Sabitlenmiş Tweet

The Dial Macro

38 posts

@TheDialMacro

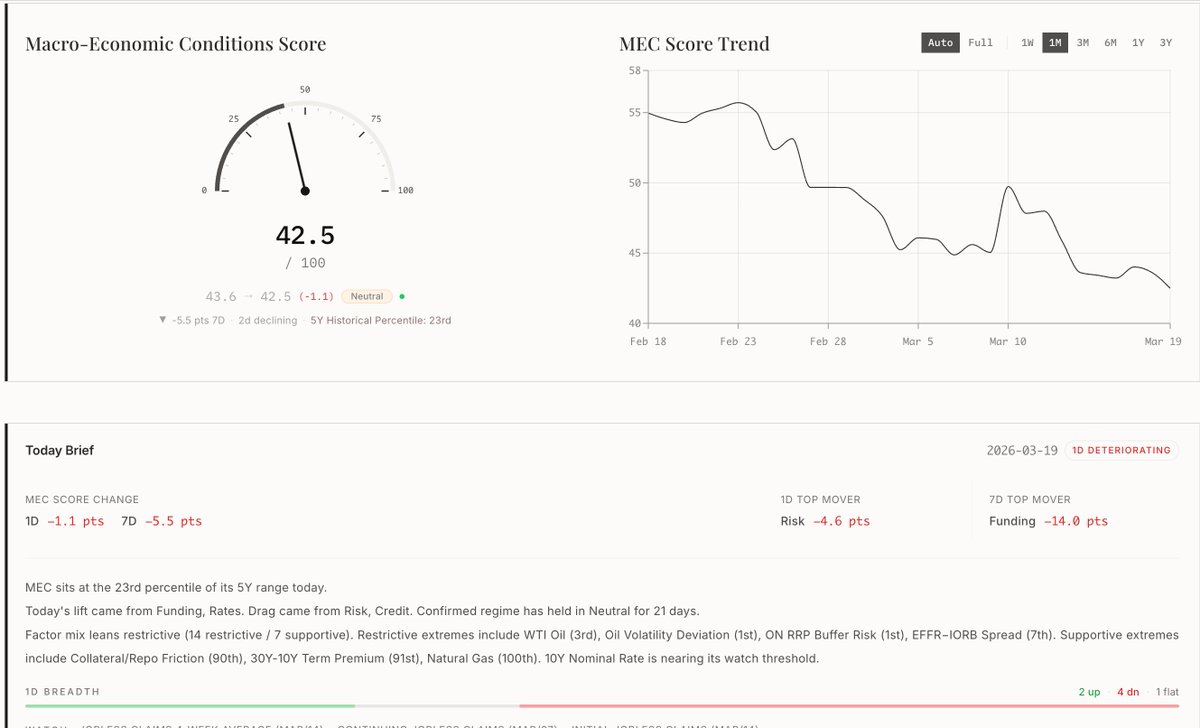

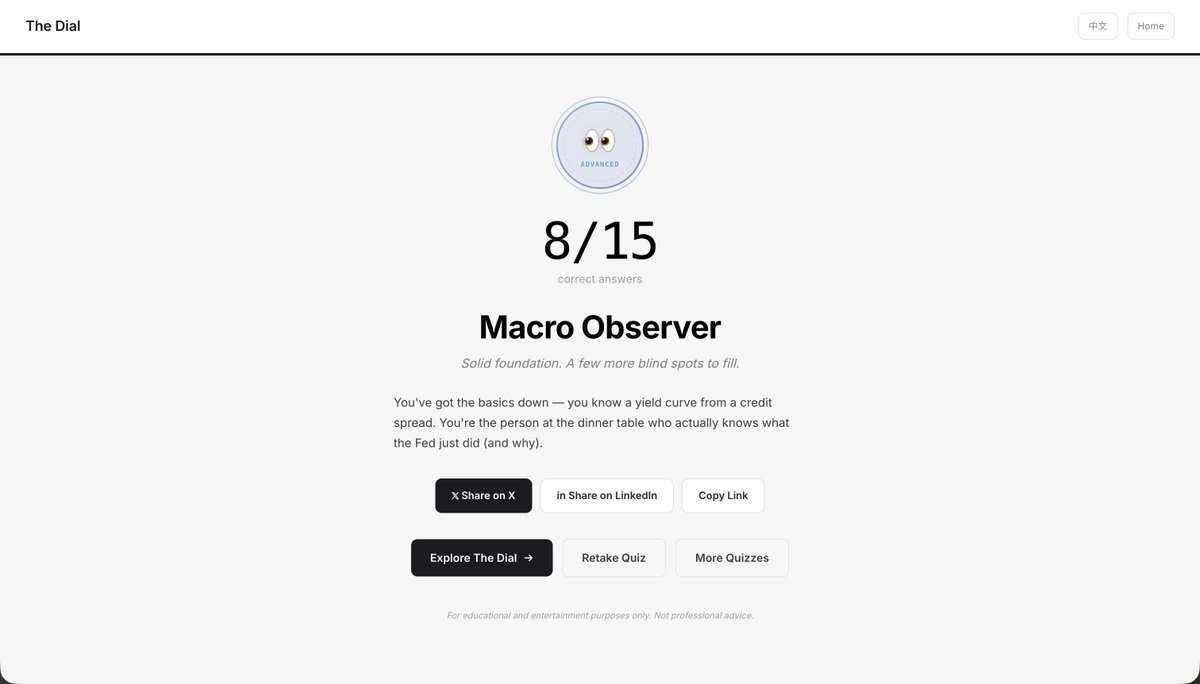

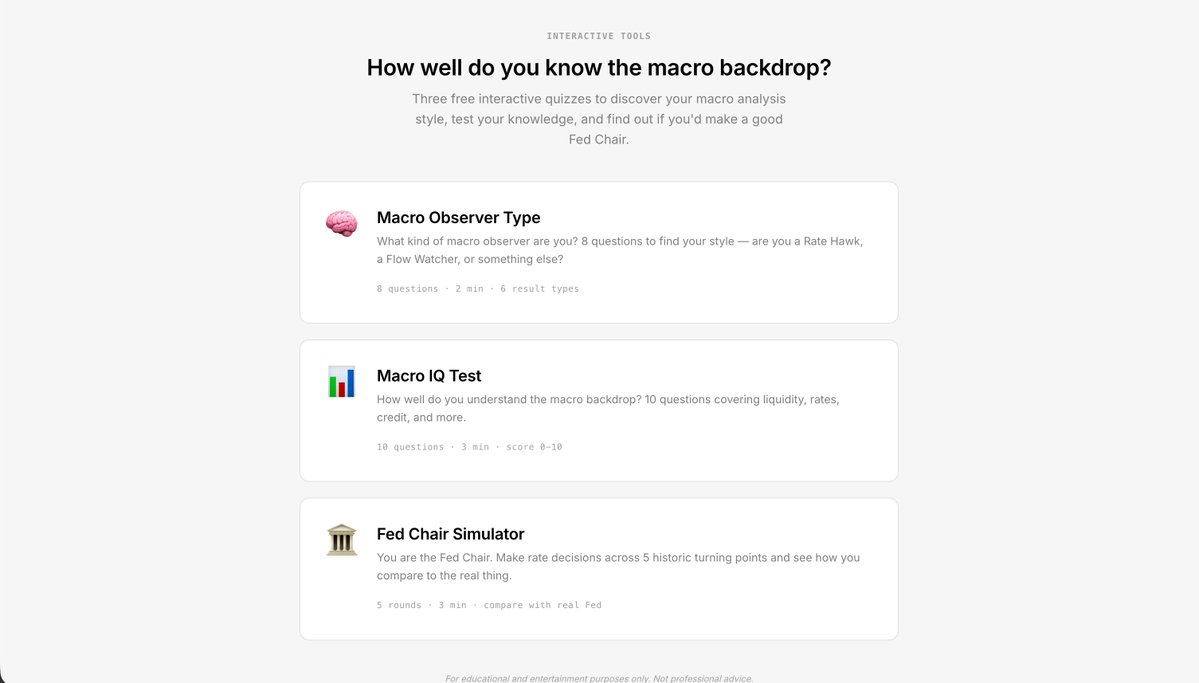

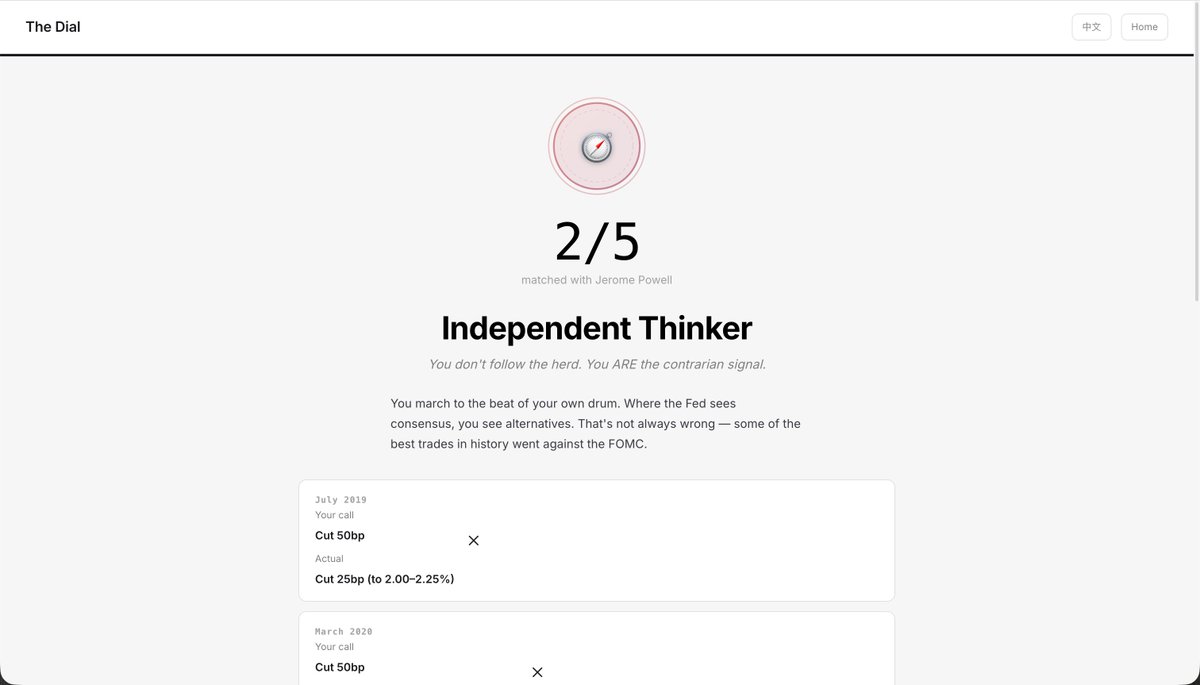

