probably a bit early few months ago, but glass core roadmaps have been speeding up like CPO. Disclosure: I do have positions. This are just my thoughts. People on X did their homework.

English

@aleabitoreddit Is it really that certain that institutions will have to own this?

English

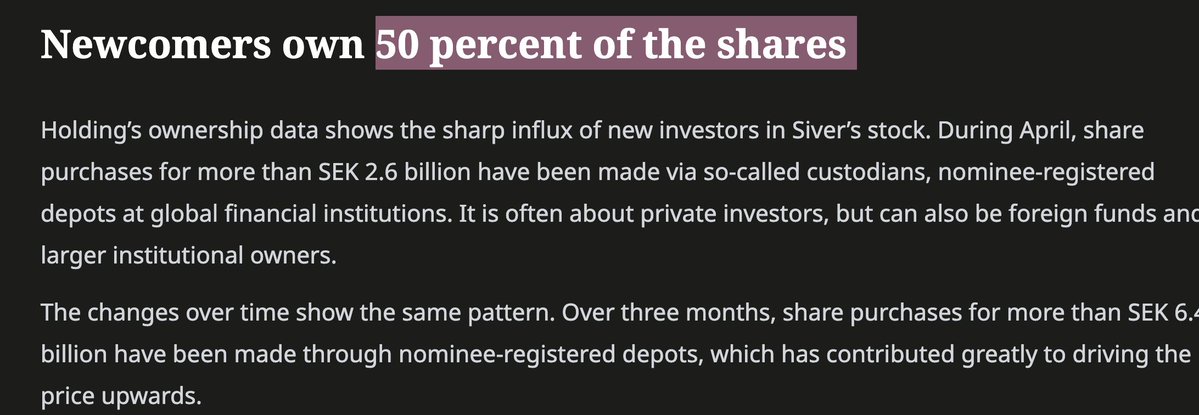

The US/West now controls majority of the shares of $SIVE.

With Goldman Sachs/JP Morgan/Morgan Stanley and other US institutions entering.

