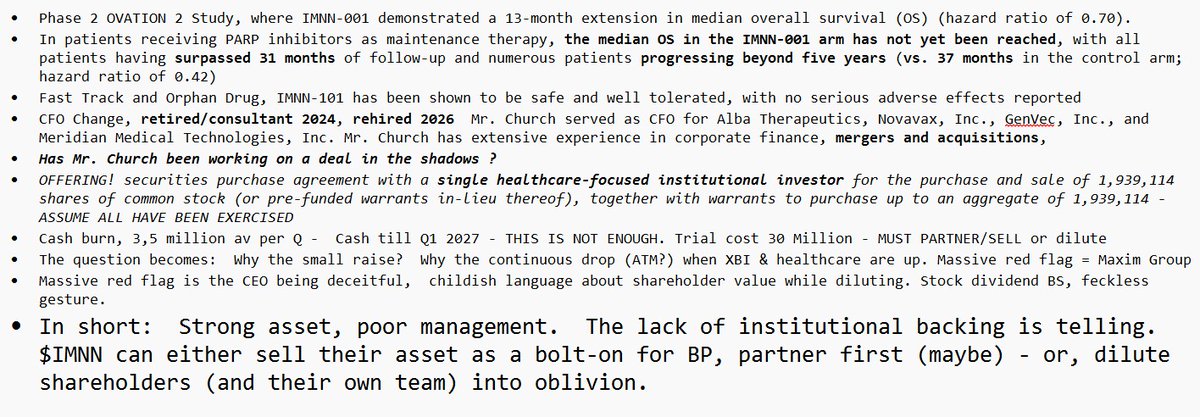

@BAMBossie81 @BiotechAutist The truth is, when more BP's would be interested, the company would be sold already. They have not much cash because investors are not really interested. The question is why? The clinical data of this product is very good, isn't it? $IMNN

English