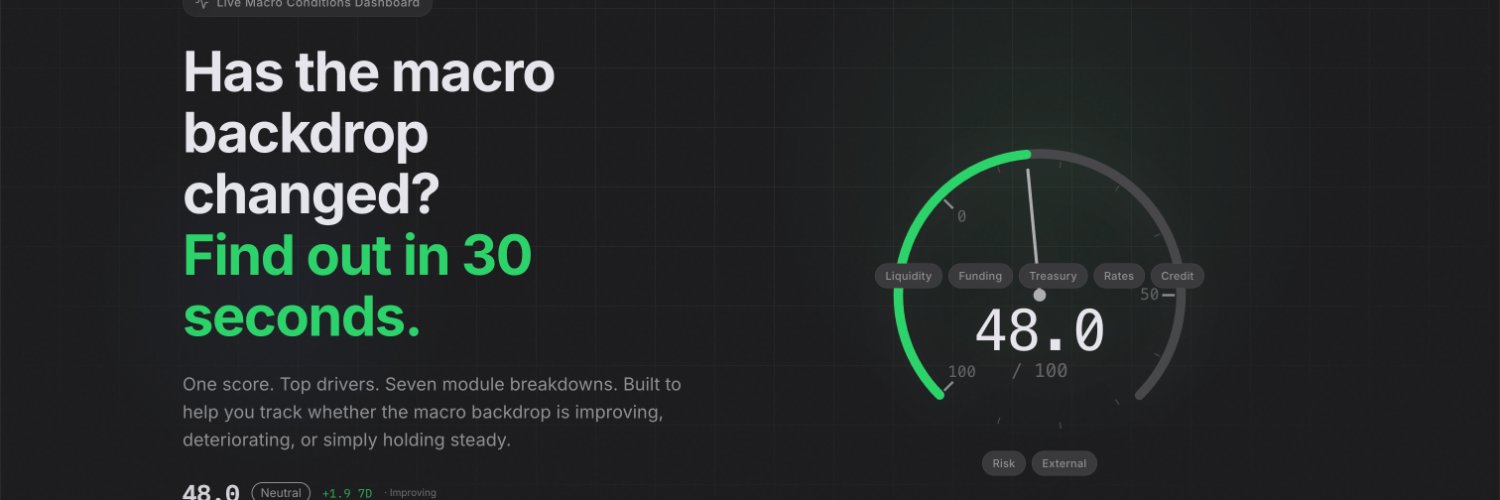

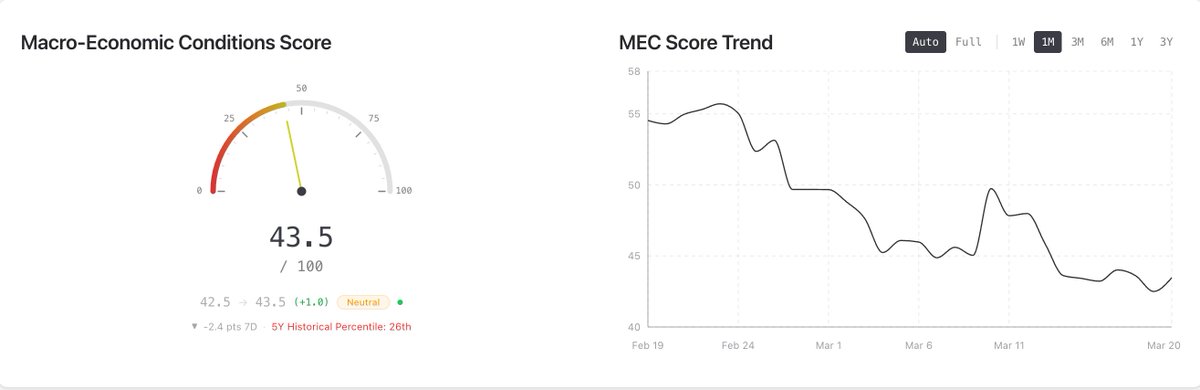

Has the macro backdrop changed? Find out in 30 seconds. 47 factors → 7 modules → 1 score. Updated daily. Free. 👀3 macro tests https://t.co/Hn36cFCWhy

Everything you need to know about investing in one image.

Gold is crashing. Silver is crashing. Crypto is crashing. Stocks are crashing. The dollar is crashing. Real talk what should we buy now?