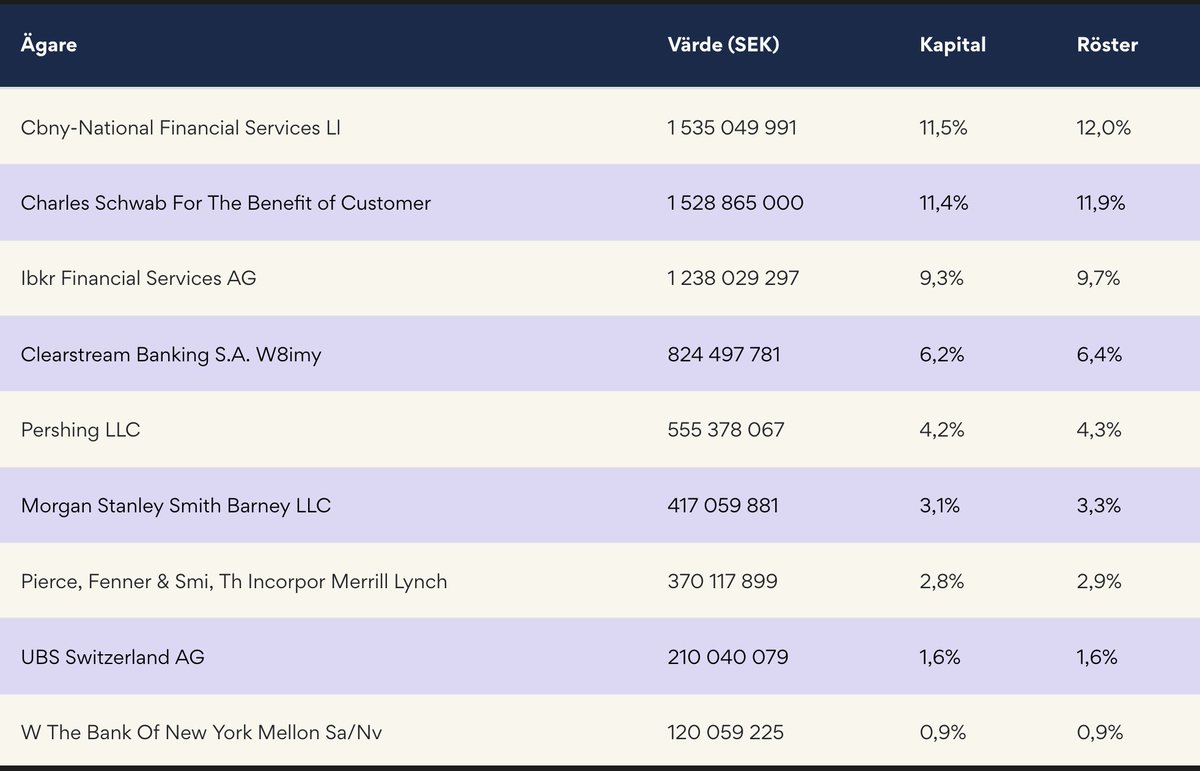

US/West 46.8%:

- Fidelity: 11.5% (retail)

- Charles Schawb: 11.4% (retail)

- $IBKR: 9.3% (primarily retail)

- BNY Mellon: 4.2% (retail)

- Morgan Stanley Smith Barney: 3.1% (Retail/Wealth management)

-Bank of America: 2.8% (retail/Wealth management)

- BNY Mellon: .9% (institutional)

- Morgan Stanley Client Assets: .7% (institutional)

- Bank of New York Mellon: .5% (institution)

- JP Morgan: .5% (institutional)

- J.P. Morgan Securities Plc: .4% (institutional)

- Citibank New York: .3% (institutional)

- JP Morgan SE: .2% (institutional)

- Morgan Stanley: .2% (institutional)

- JP Morgan Securities: .2% (institutional)

- BoFA Securities: .2% (institutional)

- Goldman Sachs: .2% (institutional)

- Goldman Sachs International: .1% (institutional)

- Cbny-Rja-Client Asset - .1% (retail/wealth)

Large % now owned US retail shareholders (eg. $IBKR on behalf of clients, probably majority retail some institutions).

The new but smaller JP Morgan Goldman Sachs, and Citibank % positions are likely hedge funds or other institutions trying to build positions.

Europe & Switzerland: 11.3%

- Clearstream: 6.2%

- UBS Switzerland: 1.6%

- Six SIS: 0.8%

- Euroclear Bank: 0.8%

- Saxo Bank: 0.6%

- BNP Paribas: 0.6%

- Caceis Bank / Intesa San Paolo: 0.2% each

- KBC / LGT / Julius Baer: 0.1% each

Swedish ~8.49%:

Försäkringsaktiebolaget Avanza Pension - 4.76%

Nordnet Pensionsförsäkring - 2.73%

Skandinaviska Enskilda - .2%

SEB Life International - .1%

Nordea Bank Abp - 0.7%

Canada/UK/Middle East ~.6%:

First Intl Bank of Israel - .3%

Royal Bank of Canada - .1%

Royal Bank of Canada - .1%

HSBC - .1%

A special thank you to the Swedish Media doing the work of US institutions:

The West now has ~58.7% ownership. Swedish is now down to 8.49% due to local media.

I wonder if they realized what they've done now scaring off local investors now that it's changed hands to US institutions/investors?

The West have now acquired majority of the float before the CPO supercycle.

You can also start to see US institutions like JP Morgan or Goldman Sachs building start positions (on behalf of institutional investors), probably off of US retail taking profits. This is likely after $SIVE reached a certain MC threshold for fund mandates.

But a large % of it is still owned by US retail on places like $IBKR and Fidelity. (this is what I call frontrunning the institutions)

TLDR:

$SIVE went from majority:

-> Swedish retail ownership

-> US retail ownership

-> gradual US Institution ownership as US retail takes profit or sells (if they figure out a way to scare off US retail like the Swedish media did).

English

@jessicatuga Es burra que doi, desperdício de espaço. Fica calada que ficas melhor

Português

PORTUGUESES ATENÇÃO!

Tudo a votar em Israel na terça!

A eurovisão vai ser na RTP e Israel participa na mesma semi final que Portugal!

Vamos dar a pontuação máxima do público a Israel como nos últimos anos?♥️🇮🇱

Conto convosco! FORÇA ISRAEL! Portugal está com vocês. #eurovision

Giannis Argyriou 🇬🇷🇨🇾🇮🇱🇺🇦@giannisargyriou

🇬🇷Στον Πρώτο Ημιτελικό ψηφίζουμε🇮🇱 #Eurovision #EurovisionGR #Eurovision2026 @IsraelinGreece

Português

Rocky Chartz retweetledi

Juízes chumbam a lei que permite expulsar estrangeiros ilegais porque os tribunais 'ficariam enterrados' em recursos.

