Sabitlenmiş Tweet

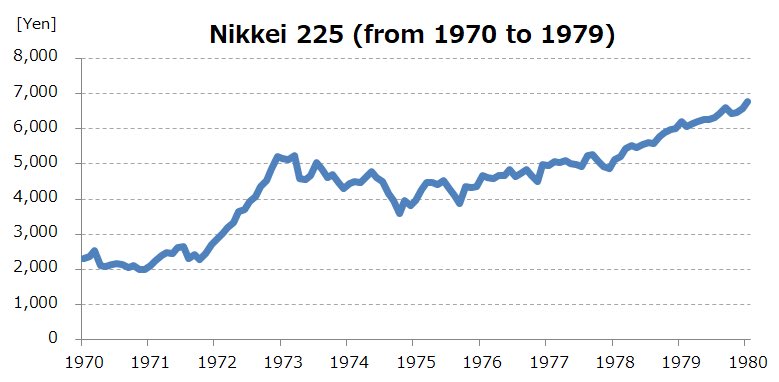

Japan’s Stock Market was up over 100% in 1972. The USA right now has a remarkably similar setup to Japan in the 70s. This month is just the start of a massive bull run that has never been seen before. $SPX could be in for a RECORD YEAR and here’s why:

The similarities between now and 1970s Japan:

• Excess liquidity flooded into a narrow group of assets

→ Japan: land, golf memberships, equities

→ Today: AI infrastructure, mega-cap tech, private markets

• Index concentration masked weakening breadth

→ A small group of winners carried the entire market higher

• Energy shocks hit during speculative expansion

→ 1973 OPEC crisis

→ Today’s geopolitical/oil supply disruptions

• Inflation stayed sticky while central banks were trapped

→ Tightening too hard risked recession

→ Staying loose fueled speculation further

• Valuations detached from underlying economic growth

→ Financial assets inflated faster than the real economy

And here’s the part most people miss:

Japan’s market didn’t collapse immediately after the oil shock.

The Nikkei continued climbing for years because liquidity and speculation overwhelmed deteriorating fundamentals.

That’s what makes late-cycle bubbles so dangerous.

They can survive bad news far longer than people expect.

The 1970s in Japan were not the crash.

They were the setup.

English