Sabitlenmiş Tweet

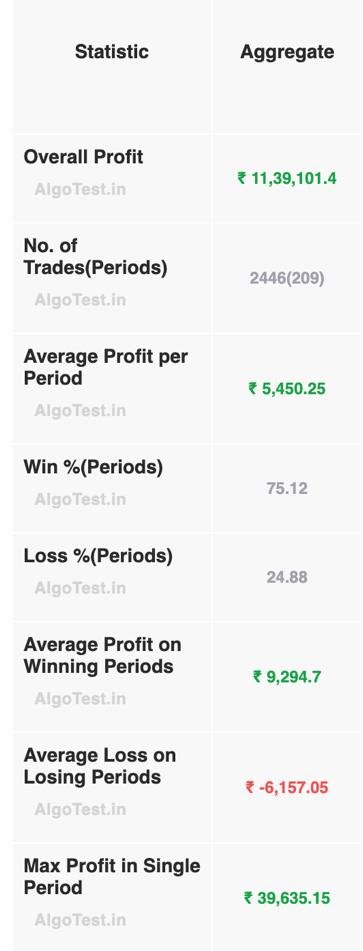

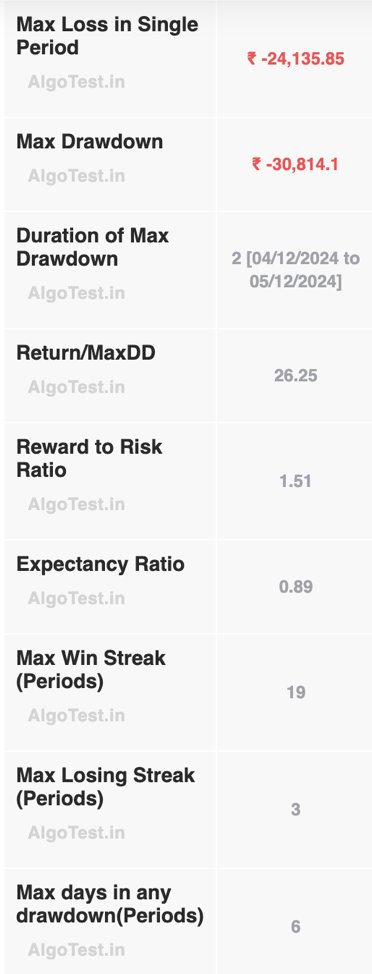

Algotest Option Selling System

(Backtested with 0.8% slippage)

Capital Required= 12L

Avg monthly ROI= 5.6%

Max loss= 1.1%

Drawdown less than 2%

If interested then ping me- wa.link/b6cytl

English

Theta Capitals

1.7K posts

@ThetaCapitals

Formerly known as Ease Trade || DM for Algo Trading || WhatsApp- https://t.co/tkynVU4zE0 || YouTube- https://t.co/Cqm5PK2V2H