Enquanto isso, entraram quase 2 milhões de imigrantes em poucos anos e o sistema judicial aguenta tudo… menos devolver quem não devia estar cá.

Protegem o direito dos ilegais a ficarem, mas não protegem os portugueses de casas caras, filas no SNS, escolas sobrecarregadas e criminalidade importada.

É um desrespeito total aos portugueses que escolheram esta mudança.

Eles defendem a 'democracia'… desde que não inclua o direito dos portugueses a terem o seu país de volta.

Português

So if Iran didn’t do it

I WONDER who did

Who wants the war to continue?

Wall St Engine@wallstengine

SENIOR IRAN MILITARY OFFICIAL: IRAN HAD NO PLANS TO TARGET THE UAE: IRIB NEWS

English

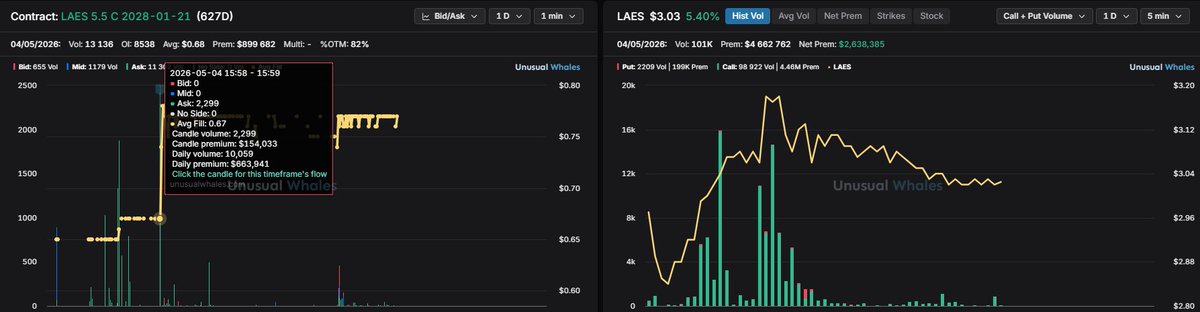

@ACInvestorBlog Curioso que mencione laes, tenho comprado muito disto

Português

Rocky Chartz retweetledi

The Portuguese flag's aura loss is shameful.

Tasteful white and blue replaced by the "our nation first came to be in the 20th century" color scheme

English

@thinklikekai @aleabitoreddit Why don’t you ask ai to do that for you lol

English

Can you start making these posts in a way where I can share them to my friends that don’t know shit about stocks

It’s so fckin hard to then explain all that to them as well

Whatever you’re promoting just add “make it simple to a point where a grandmother and a 5 year old both can understand”

English

Just in case you’re wondering why I’m so bullish on CPO.

Like $SIVE (Lasers), Shunsin (Packaging), MSSCorps (Yields), Win Semi / $TSEM (Foundry).

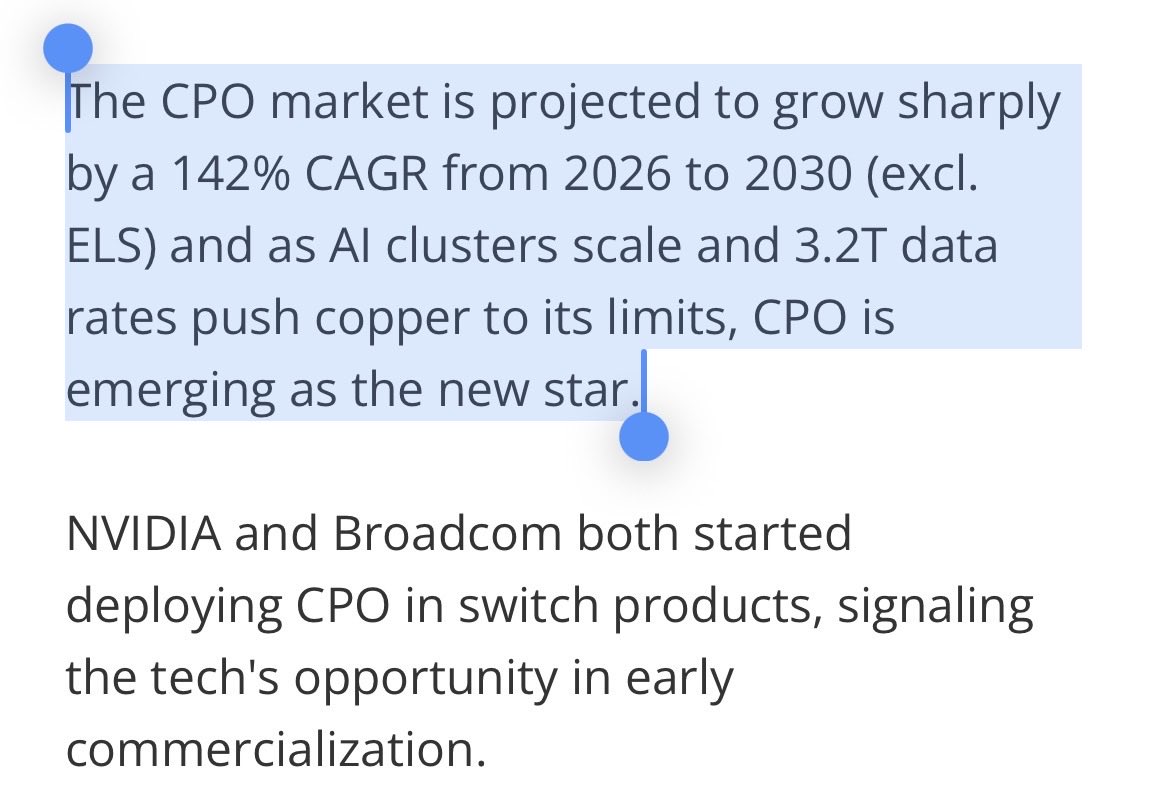

“The CPO market is projected to grow sharply by a 142% CAGR from 2026 to 2030 (excl. ELS)”

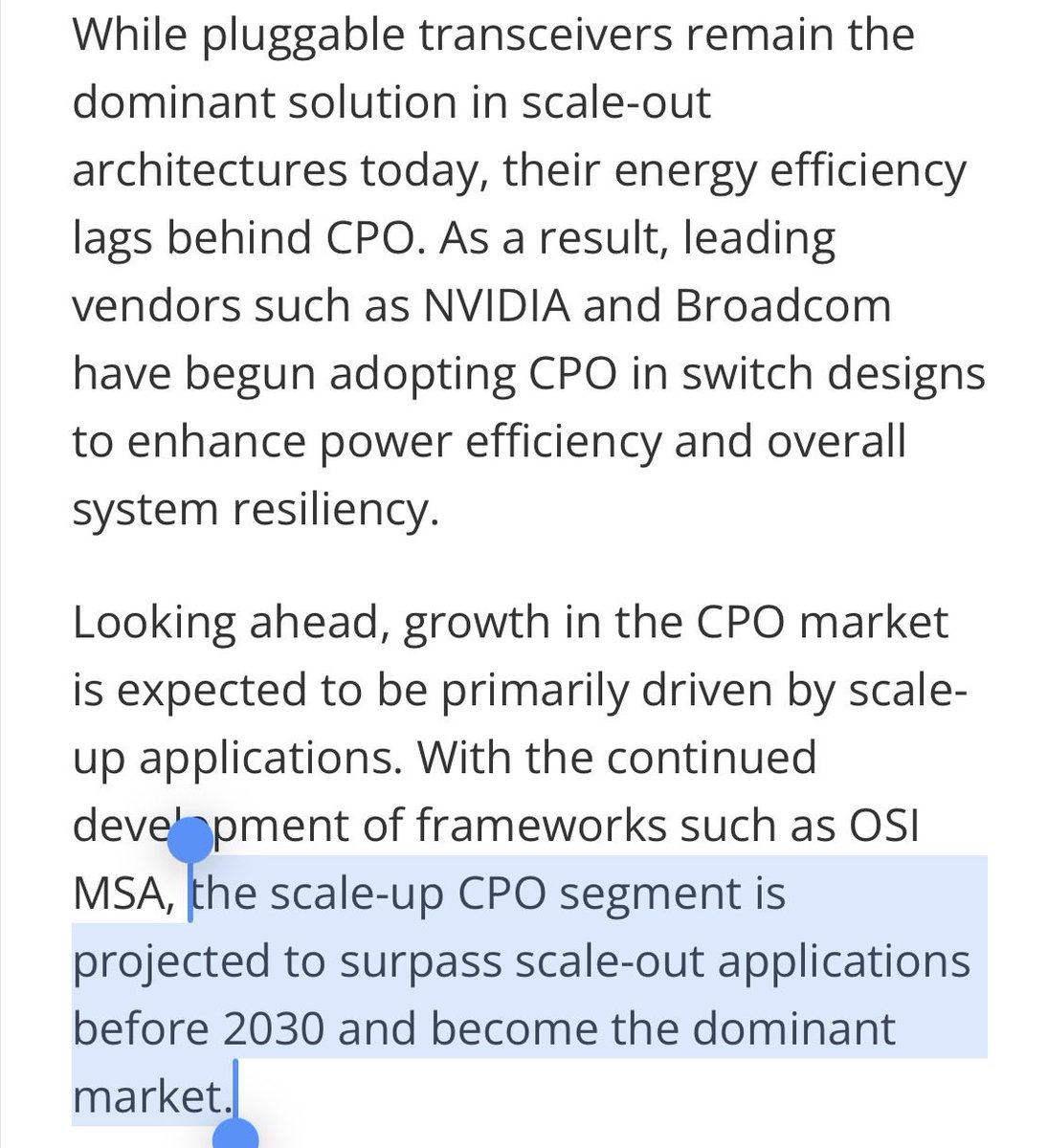

“The scale-up CPO segment is projected to surpass scale-out applications before 2030 and become the dominant market.

You have almost parabolic growth over the next few years.

With many players like Sivers having no material exposure to previous 800g pluggable optics but are the bleeding edge leaders of CPO as the laser supplier.

This is one of the best and earliest opportunities of the next optical supercycle for an architecture driven by $NVDA and $AVGO.

English

New opinion piece for #teamshardi subscribers drops on Monday

No one beats our team and this sub... NO ONE

#teamshardi

Subscribe today on @X... learn how to fish

English

@D_Tarczynski Sad to see other European governments are too corrupt/ incompetent to implement this measure, especially when we’ve been stating the declining birth rates being a major issue for decades now

English

@aleabitoreddit I thought you’d mention riber since it hasn’t gone up that much yet

English

As for 3x brrrs these levels:

1. $SIVE

2. MSSCORP (6830)

3. Auros (322310)

Are my best guesses. Here's my thought process:

1. $SIVE: I genuinely do see them being $10B+ next year, they're the literal bleeding edge for CPO lasers alongside $LITE and $COHR.

At a $1.3B MC... For likely mapping:

Photonics: $AMD CPO, $MRVL Celestial CPO, $JBL 1.6T, Lightmatter, Ayar, ALChip, GUC, O-Net (ELS), $POET.

For Space + Defense: Golden Dome via $YSS, $RTX / $ERIC / Bae Systems.

Silicon Photonics: $AAPL (Apple Watches).

This is just a stupid amount of customers and it's still increasing.

They can always TAM expansion downstream through IP acquisitions or vertically integrate to speedrun $LITE's $60B MC one day once they get more funding.

2. MSSCORP (6830): CPO monopoly over inspection at ~$1.2B.

100% monopoly over CPO yields, $TSM, $AMAT, $NVDA, $LCRX, $INTC, and others are all likely customers.

"The company’s goal is to seize a 90 percent share of the CPO inspection market"

This basically means 100%, they just don't want antitrust. If they defend their monopoly and CPO ramps, can easily see this worth ~$5B-$9B from $1.2B

3. Auros (322310): Samsung / SK Hynix supplier at ~$210M for Hybrid Bonding Metrology.

Basically pure play on two products:

-> HBM4 / HBM4e / HBM5 cycles, that $KLA had a monoply over for IR metrology.

---> Getting qualified now likely in Samsung factories, H2 volume ramp est. Sk Hynix likely qualifying too when they upgrade to hybrid bonding.

-> Thin-film thickness measurement.

---> Getting qualified now, with "major domestic chipmaker" (either Samsung/Sk hynix), targets mass supply this year.

They've been developing for the past decade, only to volume ramp two products from years of qualification H2 this year.

Seems extremely likely to 3x to $630M if they switch to volume ramp, feels like an undiscovered gem in the Korean market?

Of course, not sure how they play out and this is all speculative but high confidence supply chain mapping.

But off the top of my head these three that I own are the most likely ones at this level.

TheNewAL 🌾@Mellokhai

@aleabitoreddit Stay with us and Give us some more x3 brrrrrr

English